Gamestop (NYSE:GME) - Deep Dive

Gamestop (NYSE:GME) - Deep Dive

Video Game Retailer

About

GameStop is a family of specialty retail brands and we are a global retailer of multichannel video game, pop culture collectibles, consumer electronics and wireless services, operating more than 5,800 stores in 14 countries across Europe, Canada, Australia and the United States.

GameStop is committed to delivering innovation to consumers anywhere, anytime and any way they want it. Whether looking for new or pre-owned, digital or physical video game titles, the latest in video game hardware or accessories or consumer electronics, gaming and technology enthusiasts are invited to discover and enjoy their favorite products in one of GameStop's welcoming retail environments.

Our buy-sell-trade program provides substantial value to customers looking to trade-in video game hardware and software, or smartphones and tablets they no longer use or play. Each year GameStop provides more than $1 billion in trade credits, with more than 70 percent of these trade dollars being applied toward the purchase of new products.

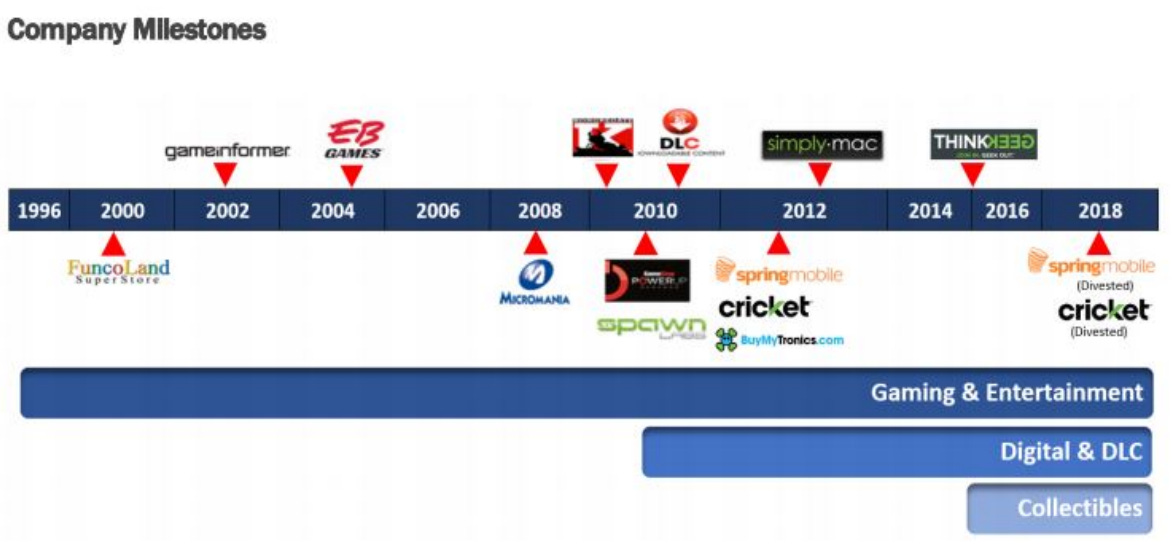

The company's global family of brands include GameStop; EB Games, Micromania, and Game Informer® magazine, ThinkGeek.

Core Values

Each one of our more than 53,000 passionate associates helps shape our company’s storyline and future with their everyday actions.

As we have navigated the path from small software retailer to a global family of specialty retail brands that makes the most popular technologies affordable and simple, the following values have been at the core of everything we do.

We are passionate about serving others, creating great experiences for our customers and our people, and sharing the magic of gaming.

We are empowered to disrupt legacy thinking with innovation and agility, create powerful experiences for our customers, take risks and trust each other on the decisions we make.

We are responsible for holding each other accountable, doing what’s right to contribute to our long-term success and making time to give back in the communities in which we live, work and play.

At GameStop, these core values form the foundation of who we are, what we stand for. They are the building blocks of our DNA, and represent how we serve and protect the GameStop family of associates, customers, shareholders and vendors. We believe that when we all stand together, living these values, our family will be impenetrable to the challenges of the competition all around us.

Catalyst 1 - Microsoft & Sony

With it being 6 years since the release of the PS4 and Xbox one and 2.5 years since the release of the Nintendo Switch, it's obvious that we are at the bottom of the console cycle. With new consoles slated for release late next year, the current levels are likely to not get worse than they currently are. Even now in this late cycle, 90% GameStop's stores remain cash flow positive, a sign that the industry is not quite as moribund as pessimists believe.

Sony and Microsoft announced earlier this year that their next-generation gaming consoles will utilize physical discs. This pro-longs the relevance of Gamestop physical stores significantly. Specifically to note is the release window of these consoles is slated to be 'holiday 2020'. Therefore, we can expect that Q4 FY2020 to be a significant quarter for Gamestop. With this in mind, holding until this period makes sense as at some point Gamestop can capitalise on this opportunity.

Catalyst 2 - Michael Burry Activism

Recently, investor Michael Burry of Scion Asset Management disclosed he owned 3 million shares of GameStop (roughly 3.3% of the company). He also sent a letter to the board of directors urging them to immediately execute the remaining $238 million on their share repurchase authorization. In his letter, Burry said the following:

"As mentioned in our previous letter to the board, we have concerns regarding capital management at GameStop... We submit that when share prices are at or near all-time lows and more than 60% of the shares are shorted despite cash levels much higher than the current market capitalization, lack of faith in management's capital allocation is the default conclusion."

In a nutshell, Burry says he does not have faith in management's ability to allocate capital or turn around the business.

