Bank OZK (NASDAQ:OZK) - One Page Stock Pitch

Bank OZK (NASDAQ:OZK) - One Page Stock Pitch

US Regional Bank

Bank Ozk, formerly Bank of the Ozarks, Inc., is a state chartered bank that provides retail and commercial banking services. Its deposit services include checking, savings, money market, time deposit and individual retirement accounts. Its loan services include various types of real estate, consumer, commercial, industrial and agricultural loans and various leasing services. It also provides mortgage lending; treasury management services for businesses, individuals and non-profit and governmental entities, including wholesale lockbox services; remote deposit capture services; trust and wealth management services for businesses, individuals and non-profit and governmental entities, including financial planning, money management, custodial services and corporate trust services; real estate appraisals; ATMs; telephone banking; online and mobile banking services, including electronic bill pay and consumer mobile deposits, and debit cards, gift cards and safe deposit boxes.

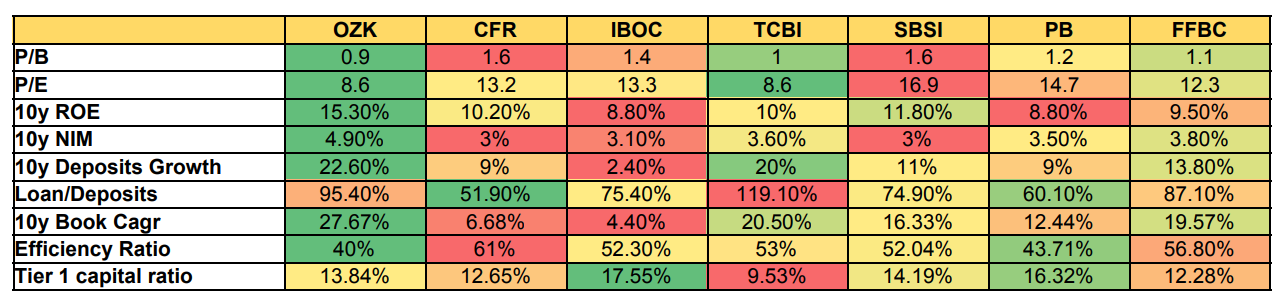

The bread and butter for a bank is the ability to draw in customers, denoted with growth in deposits. These deposits can then be used to make loans to more customers. That is the essence of the business model of a bank. As I mentioned deposits are used to make more loans to customers. The key metric here is the ‘Net interest Margin’ which essentially compares interest costs to interest income. A higher margin indicates a higher degree of profitability.

The spread of interest is very important, however not all costs are interest related. Taking a whole picture perspective and incorporating the non-interest expenses is key. For this, using the ‘Efficiency Ratio’ can indicate how profitable a bank is from a total operating margin perspective.

Leverage is also key when looking at returns on equity (ROE). To generate additional revenue, instead of growing deposits, a bank can borrow money from a third party and loan out to customers. This may increase revenues, although it increases risk and ROE should then be adjusted to an unlevered amount for a fair comparison on business profitability. The key here is the ‘Loans to Deposits’ ratio which indicates whether a bank is loaning out in excess of it’s deposits.

Of course, the risk of the current financial position should be taken into account as well. For this, post the 2008 Financial crisis, ‘Basel 3’ introduced regulatory liquidity requirements. The ‘Tier 1 Capital’ ratio is a key measure of this regulatory development that measures a bank’s financial strength. A comparison using these highlighted factors above indicates a strong tendency for Bank OZK to come out more attractive on most metrics. This is quite amazing and it’s a testament to the quality of the business.

This is largely in due part to the ‘Outsider’ CEO ‘George Gleason’ that has run the business as executive for 40 years. In addition to this, to act as incentive he currently holds almost 5% of the company. While this doesn’t sound like much, the dollar value of this is close to $200m. Given his annual salary of ~$1m, the movement of his shareholdings is material.

Of course, being value investors price is key to the process and this is no exception. Bank OZK is currently trading at 0.9x book value. Furthermore it has compounded this book value at 27.67% CAGR over the past 10 years. So paying an earnings yield of 11.6% and having the company grow at 20%+ a year is a very attractive scenario. Of course the prospects of margin expansion at a historical low help the case significantly.