DSW Capital (LSE:DSW)

DSW Capital is the listed parent company servicing a small UK-listed network of accounting firms, predominately in corporate finance, but also various other service lines including insolvency and business planning etc. The business was established in 2002 by three ex-KPMG partners, James Dow, John Schofield, and Mark Watts who collectively own 37% of the company today. When you include immediate family and business partners that figure is closer to 78%. James is the CEO of the parent, Mark is active in corporate finance, and Jon is acting as a non-executive.

The rationale behind DSW was to disrupt the status quo oligopoly of the big 4 accounting firms by allowing senior staff in those firms the opportunity to leave and start their own business under the DSW brand. With the myriad of corporate failures under the oversight of these firms, there has been countless calls for the firms to restructure, particularly by separation of consulting related service lines from audit services. The co-existence of audit and consulting creates a conflict of interest that starkly contradicts an auditor’s requirement to show independence. An example of this includes the KPMG UK restructuring practice being sold to Interpath Advisory where KPMG stated that “an increasing number of conflicts of interest had become too complex and was ‘likely limiting’ the growth of the firm’s restructuring business”.

The parent company enters into licensing agreements whereby each licensee business will split a % of their revenues with DSW in return for HR, marketing, finance, and IT. DSW typically enters their license arrangements through lateral hires (individual or teams) by enticing them with funding initial partner drawings of up to £50,000. Additional benefits to being part of the group include both a 5% introduced service line incentive and 10% referral fee commission in addition to the use of an established brand which is now in the UK’s top 50 accounting firms. The group’s global M&A network “Pandea Global” also provides a good platform for inbound M&A search from global sources.

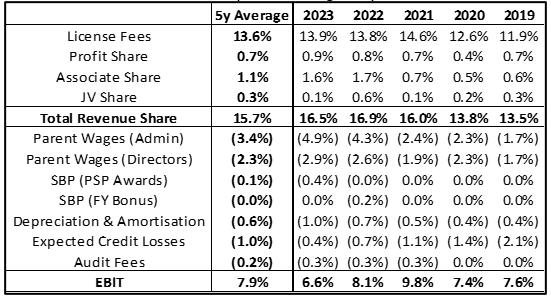

Financially, the licensing model is a share of revenue rather than an acquired ownership in that business. In some cases, an equity stake is also taken in their underlying network firms, meaning that they also receive some profit share, but it is not consolidated as it accounted for as either an associate (50%>20% ownership) or an investment (<20% ownership). This means that the parent company is highly capital light since it can service the network with 1/10 of the employees required in the underlying network. So, where the underlying firm may spend 50% of its revenue on its fee-earning staff, for DSW it may be closer to 5% of the underlying firm’s revenue. In addition to this, the cost base of the parent includes directors’ wages, compliance costs and a single office. Credit losses pertain primarily to start-up loans.

A few takeaways from the development of their income statement are that the parent company has historically been under resourced, indicated by the 3x growth in admin wages as a % of revenue. Furthermore, additional directors with the listing have caused these wages to increase along with associated share-based payment plans. Interestingly, credit losses have reduced significantly, reflecting more organic recruitment and marquee acquisitions in recent years as opposed to licensee loans.

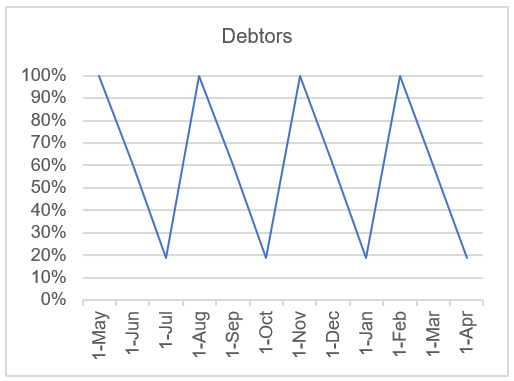

Licensees are 100% equity owners of their respective businesses, meaning that they pay themselves out of partnership profits and are incentivised to collect as a result. Unlike their listed peer Keystone Law, DSW does not collect client revenue before paying it to the partner, so there is a debtor raised specifically for license fees due to DSW on a quarterly basis. Similarly, there is one for profit share due as well. Lastly, it is treated as a debtor in the accounts, but startup loans will ebb and flow with recruitment efforts.

On the topic of future growth, the group has identified multiple avenues for potential recruitment including organic recruitment by existing partners, start-up loans to lateral hires, and acquired license fees. Their initiatives on these fronts include engaging a recruitment consultant in recent months to drive organic recruitment and lateral hires along with the introduction of the £50,000 ‘breakout’ incentive mentioned earlier. Speaking with James, it appears that acquiring license fees (such as Bridgewood) was a primary driver of seeking the listing, as they believe given market dynamics with the Big 4 afforded them to garner more scale and presence to take advantage of market conditions.

In its current state, the group generates more than 2/3 of its revenue from the cyclical corporate finance related service lines. With sustained weakness in the economy, this will continue to be a significant drag on parent level margins. During 1H23 revenue generated per M&A fee earner was ~£19k whereas in 2H23 it was ~£11k, with a cost to service of ~£8k per half, it is easy to see the impact that this can have on parent profitability with a 1H EBIT margin of 58% relative to 29% for the 2H. This can be seen as a strength of the model as well however, as 2H represented the weakest revenue per fee earner DSW has seen in over a decade yet still generated PBT margins of 37%. Furthermore, their flexible license fee whilst appealing, could cause problems with network contagion in the future if partners have issues with varying revenue share.

DSW Capital trades at an enterprise valuation of just £8.4m (£0.60 per share cost) despite generating normalised NPAT of £1.1m in FY2023 where their main activity of corporate finance was suffering significant declines in volume. With a payout ratio of 70%, the shares offer a 6% dividend on top of a model which affords significant organic recruitment potential. Capital allocation has historically shown to be successful with a highly flexible negotiation model, price discipline, and genuine revenue synergies due to their range of service lines and incentive fees. To hit our 15% hurdle for EPS growth + dividends, the group needs to generate a 30% ROIC on the capital it retains, which it has done so in all the past 5 years. For our total hurdle of >25%, the business trades at <8x earnings whereas the closest peer Keystone Law has had an average PE of >30x since it’s IPO. Over a 5-year holding period we would only require DSW to reach a PE of 13x for us to meet a hurdle rate of 25%.