Finexia Financial Group (ASX:FNX)

Finexia Financial Group (ASX:FNX)

August 2023

Finexia Financial Group is a diversified financial services business in Australia. It operates in 3 key service lines, Private Credit, Equity Capital Markets, and Funds management. The business was founded in 2014 by its current CEO Neil Sheather before conducting a reverse takeover arrangement with Natural Fuels in 2015 to list its business on the ASX. From here it acquired the Hong Kong listed Mejority Securities, who subsequently sold its HK service line and obtained an Australian financial services licence (AFSL) to provide a variety of financial services to retail and wholesale investors. Since this time, the group has conducted several bolt-on acquisitions in equity markets and professional services, before a transformational acquisition in 2020 of Creative Capital & another of StayCo in 2022 through a rights-issue.

I have been reading announcements from this business for about 14 months now, with the first being the group’s announcement of its 2022 financial guidance. Within this release I saw a rather impressive FY2022 guidance of $3.8m EBIT, which at the time would be equivalent to a pre-tax yield of about 40% of its market capitalisation. Today the price is the same, but the group just booked $4.3m of PBT for the FY2023 year, despite a delay in some loan settlements pushed into the FY2024 year. But perhaps, of the most interest to me, and why I only took a position now, was the implementation of a dividend policy for the group of ~1/3 of its net profit after tax along with the recruitment of the Sequoia financial group founder Scott Beeton to charge distribution to dealer groups. I view these 2 factors as hugely beneficial for the investment case and think that with this and the growth in private credit will lead to rapidly growing earnings and its loan book in the near future.

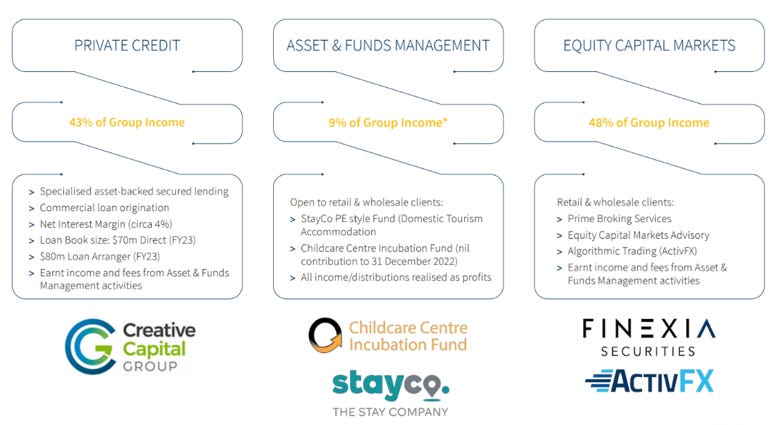

To speak further on the group’s service lines, it draws the lion’s share of its current profitability from the Equity Capital Markets division, which is the legacy business, helping businesses with equity finance, stockbroking etc. There is also a small component of SMSF administration in this service line. Predominately, this business is high margin and accounting profit is closely aligned to cash flow however, it is heavily exposed to the level of activity it experiences in both share trading volume and corporate advisory activity.

Private Credit represents its creative capital acquisition done in 2020. This business is in essence a lending business, with expertise across various forms of alternative financing, but with some 50% of their financing being exposed to residential development and a further 30% to Industrial property. This no doubt sounds quite risky, however, as per the group’s FY2023 guidance the LVR of this division is 45%, and typically these loans have a term of just 12-24 months. Per its most recent figures this division has a $28m loan book with 11.17% borrower rate. The group generates a net interest margin on this of consistently above 5% p.a. The primary risk for Finexia in my view is that the bulk of it’s lending activities across private credit and funds management are unlisted in nature, thereby not requiring frequent valuations. Whilst their current LVR’s are low of 45-60%, it is possible that with the revaluation of the underlying assets that these LVR’s are lower than initially intended and that fund investors, could see their capital impaired if they seek short term redemptions.

Last but certainly not least, the groups funds management arm is by far the most important part, with the group acquiring the Stay Company Income Fund late last year, launching the Finexia Childcare income fund and the Prime Asset Backed Lending. This division has seen the size of the loan book dramatically grow in recent times, with the Childcare Loan book in particular growing from $11.5m in March 2023 to a forecast of $69m in September 2023. Given its borrowing rate of 13.9% and its monthly distributions, the group has seen strong interest from investors seeking yield. There are several articles on their flagship Childcare fund which point to strong structural tailwinds in the childcare sector.. Furthermore, of the listed childcare centre operators, they have predominately been highly leveraged vehicles, which may support the banks hesitancy to lend, and detract from the Childcare lending thesis that Finexia is relying on. Finexia needs to ensure that these loans are properly secured by real assets and strong cash flow generating potential. Thankfully, there is strong government support in this sector including the cheaper child care bill which just passed senate, which is aimed at subsidising child care fees for families and allowing discounts for staff, which indirectly will support volume to generate enough revenue to cover fixed costs and lending expenses.

The Stay Company Income fund (StayCo) operates several properties across southeast Queensland. This business is interesting as StayCo purchases rights to operating the letting business of individual rooms under its own brand, of which have a weighted average term of 19.5 years. These properties include some of the largest apartment blocks on the gold coast including Bel Air & Ivory Palms among others. Importantly, StacyCo does not hold material ownership in any of the properties in its portfolio. This strategic decision allows the company to control a portfolio of quality real estate assets with relatively low upfront and ongoing capital commitments. StayCo seeks to enhance its management interest in properties by strategically acquiring freehold ownership in certain areas (such as lobbies, restaurants, conference rooms). AUM has grown significantly since it’s launch in the group generating FY23 revenue of $12.2m and is expected to generate >$16m in FY24.

My investment into Finexia is the first of several smaller sized opportunistic allocations which aims to focus on opportunities which may not qualify for a primary sized position, and with reservations around Finexia’s service lines, I felt that small sizing was appropriate, however, at a FY2023 Price/Earnings ratio of just 4.5x (2.4x including net cash), a fully franked gross dividend yield of 9.5%, and what appears to be a lot of embedded net interest margin (evident by the massively increased loan book in the 2H), Finexia appears to fundamentally represent a metaphorical home run should risks not materialise.