AF Legal (ASX:AFL)

AF Legal is the publicly listed parent company of a group of law firms specialising in family and relationship law. More specifically the group provides advice to clients in respect of divorce, separation, property, and children’s matters together with related and ancillary services such as litigation, most of which are settled via. mediation as opposed to long-winded court processes. AF Legal is the largest of its kind in Australia.

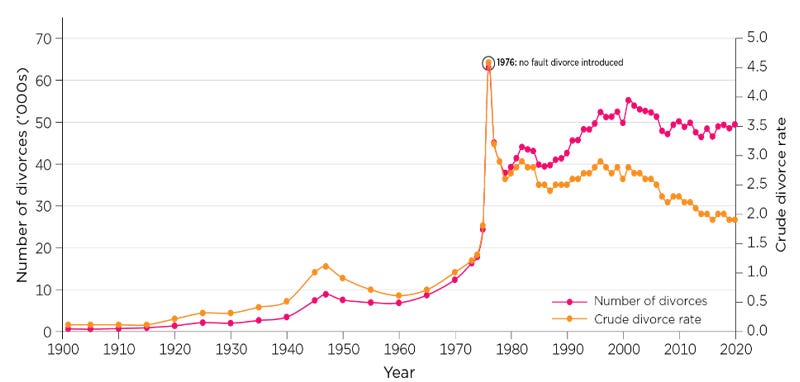

Family dispute resolution is akin in stability to industries such funeral providers and tax preparation, representing a high-quality recurring workflow. In the past 47 years since the no fault divorce was introduced, divorces have slowly but steadily climbed at a rate of about 0.6% p.a. as opposed to population growth of 1.3% p.a. leading to a decline in divorces per 1,000 residents from the ~2.5 people in the late 1970s to ~1.9 today., driven mainly by a decline in marriages as opposed to more robust marriages. However, what really moves the needle for family lawyers is the growth in household wealth in conjunction with the median age of divorce having grown from ~35 in the late 70s to ~45 today, meaning that the average divorced couple has substantially more ‘real’ wealth today than they had in the past.

With this backdrop, you’d expect the family law business to be a great one, with most cases settled by mediation along with ample asset pools to pay in trust leading to potentially brilliant cash conversion. Federal legislation allows for geographic expansion and sharing of resources and the lack of required overheads. However, AF Legal has seen anything but success as a listed company having been founded in 2015 and subsequently listed in 2019 through a reverse takeover of Navigator Resources, since listing at $0.20 in June 2019, it reached a peak of $0.66 in May 2021 before falling to as low as $0.10 in February 2023. Today it trades back at its IPO price of $0.20. So, what happened?

Primarily, this can be traced back to the actions of past management, who were nothing short of predatory in the extraction of what otherwise should have been excellent shareholder value creation. First, the key management remuneration including share-based payments over the period 2020-2022 was an average 15% of group revenue, as opposed to peers with similar margin profiles such as Diverger & Prime financial at 7%. At the corporate level, total expenses were an average 21% of revenue (excl. disbursements) as opposed to the peers with 9% and 11%. It’s clearly hard to argue that management weren’t taking shareholders for a ride. AF Legal has a similar margin profile to Prime Financial (Slightly lower gross margins), so theoretically it should be able to generate margins of ~10% on a net profit after tax basis, yet it averaged closer to NIL due to what was explained above.

This leads us into where AF Legal is today, since the fallout of management during the fiasco that surrounded the unsuccessful GTC Legal merger where internal arrangements were leaked to the AFR and substantial shareholders that led to management resignations and shareholder activism, the management team has been highly streamlined and a cost-conscious CEO that led a very successful turnaround at Ashley Services Group (ASX:ASH) has been appointed in Chris McFadden. In Q3 FY2023 the group reported a consolidated NPBT margin of 10% & 7% before and after non-controlling interest, despite only being the first quarter not inhibited by prior management, alluding to strong potential for the group to streamline their operations and perhaps start to generate shareholder value that attests to the favourable setup of the industry.

AF Legal when the Hurdle Rate Unit Trust purchased it was trading at an enterprise value of $10m despite generating LTM Revenue of $17.9m. If we think the business is capable of ~10% NPAT margins less minority interest, this will equate to a normalised NPAT of $1.58m, a potential post margin improvement PE of 6.3x. Given the improvements they have made in a short time span, I don’t see why this should not be the case. Furthermore, Chris McFadden’s is incentivised to generate $2.35m of NPBT attributable to the parent in FY2024, which at the current revenue is equivalent to a 13% NPBT margin, which would align closely with a 10% NPAT margin. In the event of this profit being achieved, we have an earnings yield of 15.8% which meets our hold return hurdle rate and should be fully capable of some organic revenue growth via. recruitment and rate expansion and/or multiple expansion to get us to a hurdle rate of >25% p.a.