Gazprom (LON:OGZD) - Deep Dive

Gazprom (LON:OGZD) - Deep Dive

Russian Energy

About

Gazprom is a global energy company focused on geological exploration, production, transportation, storage, processing and sales of gas, gas condensate and oil, sales of gas as a vehicle fuel, as well as generation and marketing of heat and electric power. Gazprom’s strategic goal is to establish itself as a leader among global energy companies by diversifying sales markets, ensuring reliable supplies, improving operating efficiency and fulfilling its scientific and technical potential.

Strategy

Diversify Export routes into Europe and China with market share targets of 35% more in Europe and 13% in China

Further strengthen their Russian position in gas.

Already a leader in environmental carbon footprint with more goals in the works.

Business Moat

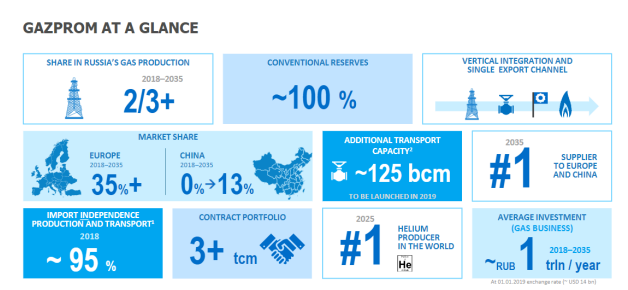

Gazprom has a huge presence in the energy industry, holding 16% of the worlds natural gas reserves and 71% of Gas reserves in Russia . In addition to this, Gazprom accounts for 12% of Global gas output and 69% of domestic output. To top it off, Gazprom ranks No.1 in the world in thermal gas production and is 3040% owned by the Russian Federation. This puts in Monopoly status in Russia and a key player internationally.

Using help from the Government, Gas produced by Gazprom Subsidiaries is sold mostly at prices fixed by the government, however they have been working at deregulating the pricing of Russian gas, allowing Gazprom and subsidiaries to use unregulated wholesale prices in respect of natural gas produced by these entities. This should allow them greater cost competitiveness and further build their status as a reliable supplier.

As a result of Gazproms aggressive capital expenditure and strong operations, it has consistently grown it's revenues at an annual rate of 9.2% over the last 10 years despite a slump in demand for energy commodities. Given its geographical diversification advantages, Gazprom is targeting the Asian market and predicts it will be the world's largest natural gas consumer by 2035. It expects a 15% global growth in energy consumption, 2/3 of which from Asia and also significant growth in emerging markets. These represent strong economies of scale for Gazprom going forward.

