Amira Nature Foods (NYSE:ANFI) - One Page Stock Pitch

Amira Nature Foods (NYSE:ANFI) - One Page Stock Pitch

UAE Basmati Rice Grower

About

AMIRA is a major international producer of Packaged Food, Indian Specialty Basmati Rice and over 200 food products, with sales across five continents around the world.

AMIRA generates majority of its revenue through the sale of Basmati rice, a long-grain rice grown only in certain regions of the Indian sub-continent, selling its products, primarily in emerging markets, through a distribution network.

AMIRA offers an extensive portfolio of brands that have been carefully developed to appeal to local markets around the world. Customer tastes and expectations have been finely segmented to deliver authentic flavors that go well with a variety of popular cuisines. Consumer palettes across the market segments have been well researched and adapted to suit the requirements of various trade channels. AMIRA has expanded its product line into snacks, Ready-to-eat and organic food products.

All of AMIRA’s branded rice products are made with rice that is grown in the areas of India that area specially dedicated to basmati rice production. The rice is aged for up to a year before being processed, then prepared at a stateof-the-art treatment plant that preserves all its purity in perfect hygiene.

AMIRA has expanded its portfolio to include brands of oils, dairy products, snacks, and ready-to-eat meals.

Strategic Vision

We at AMIRA, endeavor to build relationships that bond people and cultures across the world through the common language of food, which we call the Food Connect.

With the power of Food Connect and driven by passion for purity, we are committed to creating a global food brand.Our unrelenting focus on quality, innovation and superior taste reflects in our wide range of products, enabling us to build sustained consumer loyalty, making AMIRA, simply the best money can buy.

The appeal of basmati rice around the globe as a healthy food is considerable. Basmati rice is a super grain: It is gluten free, cholesterol-free, and its cultivation requires approximately 50 percent less water than does that of other kinds of rice.

AMIRA’s brand of basmati rice is one of the four major brands in India, according to Marcom ratings. It is distributed both in the country’s traditional distribution networks, and in the newer, ‘Western’ style retail outlets that today account for about 19 percent of the country’s retail network. In India we continue to increase the number of our distribution centers around the country, with four new ones set up in 2013. We are also distributed by Wal-Mart in India.

Outside of India, in emerging markets, AMIRA is working with 3rd party distributors in long-standing and deep-rooted white-label arrangements. These offer a low-risk entry for our product into many markets, and there is still vast potential for expansion in this area.

And AMIRA is already successfully penetrating high-growth markets like the US and the UK.

In the U.S., we work with major retailes like CostCo, and we expect to greatly expand our alliances in that market. In the UK, we are already present at Morrisons with five products. Again, there is great potential for expansion here.

AMIRA is also now expanding into new products. We already offer a line of ready-to-eat snacks and institutional packaged products. And we are expanding with a line of organic products that will launch in Europe and the U.S. in the coming year. There has already been a very positive reaction to these products at trade shows both in the US and in Europe by retailers who are eager to expand their healthy product offerings.

In every market, AMIRA has vast room to expand. With a healthy balance sheet (see latest financial information), and burgeoning sales, AMIRA has the very best chance for rapid growth in the coming years.

