AF Legal (ASX:AFL) - #2 - Deep Dive

AF Legal (ASX:AFL) - #2 - Deep Dive

Australian Family Law Firm

Background

Australian Family Lawyers (AFL:ASX) is the largest family law practice in the country as of the time of writing this memo, Edward Finn founded AFL in 2015 when he saw an opportunity to improve the ways law firms find clients by developing a digital-driven marketing system to remove the reliance on relationship-based business development.

This can be personified with the concept of ‘New Law’, an industry trend that whilst not explicitly defined, refers to the disruption of the legal industry through the provision of services in new ways. This has resulted In an increased use of technology in the workplace, leading to an improved work-life balance. providing new communication channels for clients and alternative pricing models. In stark contrast, ‘Big Law’ is the incumbent personification of bureaucracy at its core, a cutthroat model that compensates lawyers for over-working on tiered timesheets according to their seniority. As an accountant, this reminds me a lot of the traditional Big-4 Accounting firms.

Family Law is a subset of Legal services that has no national presence despite accounting for over $1.1b in annual revenue. From my discussion with Grant Dearlove (Executive Director), previously, the largest in Australia had revenue of $12m, which has since been eclipsed by AFL with their recent acquisition of Watts McCray.

There are two main categories of competitors in the Family Law industry including:

Large generalist firms that offer family law as an ancillary service. These firms have a high-cost structure & lack specialisation & value proposition to clients.

Small specialised firms of 3-10 people. These have key partner reliance & capital constraints to growth, leading to difficulty in retaining staff and entrenched work practices.

In respect of divorces, there are ~50k divorces per year in Australia, the statistics also point towards an older average age of marriage and longer tenure of marriage, but the volumes remain stable thanks to an increasing population. All in all, the industry growth is little to none, but volumes are extremely stable per year (Source: ABS). Importantly, to note is that these figures also don’t take into account de facto relationships. Cohabitation is on the rise, having accounted for 6% of all relationships in 1975 compared to 18% in 2016. (Source: AIFS). Lastly, the size of the asset pool is also an important determinant in seeking legal advice on separation, which of course has been steadily increasing over time meaning more capacity to pay legal fees, this in effect would drive the average legal costs up over time with increased complexity.

Besides this, there is a looming issue in the Family Law Court system of a long backlog of cases, with more than 40% of cases taking more than 12 months to finalise. Thankfully, the 2021 Federal budget aims at providing $100m of funding into the system and reduce costs for all parties involved

