Evergreen Gaming (CVE:TNA) - Deep Dive

Evergreen Gaming (CVE:TNA) - Deep Dive

Washington Land-Based Casino's

Evergreen is in the business of overseeing the gaming operations of its principal U.S. subsidiary, Washington Gaming, Inc. (“WGI”). WGI, through its subsidiary corporations, operates four casinos in Washington State: The Riverside Casino in Tukwila, Goldies Casino in Shoreline and Chips and Palace Casinos in Lakewood. The Company did operate a fifth casino, the Palace Casino in Tukwila, but that property was closed on February 4, 2017. These are mini-casinos (or house-banked card rooms) which offer to persons of legal age a variety of card games of chance at which the player may win or lose money, a business commonly referred to as “gaming”. The Company also operates bars and restaurants in each casino, as required by state law. The casinos currently offer card games such as Poker, Blackjack, Spanish 21, 4Card Poker, PaiGow and Baccarat. Each casino has up to 15 gaming tables and, in accordance with Washington State gaming law, the maximum single betting limit is $300. They also offer a game known as “pull tabs”, a game in which the player can win specified prizes by matching certain combinations concealed under perforated strips on each paper game piece.

The Spectrum Gaming Group completed a market study on the cardrooms in the state, highlighting the following which differentiates most from each other.

"Due largely to the 15-table cap, we found that the primary points of differentiation among cardroom operators are in the quality and breadth of their food and beverage offerings as well as the overall environment. In our observations, cardrooms were less like casinos and more like comfortable, unintimidating hangouts for locals – and thus one reason for their appeal."

Furthermore in regards to the drivers behind the industry, the study highlighted a particular point of challenge for the industry.

"According to the RGA leaders we interviewed, cardroom dealers must be paid the minimum wage, as they do not meet the necessary requirements for exemptions under the law, even though tip income for dealers can be extensive. According to one operator, every 10-cent increase in the minimum wage adds $1,000 in cost per month. That presents a serious future challenge to an industry, particularly in light of an upcoming referendum that would raise the statewide minimum to $13.50 over a four-year span."

Evergreen Gaming has operating profit margins that regularly achieve over 10%, putting it into the higher tier of card rooms.

"Such increases, coupled with related requirements on paid sick leave and other areas, will place material pressure on an already pressured industry, according to RGA leaders. They report that about 20 percent of their members are presently operating at a loss, while those that are profitable are likely to be reporting profit margins in the 5 percent to 10 percent range. We note that for Fiscal Year 2014, the last year for which WSGC data are available, 14 of the 49 cardrooms reported a net loss and 18 more operated at margins of less than 10 percent. "

"Low margins lead to lower capital investment and marketing outreach, which in turn can depress revenues and further depress profits. In challenging times, their profit margins face erosion from a variety of sources, but in profitable times, cardrooms face challenges from new competitors who view cardrooms as a low-cost means of entering the gaming business."

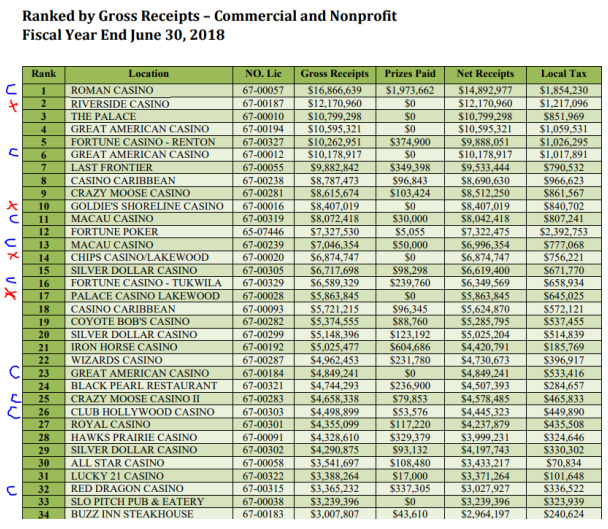

Geographical advantage I would consider very important in determining the competitive edge and ongoing quality of revenue when looking at Casino's.

