China Index Holdings (NASDAQ:CIH) - One Page Stock Pitch

China Index Holdings (NASDAQ:CIH) - One Page Stock Pitch

HK Commercial Real Estate Website

This purchase was put forward to me by ‘The Bad Investor’ on Twitter. CIH is a ‘Spin-off’ from Fang Holdings Ltd (NASDAQ:SFUN) completed in June 2019 and taded at $3.20 on the day.. The business operates the Commercial real estate portion of ‘Fang.com’ while ‘Fang Holdings Ltd’ operates the residential portion of the site.

What interests me in particular is the capital-light, high-quality business you’re getting for an unreasonably cheap price. Some highlights include a stable 80% gross margin, 40%+ operating and net margins, 20%+ Revenue CAGR along with a debt-free and float-heavy balance sheet.

All is not as good as it seems though, as the share capital is worth inspecting further to identify some key risks and why this only takes place in my asymmetric basket rather than my high-quality holdings. Looking to the Prospectus, on page 1 you can see the structure of the shares. The shares listed are the American Depositary shares (ADR) which take up the majority of the Class A shares. Breaking it down to the percentage I get 65.96% of the total shares outstanding held by ADR holders. So when taking into account consolidated accounting figures, you have to remember that not all of the published figures are attributable to you as an ADR holder. And unlike minority interest holders, these class B shares aren’t segregated in the accounts which can be misleading.

Keeping this in mind, after splitting out the share capital structure I calculated an equivalent EV/FCF ratio of just 4.73x and a PE of 14.69x. This large discrepancy can be explained by the fact that the company has no debt, a large amount of cash on the balance sheet and a large amount of deferred revenue which increases the cash conversion well over 100% of net profits.

Lastly, and the main reason the company didn’t take a spot in my high-quality portfolio is the voting interests attached to the Class B shares. First of all, the holder of the entirety of these shares is the executive chairman.

“Each Class B ordinary share shall be entitled to 10 votes on all matters subject to the vote at general meetings of our company. Voting at any meeting of shareholders is by a show of hands unless a poll is demanded. A poll may be demanded by the chairman of such meeting or any one shareholder present in person or by proxy.”

This effectively gives the chairman in excess of 80% of the voting rights of the company along with the fact that being a chairman means he can demand a poll at his discretion.

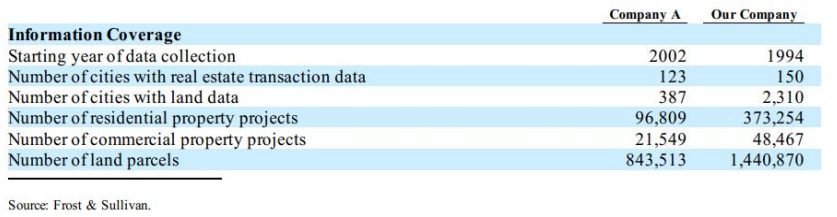

In addition to this, China Index Holdings operates as 1 of 2 services providers in the real estate information, analytics and marketing service industry in China that provide the service nationwide. Other major market players provide services to specific regions in China, the revenue generation capability of which falls far behind the nationwide players. Among them, China Index Holdings operates the largest real estate information and analytics service platform in China in terms of geographical coverage and the volume of data points as of December 31, 2018, according to a Frost & Sullivan report. The following table sets forth the two players with national coverage and their respective data coverage in multiple dimensions.

The competitor is E-house holdings (HK:2048) which is one of China’s leading real estate agencies. As you can see above, the volume of data is still outpaced by China Index Holdings. Furthermore, some scuttlebutt from the aforementioned ‘Bad Investor’ has indicated that most leading developers in the region use both services if they can afford to. If not, CIH is often the preferred option as it is 40% cheaper than the E-House service. In short, you can see this pick is definitely very cheap. However the margin of safety offered is essential due to the risk of voting rights held by the chairman. This still constitutes a strong investment for me given the quality of the company.