Business Model

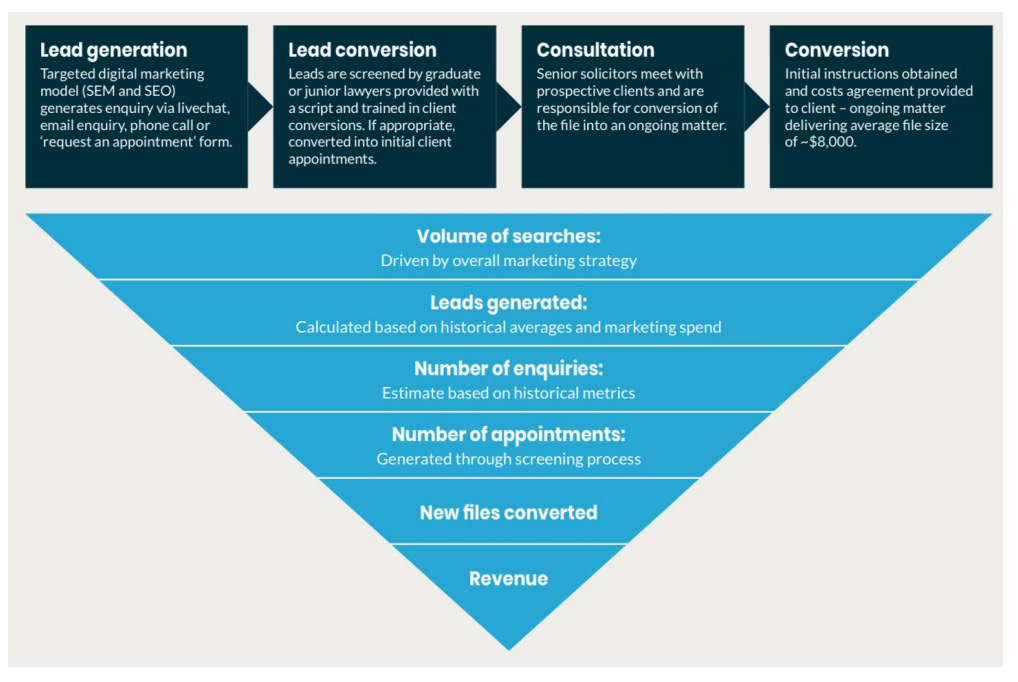

AFL’s business model starts with the foundational use of Data to generate leads. The DSAS (Data, strategy, acquisition, and sales conversion) model takes over the traditional use of a business development team to generate leads

AFL has a 5-step system to converting clients with involves:

Free Consultation via. Phone appointment

Strategy Session ($350) to discuss the situation & provide an estimate of future costs

Dispute resolution where property/children involved.

Assisted negotiation/mediation to avoid courts where possible

Final settlement by consent (preferable) or court hearing.

This process utilises accumulated data related to the online search patterns of the target demographic to optimise marketing campaigns and hire staff effectively where the demand lies.

Due to the reduced reliance on business development teams to generate referrals, the model removes the need to source talent and instead uses data to generate revenue. This makes it more scalable since marketing infrastructure is much easier & faster to implement in various geographies & laterals.

Accounting - Dispelling fears

One of the most common criticisms I received from others when first sharing this investment was the downfall of other listed businesses including Slater & Gordon etc. First of all, this business operates in Big Law and bills often on a “no win no fee” basis. This as a result requires a huge amount of subjectivity when reporting results due to the revenue being based on Work in progress (Dollar value of unbilled work). The subjectivity is mainly on management’s best estimates.

The easiest way to avoid this as an investor was simply to focus on cash flow, but most investors did not, leading to reliance on overly complex accounting that most people wouldn’t even know where to start. Acquisitions have to make sense from day one, and that generally means a clear integration process, strategic purpose and a cash-based low valuation that adds per-share value.

