Diverger (ASX:DVR)

Diverger provides services to circa 3,000 accounting practices, 150 financial planning firms and 600 licensed advisers. These services include licensing, back office, equity investment and managed portfolio services for financial advice firms along with CPD and help-desk support to accounting firms.

Historically the business was known as Easton Investments and is only relevant from the start of the 2014 financial year onwards when Kevin White (Founder of WHK Group/Crowe Howarth) who subsequently went on to acquire the Knowledge Shop training business along with the Merit Wealth AFSL, and some great talent as part of that deal in Greg Hayes and Lisa Armstrong. From here the group made leaps and bounds in terms of improvement in profitability with a misstep buying AFSL licensee GPS wealth in 2017 shortly before the royal commission into misconduct in the banking, super and financial services industry, however, despite this drastic industry event, the group-maintained profitability throughout and has successfully shifted their business model. Kevin White served as CEO for part of 2014 before Greg Hayes was appointed CEO from 2014 to 2020 before current CEO Nathan Jacobsen joined as part of the acquisition of Paragem.

Financially, the group has several service lines with vastly different margin profiles. Firstly, the accounting solutions division inclusive of Knowledge Shop and TaxBanter accounts for 49% of the revenue but 58% of the profitability of the group. This division has a 40% EBITA margin with its primary cost being direct wages accounting for 51% of its revenue, leaving a mere 8% to other expenses. The wealth division is inclusive of both the licensee business and the managed portfolio business. It is difficult to put a number on just how much profit is being driven by each side, but I do know that managed portfolio’s has a significantly higher margin than licensee services, which is unsurprising as we might assume the average adviser does ~$450k in revenue and Diverger is bringing all of that in to their accounts before forwarding the advisers share, debiting $37k of that as net licensee revenue, therefore it would be more fair to consider wealth margins on the basis of revenue share being a mere disbursement to underlying firms rather than revenue, In this case, wealth has EBITA margins of c.25-30%.

Cash conversion is exceptional in all cases, with the training business having 2 billing models, with ~40% coming from recurring subscription revenue billed monthly in advance and the remaining 60% coming from on-demand training, often billed well in advance of the training date as well. Wealth consists of the licensee business which controls the flow of adviser cash, receiving directly from clients before forwarding to advisers, the CARE business bills management fees at a rate of 0.297% p.a. of which is apportioned monthly.

Shown below is the development of free cash flow and cash returns on equity and capital over the past 10 years.

Over this period the group has accumulated an incremental $26.7m of capital and grown its free cash flow by $5.5m, an incremental return on its capital of 21% p.a. Furthermore, when including dividends declared an investor would’ve seen an additional 4% p.a. dividend yield. Despite this, capital growth in the share price was a paltry 7% p.a. for a total return of 11% p.a. As you would surmise from this, the valuation multiple demanded by the company hasn’t kept up with the pace of business growth with a 3.3x increase in free cash flow per share occurring whilst it is now trading at 0.9x it’s 2013 enterprise value per share. Therefore, the group has suffered 14% annualised multiple contraction since 2013…brutal.

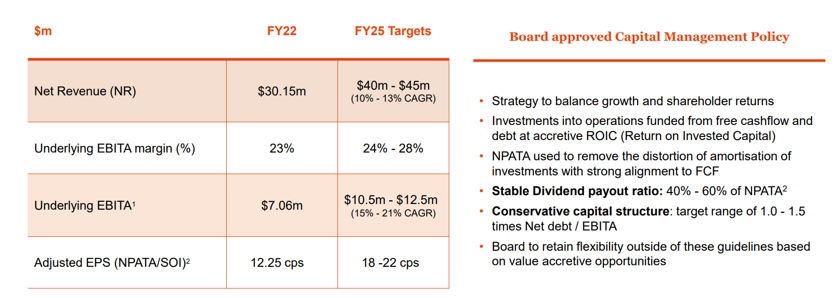

Going forward, the management team are enacting on a strategic plan and capital management policy detailed below.

Positively, the group now is valued at an enterprise value of just $32m ($0.80 cost) whilst generating free cash flow more than $4.5m, an EV/FCF multiple of 7.1x which when considering the above mentioned strategic goals and the 40-60% fully franked payout ratio that would provide a yield of 8-12% for investors, and implied incremental returns on their capital of 25%-50% (based on a low case of 15% EBITA CAGR / 60% retention rate OR high case of 21% EBITA CAGR / 40% retention rate). Further to this, management is incentivised with performance rights that straight line vest based on (1) EPS CAGR of 13.5% to 18% and (2) TSR CAGR of 12.5% to 20% with a baseline EPS and share price of $0.1225 and $0.94 respectively. Nevertheless, Diverger represents what I believe to be a high-quality business at a low valuation.