Charle Co (TYO:9885) - One Page Stock Pitch

Charle Co (TYO:9885) - One Page Stock Pitch

Japanese Women's Underwear Net-Net

CHARLE CO., LTD. is a Japan-based company principally engaged in the wholesale of women's underwear. The women's underwear anchored clothing and cosmetics wholesale business sells clothes, focusing on women's underwear, as well as cosmetics and others, produced in Japan and overseas subcontract factories. The Company operates door-to-door sale and mail order sale business through its business members, via home party-style fitting sessions for membership and general consumers.

Similar to Gamecard Joyco Holdings , Charle Co Ltd is trading below it's net cash position at a Price/Net cash of 72%. Not quite as attractive of a discount as Gamecard was, however Charle Co also has some property and land on it's balance sheet net of depreciation which could have great value.

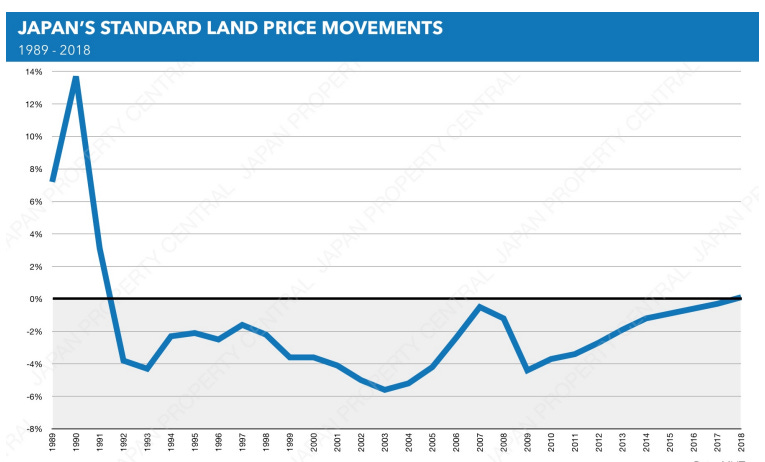

Specifically the Land has not changed in value for a very long time as i can see it is the same value in the 2009 Balance sheet.

However, market trends for land have been negative for a long time so the realisable value of this land is debatable.

The value depends on when this land was purchased essentially. But given the overall trends this can't be safely assumed to have a higher realisable value than recorded on the books.

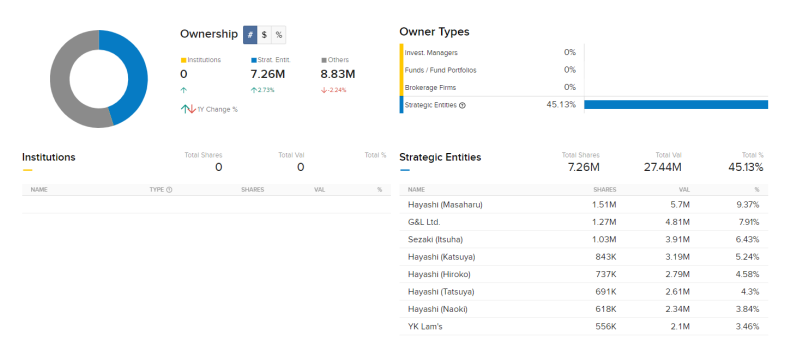

There are small ownership details in the firm’s FY2017 financial statements. The company’s President & Representative Director, Mr. Kazuyoshi Okudaira, held 10,000 shares; and, Mr. Osamu Hirayama, Director, held 2,000 shares. Their combined stake of 12,000 shares 0.075% is only worth 6.36 million JPY at today’s market price (equivalent to 0.06 million USD, which is negligible, so Charle Co. fails this criterion. There is one Hayashi family which holds substantial number of shares in the company but they are not in the management board.

This ownership has remained the same for the company since listing in 1998.

The main attraction here is that Charle Co maintains a 2.3% dividend yield and has grown it's asset base quite a lot over the last few years while the price has barely moved. This elastic effect makes me comfortable to hold with substantial downside protection and very strong upside potential.

There has also been a reduction in shares outstanding during the last few years with an authorised 16% of float buyback in 2016.