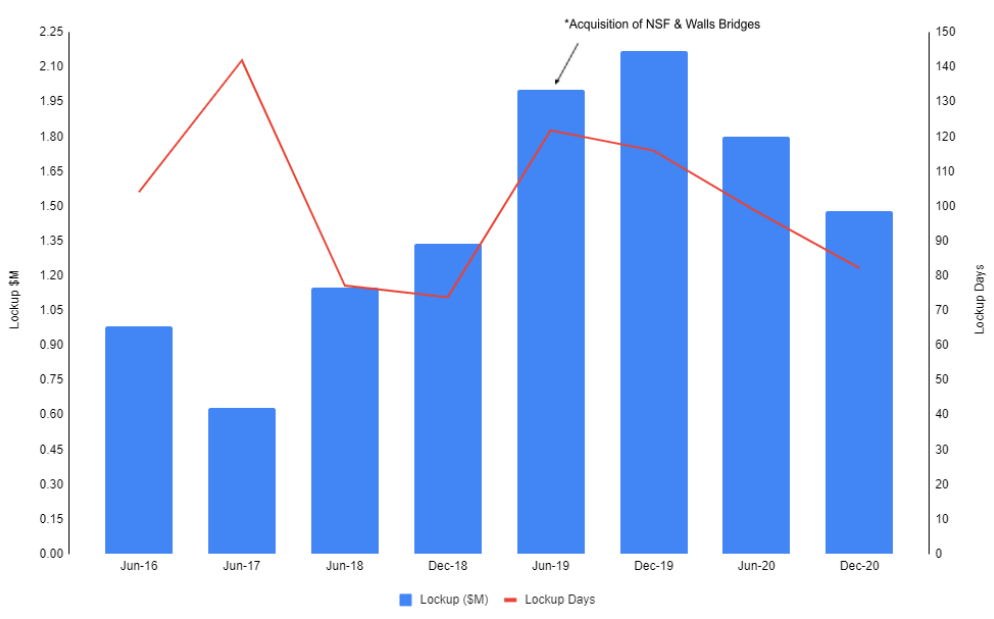

Slater’s acquisition of PSD was littered with red flags but perhaps the most obvious was that neither Slater nor PSD generated any Operating cash flow in the majority of years prior despite the reported profitability. Instead, PSD carried extreme levels of WIP and had a poor conversion. I like to focus on Lockup days as a key KPI for professional service businesses which indicates how long it takes for a client to engage and then pay for a job. Slater and Gordon typically took in the range of 500-700 days (with the majority of it in WIP days) to convert their receivables & work in progress to cash, yet despite this, they were both recorded as ‘current’ on the balance sheet. And we know that this is certainly not the case as the ‘receipts from customers’ line in the annual report was only half of the ‘current’ lockup. A clear misrepresentation on their part.

Nonetheless, it serves as a good example not to ignore cash, in fact, as an investor if I were to rank the importance of the financial statements, it would be the cash flow statement & balance sheet as first and second with the profit & loss statement as a distant third.

Relating this to AFL, the business does minimal work on contingency-based billing, instead of billing monthly based on agreed-upon cost agreements leading to an objective recognition of revenue. Targets are based on a multiple of salary paid rather than billable hours, allowing for greater flexibility in working arrangements.

Comparing Lockup days, AFL had lockup days of just 93 in the 2020 financial year, consisting of just 8 WIP days and 85 debtor days, meaning that the majority of the work has been billed already. This leads to better cash conversion for the business and high cash returns on tangible capital deployed.

Scaling Up - Rockefeller Habits

Now that we have a basic idea of how the business generates revenue, I wanted to give a nod to a book that is present on the Kelly+Partners reading list, a list of excellent books that have influenced Brett to create such an excellent business. This book is called ‘Scaling-up’ by Verne Harnish, a sequel to the bestseller ‘Mastering the Rockefeller Habits’.

I was delighted to find out that one of the current AFL Executive Directors Glen Dobbie is an accredited Gazelles business coach. After careful inspection, I saw several parallels with the AFL growth strategy and the lessons that come from the book including a One Page Strategic Plan (OPSP), use of the sandbox concept, BHAG (Big Hairy Audacious Goal), 3-year plan & Rockefeller habits among others. Glen has a material influence on this business and their growth trajectory through his mentorship since 2016.

Glen is also the Managing Partner of Asia based ‘Auxano’, an independent advisory firm that invests and advises operational and investment expertise to companies to support their growth plans. It’s clear that is the case here, having originally started as a non-executive director, on the departure of the previous CFO, Glen entered the slot as a current CA licensed accountant and assisted the business operations at the time.

Another irony to mention is that Shine Lawyers is also discussed in the book as a Rockefeller-habits driven legal firm which unlike Slater & Gordon does emphasise its operating cash flow. They have a very steady track record having grown its revenue 11 out of the past 12 years with a CAGR of ~15% p.a and EBITDA 10 out of the past 12 with a CAGR of 11.2% p.a. Despite these respectable results the business has compounded at -2.5% p.a. For shareholders, largely due to the valuation contraction over the past 8 years (-9.8% CAGR) offsetting the revenue (CAGR of ~4.3%) with 3% from dividends.

Circling back to Scaling up, this book is excellent and upon reading I was quite surprised at the depth and can see why it’s used by over 40,000 companies worldwide. The book provides tools to navigate the s-curve growth trajectory without blowing up. I think it’s worth going through the 4 key stages of scaling up and applying it to AFL to contextualise the strategy here.