"But what is happening now in the stock is about more than late cycle doldrums or even the streaming paradigm - shareholders do not have faith in current management and have not been inspired by new leadership policies"

So if he doesn't like the business or the management team, why the heck is he buying the stock?

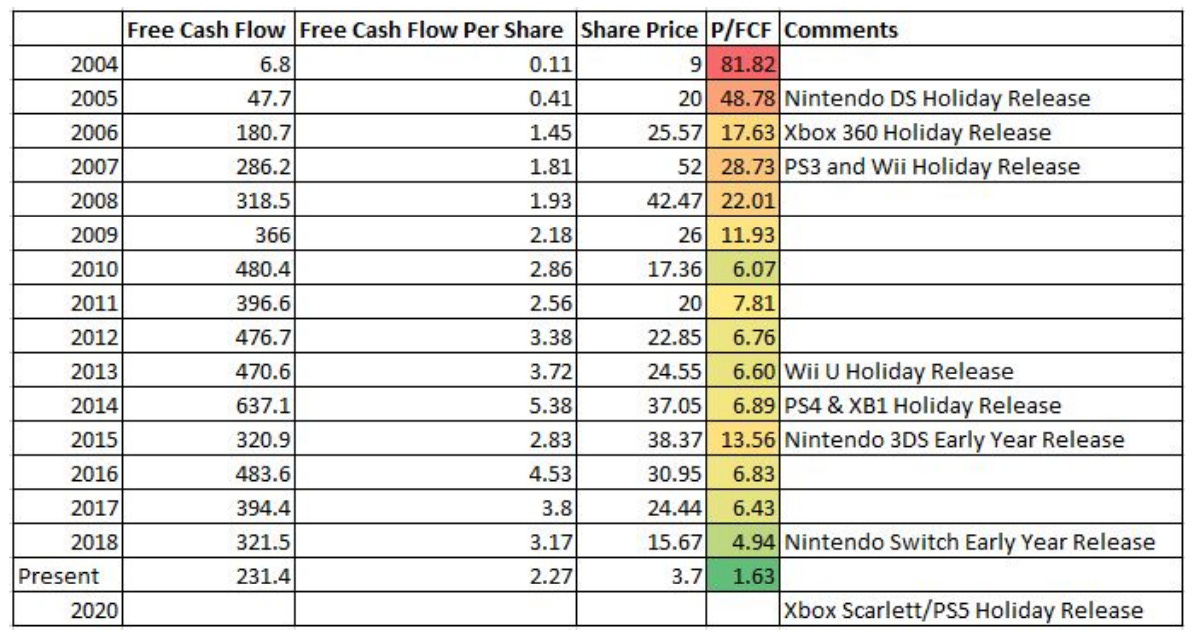

Burry is particularly focused on the generation of cash that Gamestop can dish out. On a historical P/FCF Basis Gamestop is the cheapest it has been ever. With an optimistic holiday 2020 season approaching next year, it could be very possible to see an increase in FCF and hopefully a reversion to a mean P/FCF ratio. The mean is 17 over the last 14 years, however a mean ratio since 2009 may be more relevant at 7x P/FCF. This would imply at current FCF that the stock is worth close to $16 per share at the current time.

Burry's second point deals with the long-run technological trends affecting video game consumption. There is an undeniable long-run trend toward downloading video game content, rather than buying physical game disks. At the same time, sales via alternative channels, such as online retailers like Amazon.com Inc. NASDAQAMZN, threaten GameStop's retail business model. These twin forces have led many analysts to start a veritable deathwatch for the company. But Burry says this is a mistake.

Indeed, while the days of physical video game disks may be numbered, their imminent death is likely exaggerated.

GameStop shares are down 80% from their highs, but Burry believes 2019 will likely prove to be the near-term bottom as next-gen consoles emerge and the cycle revs up. At the same time, Burry sees an opportunity for the company to buy back shares at the current depressed price levels.

"Technical factors driving the stock to lows has created an opportunity for substantial buybacks at below private market prices. There is no better use of capital."

GameStop currently operates under a $300 million buyback authorization, but has thus far bought back only $62.4 million. Last week, Burry took a newly activist tone, issuing a letter to GameStop's board calling for a more aggressive buyback strategy:

"We're at low tide on the cash balance. The balance sheet checks out for me."

With a high level of short interest in GameStop, a surprise to the upside could pop the stock significantly, as could a reinvigoration of its stock buyback program

Risks

GME has over 50% of it's Float being shorted, which could largely explained the distressed stock price and why it is so cheap. If this issue persists the value may struggle to become unlocked and management allowed to continue to destroy shareholder value. However this also presents an opportunity, as a suprise to the upside due to a new console cycle could significantly price up the stock. For this reason it is likely why Burry want's to see a stock buy-back now of all times. The cash generation and depressed prices at 0.38x Book value could easily provide significant value for shareholders.

Dying Business Model - Even despite the Cheap price, it is clear-cut that physical game sales are trending downwards, although i think this is exaggerated, a high short interest and continued declining sales could continue to push the stock down.

Conclusion

Gamestop is currently operating in bottom of the cycle conditions. Along with positive cash flow generation and a significantly depressed stock price due to significant short interest, the best value creation to shareholders is a continuation of their committed buy-back program. Micheal Burry is advocating this. Furthermore, the release of new consoles late next year can provide an expansionary environment for Gamestop to get back on it's feet. With the consoles including physical disk trays, accompanied physical copies will assist this. The business model is no doubt in decline and to hold this stock as a potential long-term business is not advised at all. The thesis is to unlock the stock's value through either buybacks, scaring off shorters or, start-of cycle operational improvements.