Financial Information

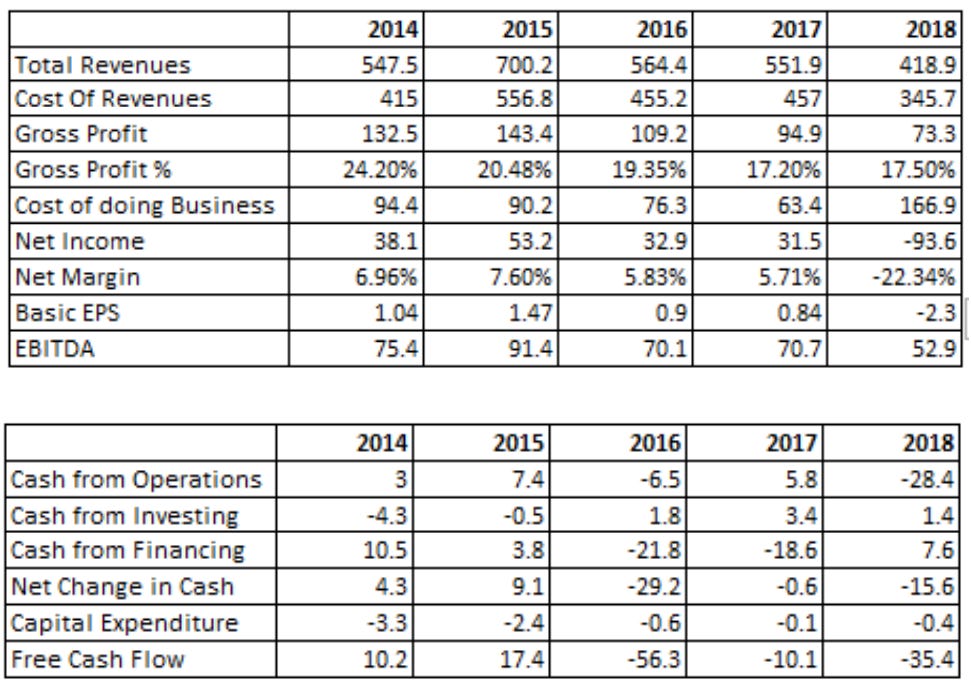

Amira has suffered a significant decline in it's share price in recent years. Part of this is due to declining financial performance, however that has pushed the stock to deep levels of undervaluation, so much so that we can consider this a cigar-butt stock.

First thing to note is the drastic drop in inventory over 18 months. In their words

"We carry inventories for a regular period of time and at times upon careful consideration, inventories are written off on their natural qualitative deterioration. However, this year we identified certain deterioration in quality of inventories primarily due to large number of warehousing facilities spread across India, the mismatch in cash-to-cash cycle and sporadic unfavourable weather conditions. The management believes these are one-time events driven largely by macro-economic conditions as also, by uncontrollable external factors. This deterioration in quality of inventory results into a higher percentage of broken rice content upon processing. The management has decided, consciously and conservatively, to recognise a provision for impairment of inventories for $134.0 million, considering the adjustment in its realisable value. "

So from this we can highlight this as a large risk. Are the remaining inventories still held at value fairly represented?

The next thing of note is the increasing shares on issue. This is largely due to a debt to equity conversion of a subsidiary. As a result of the debt conversion, the Company’s ownership in Amira India decreased from 80.4% to 49.8%. This event is a continuation of Amira’s focus on strengthening the Company’s international business.

Turning the focus to profitability. The company has guided towards a $200m revenue figure for the year ended 31 March 2020. Given a $124m result for the 6 months ended 30 September 2019. This is quite a weak guidance. Yet the important thing is how their assets hold up as a result. Such a deep discount to tangible book provides a huge margin of safety for the share price to revert.

The Good & Bad with the business

Good

Rice is the primary stable for 50% of the world's population, has a huge market in Asia and India. The total Global rice consumption is currently almost 500m metric tonnes growing at an estimate 2% CAGR. The value of this market translates to an estimated $275b USD. This means their is a huge opportunity for Amira to gain addressable share of the market.

To add to this point, Indian Basmati rice in particular is growing much quicker in volume at over 10% CAGR. This translates to a potentional $7b addressable market.

Defensive and non-cyclical

Rice has a Long shelf life.

Karan A. Chanana Chairman & CEO retains a large stake of ownership in the company, representing over 50% of the overall share capital.

Bad

Inability to file Form 10Q for multiple successive quarters. The most recent results i could find for the company were those ended 30 September 2018. This is inexcusable for a public company and have since had much correspondence with the SEC, recently requesting a late lodgement for the Financial year ended 31 March 2019 that will grant them relief until February 16 2020. As reported in the Form 12b-25 filed with the SEC on July 31, 2019, the Company experienced unexpected delays in the completion of the audit of its financial statements for the year ended March 31, 2019 because of corporate organization restructuring that occurred as a result of the de-consolidation of the Indian subsidiary as of November 18, 2018. The Company intends to file its Form 20F as soon as practicable.

Declining operational results. Revenue forecast of only $200m for FY2020 represents an over 50% revenue drop. While the stock is so cheap that it isn't really priced for growth anyway, depending on the costs of doing business, this could hint towards a big loss for the year. That remains to be seen yet given the gap between asset value and share price, that is our margin of safety. The Company had received notification regarding the price deficiency on November 16, 2018. The NYSE requires that the average closing price of a listed company's shares be no less than US$1.00 per share over a consecutive 30 trading day period and close above US$1.00 per share on the last trading day of the month to regain compliance.

The Company has been notified by the NYSE that is has cured the price condition and regained compliance with all NYSE continued listing requirements as of March 29, 2019. However, now the price is once again below $1.00, this is a regulatory risk and could result in them being delisted or forced to buyback stock to prop market prices up.

Conclusion

Amira Nature Foods Ltd represents a depressed stock due to issues with lodgement to the SEC on time and declining sales conditions. Despite this, the company is still significantly worth more than what is quoted by the market on an asset basis. With such a large margin of safety, a catalyst such as a expansions to their international business could turn the stock around, closer to book value. Given the uncertainty of this thesis and substantial upside, a small position is suitable as the position has potential to become a multibagger if this thesis plays out. FY2019 Results will be the next point to review the thesis and i will review the fact in the quarterly report of that quarter.