The first stage is People, broken up into Leadership, Management & Teamwork. Leadership can be summarised as having the right people doing the right things right along with the right systems and processes. In essence, it relates to having accountable leaders, which we can evaluate using the current executive and board structure. On the 10th of August 2020, there was an enhancement of the management structure to best reflect each individual’s strengths putting Edward & newcomer Kevin Lynch into a newly established marketing advisory board. Past Shine Lawyers operator Grant Dearlove & Gazelles business coach Glen Dobbie got placed into executive positions to manage the day to day operations. One caveat of which is that the proposed appointment of Matt Seakins as Chief Marketing officer never occurred due to him being poached by another business in an unrelated industry.

Hiring the right team is a process that requires careful consideration and Verne suggests that recruiting is a marketing function that benefits from a large number of applicants, allowing for choice in the hiring process to ensure maximum cultural fit.

Perhaps the most unclear regarding AFL is the coaching function associated with management. What I see is an excellent executive team, however, lateral hires run the risk of cultural barriers to integration. AFL has stated that they have engaged staff with “Individual Plans”, a system to drive individual goal development and have also rolled out incentive plans. It remains to be seen how effective lateral hires can be as coaches, but this is something I may query the business management on in the future as I’m not sold on for cultural fit.

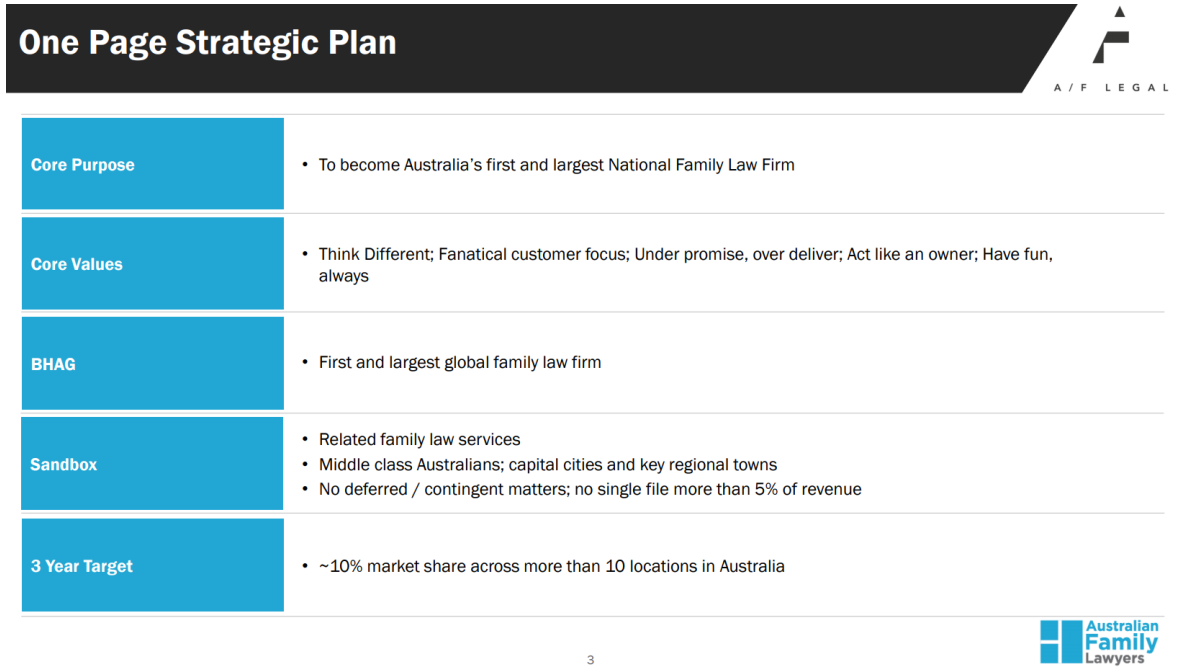

Strategy is the second stage of scaling up and involves a differentiated strategy, supported by a strong culture that delivers on the brand’s promises. For Kelly+Partners their purpose is to help business owners become better off, guided by a set of values to want the best for others, do what they say and in one best way. These are intended to provide a should/shouldn’t test for everyone in the company. AFL has summarised their strategy into a one-page strategic plan as shown below:

To further describe the one-page strategic plan, the 7 Strata of strategy can provide context.