Using the above we can see all of Evergreen Gaming's Casino's come in the top 20 in the state in terms of gross receipts.

Another listed company 'Nevada Gold Casinos' owns a few on this list as shown below. However while competitors they also have horrible margins fluctuating between 05% per year on an operating basis.

Speaking of Nevada Gold, the company was recently acquired by a Las-Vegas based gaming operator Maverick Gaming LLC along with many other Cardrooms. This external force has bought 20 Casinos and owns over 300 of the states' cardrooms over the span of 2 years. This aggressive action puts a risk that Evergreen may be bought out. At an acquirers' multiple of 3.14 it's no doubt considered attractive and I'm reasonably certain that Evergreen Gaming is on their radar. Of course such a strong asset and revenues It's a risk they will be underpaid for leaving investors with mediocre results. However that's something that will have to remain to be seen.

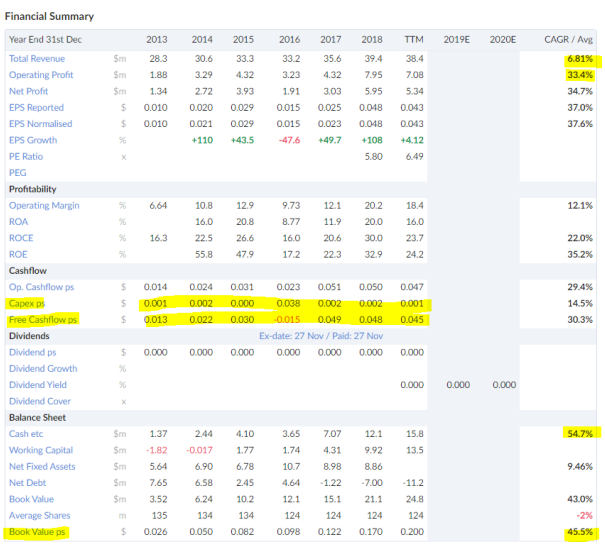

Turning to the Fundamentals of Evergreen Gaming we see quite an attractive proposition. At first glance you see that the company is growing operating profit significantly faster than revenues while on average spending little to nothing on capital expenditure. This has resulting in growth of book value per share at a 6Y CAGR of 45.5%.

So with the highlights made, why is this the case? For revenue growth the Economic market study mentioned earlier covers a trend of reduction in the number of cardrooms. While total revenues are decreasing, the number of cardrooms is decreasing at a faster rate, causing the revenue per cardroom to increase as a result. This consolidation is assisting growth in higher quality Casino's such as those owned by Evergreen Gaming.

As for earnings, the above trend has assisted given their margins, however for the excess this can be attributed to a number of factors including:

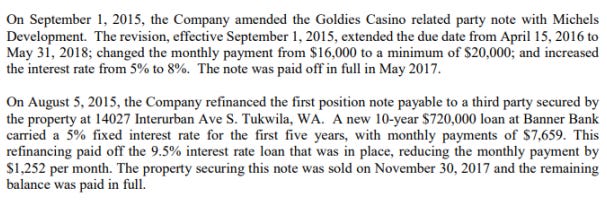

Refinancing of Notes payable.

Purchasing properties that were leased in the past as shown:

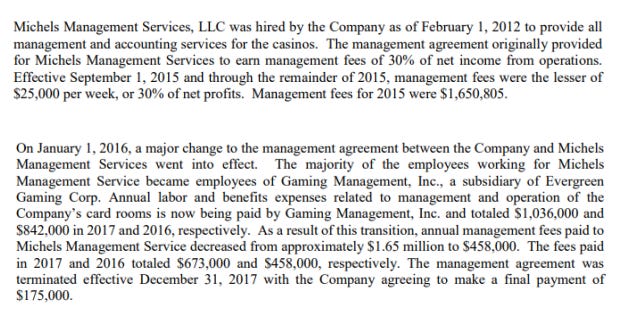

Reduction in service management fees relating to Steven Michels related entity Michels management services as described below:

In recent years the operating margin has contracted due to a minimum wage increase approved in 2016 as described below:

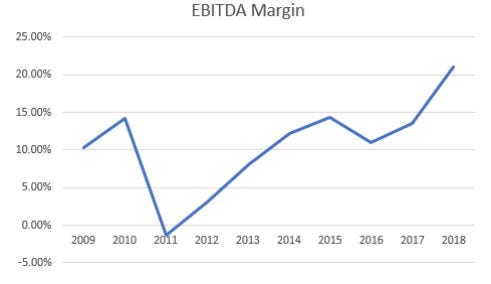

These decisions all assisted in allowing cash flow to make it to the bottom line as a result the EBITDA margin has shown a steady increase in recent years

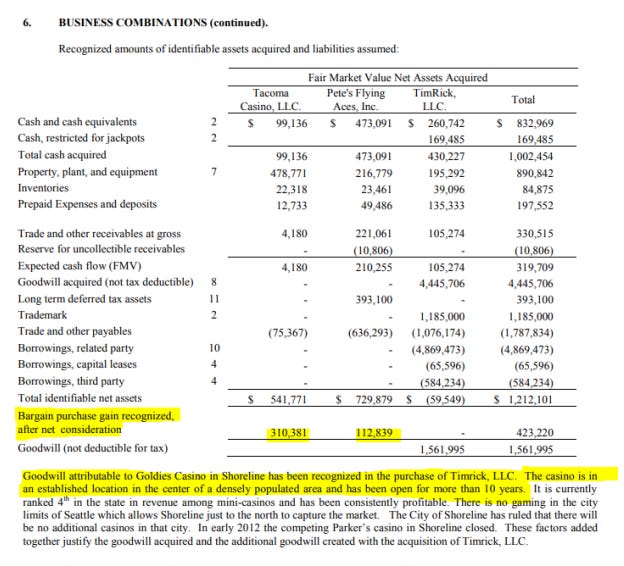

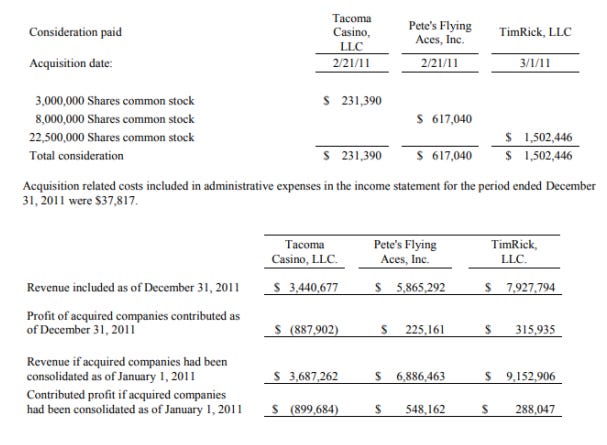

You might see that in 2011 there was a huge fall in the margin, this was the year where the business purchased Chips Casino, Palace Casino, both in Lakewood as well as the purchase of Goldie's Casino on Shoreline with the issuance of company shares. Both Chips and Palace were bought extremely cheap, well below the book value of assets. The details of these acquisitions are shown below.

Speaking as to the value of these acquisitions you could draw the conclusion that:

Tacoma (Chips Casino) was purchased at just 0.42x NTA & 0.06x Sales. however had negative earnings in the 2011 year.

Pete's Flying Aces (Palace Casino) was purchased at 0.84x NTA, 0.09x Sales and 1.12x earnings

TimRick LLC (Goldie's Casino) was purchased at Negative NTA, 0.16x Sales and 5.2x earnings.