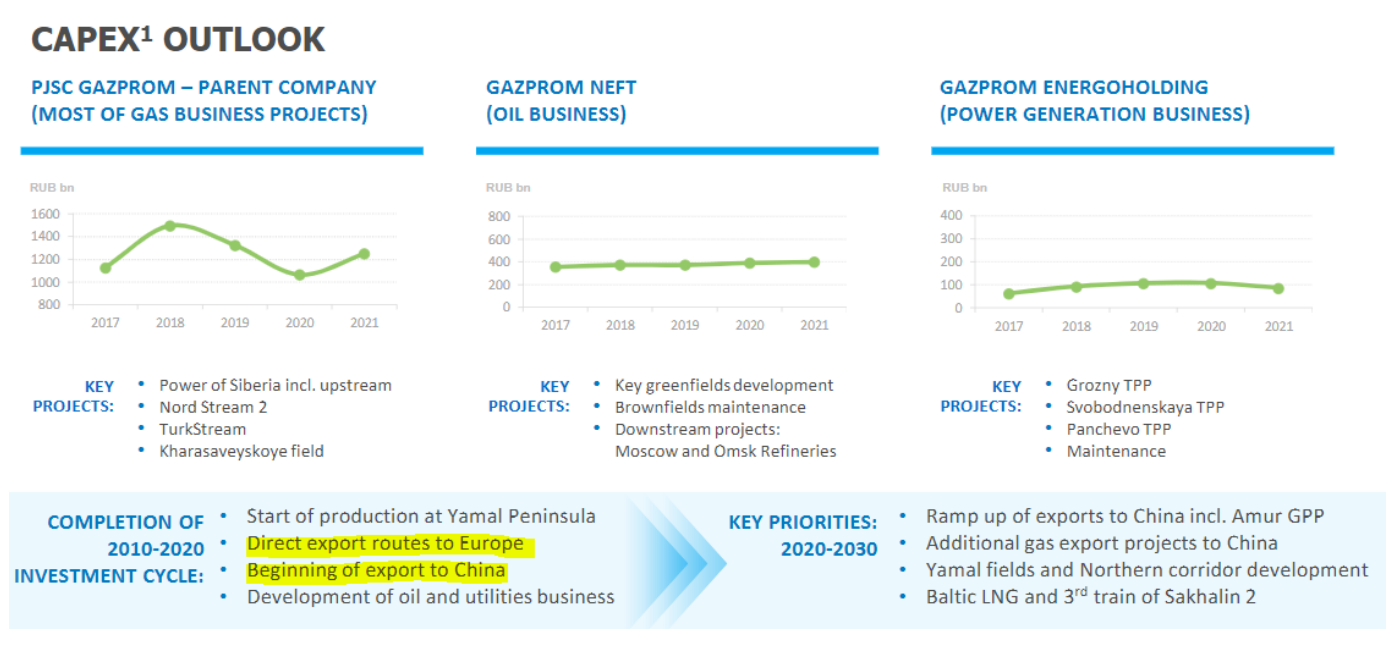

Capital Expenditure

Despite an increasing rate of capital expenditure, free cash flow has managed to continue growing. This is the very essence of sustainable growth, shall management maintain this style of growth, returns to shareholders in the form of dividends should grow along with capital appreciation.

There is a multitude of investments in place despite the dividend that was announced being double of the previous dividend.

Dividend Policy

Gazprom states that they intend the raise Dividends year after year while maintaining sustainable Free cash flow. Management has a very good track record, growing it's dividend almost every year since 1994 with the exceptions of 1998, 2008 and 2009.