Words you own (Mindshare)

Sandbox

Brand Promise (Catalytic Mechanism)

One-Phrase Strategy (Key to making money)

Differentiating Activities (3 to 5 Hows)

X-Factor (10x-100x underlying advantage)

Profit per x (economic engine) and BHAG (10-25 year goal)

AFL chooses to omit much of this information, perhaps to avoid making things too obvious to competitors but I have my ideas. For example, with the acquisition of Watts McCray, they have the domain name ‘Divorce.com.au’. The brand Australian Family Lawyers also has mindshare potential itself. The X-factor could indeed turn out to be the DSAS model. Regarding the 3 year target, the book suggests that if a company is growing extremely fast anything between 90 days and BHAG is a WAG (wild-ankle guess) and therefore suggests setting 3-5 year targets on an aspirational/aggressive basis. That is exactly what AFL has done, which I tend to agree on as I can’t estimate future growth for this business reliably due to the potential.

The third stage of scaling up is to focus on execution. This is where the Rockefeller habits take their place. These have also been rolled out to the team and the wording AFL uses is as a ‘platform’. The book highlights that there are SaaS tools out there to track the Rockefeller habits and update your OPSP in real-time, which is incredibly useful. AFL recently upgraded to using Salesforce for CRM business metrics, and there is a Gazelles integration that allows for this OPSP called Scoreboard. Of course, I’m not sure if they use this although would not be surprised.

The Last stage is the oxygen of the business - Cash. This stage emphasises the cash conversion cycle as the central concept. For professional services firms, this can be summarised with lockup as discussed earlier. Below is the Lockup History for AFL.

Growth Strategy - Organic Growth

Now that you know the general strategic foundations of the group, it is worthwhile discussing the levers to scaling the business. And AFL has outlined this clearly into 3 buckets, ordered intentionally based on their attractiveness. This hierarchy largely reflects the ‘bang for your buck’ of each which I will further discuss below:

The #1 preference for growth is ‘Organic growth’ which refers to the use of marketing and sales to generate internal revenue growth. This is attractive as it does not cost any upfront capital to commit to. Instead, efforts such as employing call-centre staff & referral networks that are incrementally attractive are sought after.

For example at the end of June 2020, AFL announced an international partnership with Stowe Family Law to provide a referral program for UK citizens living in Australia & vice versa. They have also rolled out additional service offerings including Binding Financial Agreements & corporate services in partnership with Flight Centre. A win-win strategy like this provides a no-cost solution to generating additional sales volumes.

Besides these traditional methods of generating volume, we can not forget improvements to the core of the business. AFL 2.0 is a recent update to the way that AFL finds customers, more specifically, AFL is optimising the use of technology and improving the landing pages of their websites to drive consumers into booking a free phone consultation and the ideal $350 initial consultation. This behaviour feeds into a technology stack including salesforce, WordPress plugins & Google analytics among others to provide useful information to further drive leads & reduce conversion costs.

Growth Strategy - Lateral Hires

Lateral hires involve the process of hiring expert lawyers to run in their existing capacity. For example, hiring a senior practitioner to run a new office in a new location etc. The allure of lateral hires is cost-effective growth in existing and new markets due to the minimal upfront costs. Of course, these aren’t without risk, which is perhaps why they are second in priority as compared with internally generated sales. These risks largely relate to sourcing talent with a cultural fit, pricing them correctly and incentivising them to stay with the group.