It's clear that these were all cheap on a revenue basis, and the improved efficiency of operating expenses has allowed these assets to show their value several-fold. Chips Casino is a particularly cheap acquisition on an asset basis, Palace Casino is a cheap mix of sales, assets and earnings while Goldie's is an advantaged asset that has a protected moat (See the goodwill note above)

As for the profitability of these assets they have all paid back their purchase price several fold, indicating that these acquisitions were brilliant in hindsight. These earnings were reinvested into assisting the efficiency of operating margins as seen in the steady increase in EBITDA margin earlier.

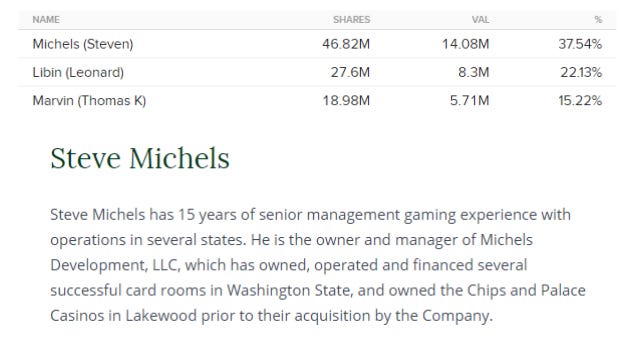

It's clear the fundamentals of this business show a favourable situation, what leads the management to make these sort of capital allocation decisions that have worked out so well? Well first off the management hold a significant stake of the company which is great for pushing them to think about the longterm value of their shares. Of course this carries the risk of a lack of control as well for minority shareholders.

Interesting to note here is that the reason Steven Michels has such a large ownership in the company is due to him being the previous owner of both Chips and Palace Casino's. It's great that the company kept him on as management since he knows them both well.

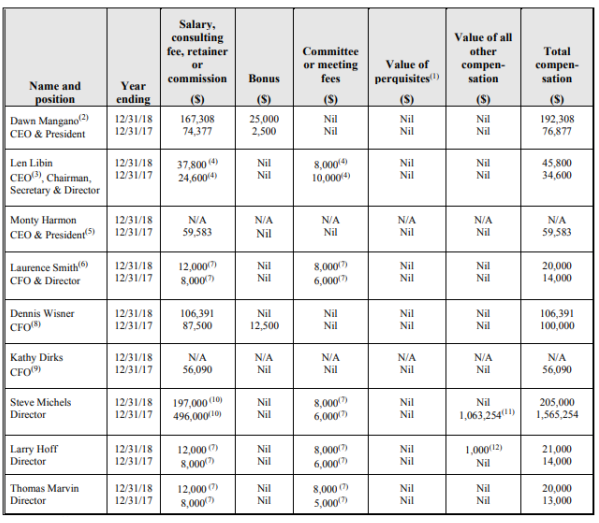

Compensation for management is generally fairly conservative with particular interest in the arrangement of Steven Michel's prior compensation arrangement which was shown earlier in the operating expenses section. The removal of his management arrangement has lead to significant decline in compensation as the employees that were working under this agreement are now working under a subsidiary of Evergreen, removing the need for this arrangement.

All in all, the value of a company can be simplified to the FCF Yield + Growth that one can expect to get, which is essentially the cash flows that the investors expects to receive from the company.

For Evergreen Gaming the following valuation is made:

When compared to the previous 5y Returns the valuation seems much higher than actual returns. This is likely due in part to the FCF yield at the time being much lower than it is now. So a higher entry multiple leads to a multiple contraction diluting the valuation we have above.

Nonetheless at such a high FCF yield, the prospects of the business to generate enough free cash flow for shareholders is very attractive with high quality bargain assets held by Evergreen. The main risk is that of Maverick LLC. Their aggressive acquisition of cardrooms in the state could be pointed towards Evergreen. Given that the purchases were bargain at the time of acquisition this could mean that an offer is above expectations however that is only speculation at this point. Evergreen provides what looks like a very high likelihood of receiving free cash flow to payoff the initial investment within just a few years including the liquid assets on the balance sheet.