Risks

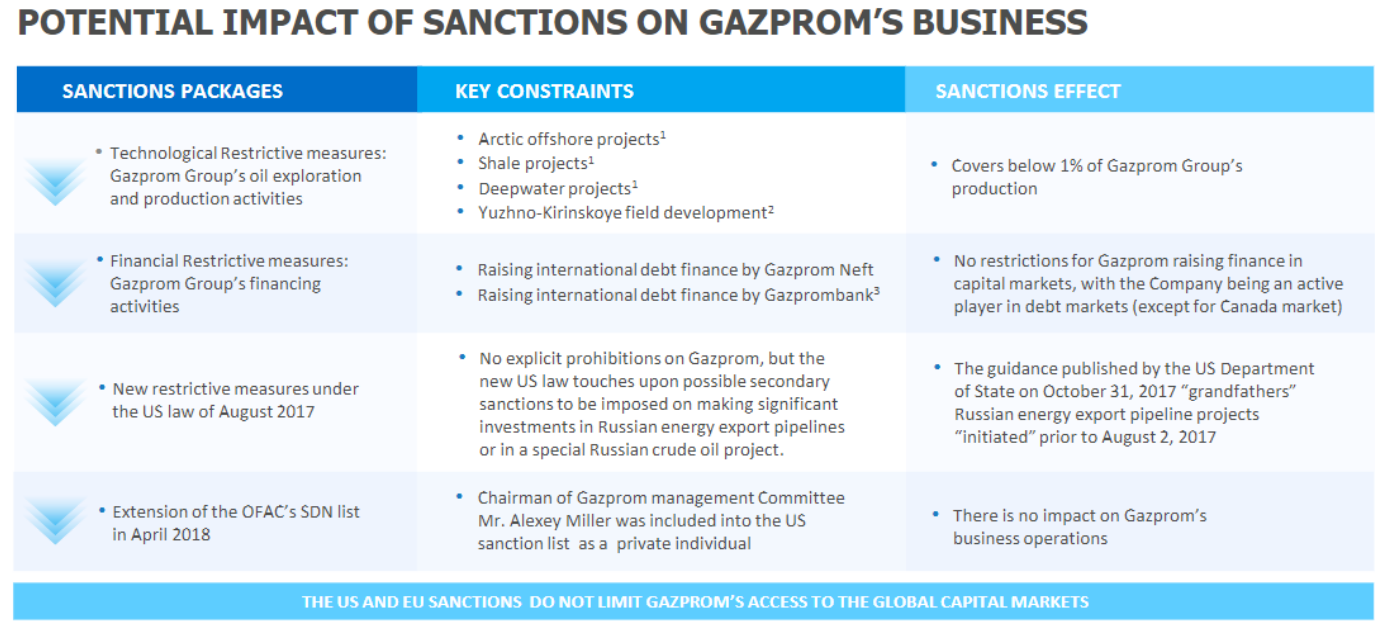

As Gazprom is a Russian based company in addition to being part-publicly owned, it is extremely important to address the risks. Gazprom has addressed risks relating to sanctions in their recent 2019 Investor day presentation.

In addition to this, Key risk factors along with mitigation strategies are outlined in the corporate governance section of their investor centre.

For example, Gazprom addresses a global economic risk by diversifying sales channels and optimises leverage to maintain financial stability. European market risks are managed by utlising flexible long-term contracts and build infrastructure to bolster natural gas demand.

It is clear that risk is managed exceptionally well and that Gazprom is well positioned to excercise action quickly according to plan.

Fundamental Analysis

Key takeaways:

Valuation Ratios are very cheap, however, this has been an historically cheap stock over the last 10 years identified by the low Shiller P/E Ratio. Despite this all TTM ratios are well below both the 10y and 5y averages.

Margins are all extremely attractive at historically strong levels.

Conservative debt, easily paid off using Free cash flow, This leaves Gazprom plenty of room to leverage if it needs.