Lateral hires are typically incentivised with competitive remuneration and a % of earnings above budget. Besides that, due to the billing model, flexible work arrangements are an attraction as well to provide work-life balance. Long term incentive plans are rolled out after staying for >3 years and if someone leaves, they can’t take their clients with them.

Through my conversings with Grant, Lateral Hires typically bring in books of work worth between 400-800k per year. They are self-sufficient from the get-go, benefit from word of mouth referral work and aim to supplement with the Digital model AFL have created over the years. Perhaps, more importantly, is that AFL does this in a way where the operating costs are kept to a minimum, often looking at utilising existing offices or using shared office spaces. Take for example the Gold Coast office which operates out of a Flexioffice.

Growth Strategy - Acquisitions

The least desirable medium for growth is to grow through acquisition, but it also happens to be the fastest way to grow given the superior operating model that AFL has harnessed. The family law industry was chosen specifically due to its highly fragmented nature and lack of competitive rivalry with no large scale national player.

It is anticipated by AFL that the acquisition strategy will provide the following benefits:

First mover advantage - the first national specialist family law firm

Critical mass - the largest network of accredited family law specialists in Australia

Economies of scale - cost savings from the replication of the AFL model can be reinvested into marketing without diluting margins

Value Arbitrage - AFL will be able to transact at “Small business” multiples before any synergies.

In addition, the Purchase discipline is focused on three key pillars:

Value - Earnings accretion

Model - Clear path to implement the client acquisition model and Rockefeller Habits

Strategy - Strategic purpose (Geography, scale, new services etc.)

This is a solid discipline and given that they have just recently completed the fourth acquisition, I can evaluate the success in execution as seen below:

It’s not hard to determine here that the growth strategy is executed at extremely attractive valuations, and the strategic purpose certainly makes sense. I’m happy with what they are doing here but will continue to monitor the success of ongoing acquisitions.

Growth Strategy - Medium-Term Outlook

I expect that if the Watts McCray Acquisition occurs and AFL DOES NOT use the Cash raised in the entitlement offer to grow further, that the revenue for the business will rapidly grow with minimal dilution and the use of no debt. Given the price paid for one of the largest firms in the country ‘Watts McCray,’ i expect them to be able to continue to add value and scale up over time along with supplementing this with the expansion of their referral network, continued improvement of their marketing engine along with geographic expansion using lateral hires.

The risks to watch out for include the retention of staff and cash flow discipline. However, these are not difficult to track as it seems to be universally agreed upon that each staff member has a Linkedin account, allowing for monitoring of the staff overtime and consistent updates through their social feed.

Valuation

This is the least useful section of the entire post, as it’s difficult to put a number on given the frictionless growth experienced so far and attractive use of valuation arbitrage on acquisitions.

Regarding the FCF, this is another point in which I suppose deems an explanation given that the Net profit margins are only in the mid-single digits, so optically the business is trading at more like 40-50x statutory earnings, which given the growth I would still consider fair to modest. But this does not reflect the underlying profit potential of the group and belittles the focus on cash they have fostered. A reconciliation is provided below to demonstrate this using actual figures.

The main things that are obscuring the underlying profitability are the normal course of w/off of lockup, a typical practice in a professional services firm, and has no bearing on cash flow. Furthermore, on the Listing of AFL, the IP was capitalised on the BS and is being amortised. Once again, this has no bearing on the underlying profitability of the business.

Nonetheless, I paid a price of just $0.45 for AFL in December of 2020, just after they had acquired Strong Law. At this point, I suspected that the run rate was at least over $10m or $0.16 per share along with having $0.03 in cash on the balance sheet which has since been used to pay the Watts McCray debt off. This means I was paying a price of ~2.5x forward sales for a business capable of free cash flow margins of 20%+. Given the growth potential of the business, you don’t need to be a genius to realise how insanely cheap this price is. A FCF yield of ~6% for a business growing 30%+ on a per-share basis provides some downside protection if you’re wrong.