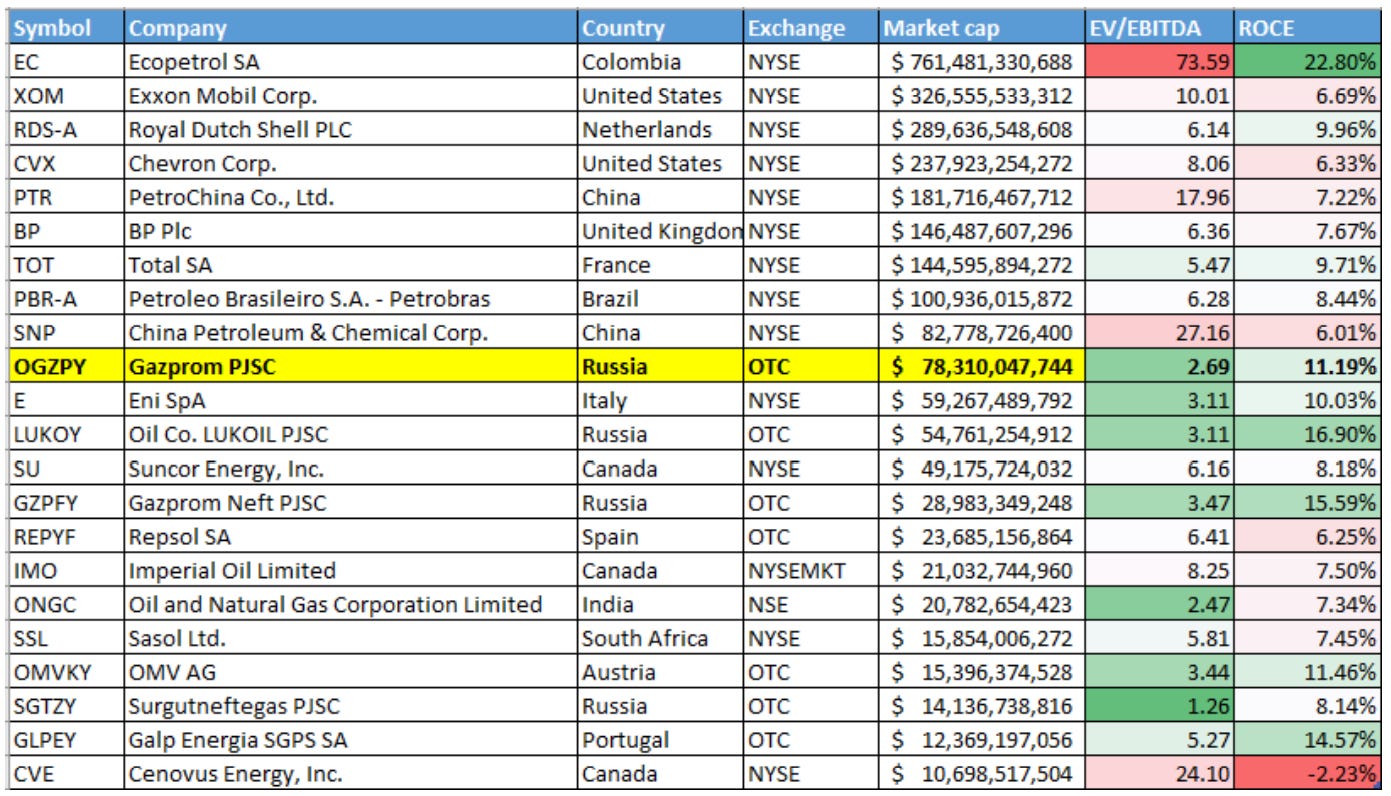

Peer Comparison - Fundamentals

Gazprom PJSC and it's subsidiary Gazprom Neft both have attractive Returns on capital and EV/EBITDA. In terms of Market Capital Gazprom is the 10th largest in the sector. However, with the backing of the Russian Government, Gazprom can seem to have a huge amount of power. Given the uncertainty in the european markets, Gazprom looks depressed in valuation and hence the attractive ratios.

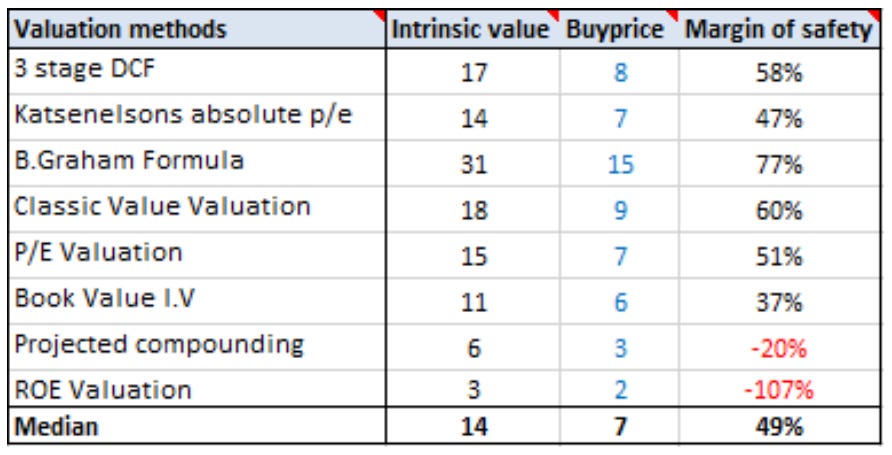

Intrinsic Value

Assumptions:

Book Value Growth = 8% (Payout ratio will increase, therefore 8% seems Conservative)

FCF/EPS Growth = 10% (Capex will remain around the same level)

Margin of Safety = 50% Preferred (Conservative)

Discount Rate = 15% (Conservative)

Payout Ratio Increases by 10% each year until 50% in 3 years time

10y Median Margins at 15%, 10y Median PE at 4

3% Risk-free rate.

Gazprom carries a large margin of safety on the current price, allowing me room to be comfortable with sovereign risk in the hope of exponential capital and dividend growth in the coming years.

Conclusion

With a growing payout ratio despite aggressive capital expenditure, Gazprom is utilising it's Free cash flow excellently by diversifying into asian and European markets. This will allow Gazprom to compound it's equity and has intent to pass on the excess earnings onto shareholders by increasing it's dividend year over year. As a business, the company is an excellent long-term realisation of value and is preparing itself to engage risks head on with full transparency of it's actions. I see this depressed stock price as misplaced and even if the market is correct in some way, attaching a large margin of safety will make up for my misjudgement. This review is to re-done on the 4/06/2020 If i have not sold the stock.