Getbusy (LSE:GETB)

Getbusy is an LSE-listed software holding company that currently owns several Document management software products geared towards accounting firms. It was the result of a spin-off from the ASX-listed Reckon (ASX:RKN) in 2017 and has been on the AIM exchange since.

Its primary products include Virtual Cabinet which is provided to mid-large accounting firms in the UK and Australia in addition to Smartvault, provided to small accounting firms in the US. There are also several emerging products including Workiro, a Netsuite app aimed at plugging the poor Document management functionality inside Netsuite and Certified Vault, a Smartvault add-on which aims to allow for the provision, storage, and distribution of so-called e-document contracts.

The group’s current executive team consists of Daniel Rabie (CEO) and Paul Haworth (CFO) along with 4 members of the Board including Daniel’s father Clive Rabie, both of whom came over directly from Reckon at the time of the spin-off. Clive and Daniel own a collective 20.4% of the company, whereas the Reckon founder Greg Wilkinson also owns an additional 7.4% of the company. All up, members of the Reckon and Getbusy board and executive team own around 30% of the company.

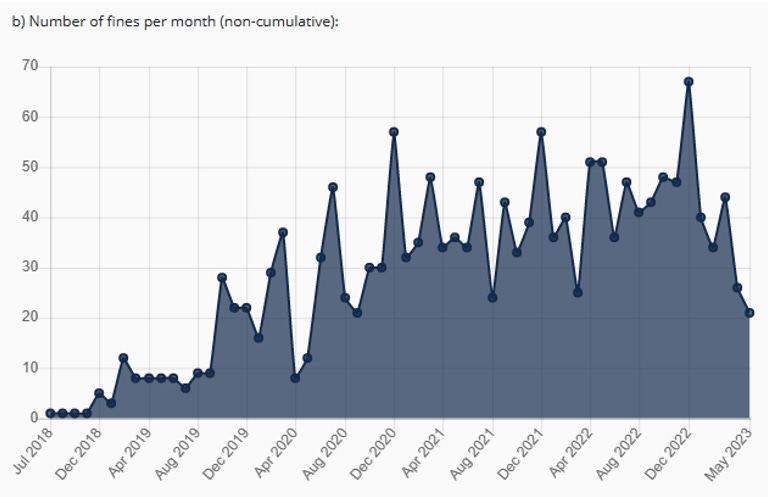

On a macro level, all Getbusy’s services will benefit greatly from the data privacy driven GDPR style legislation that is permeating throughout the world, particularly so as state legislation is plotted across the US will Smartvault see continued growth in its customer base. As of May 2023, there is just 9 states in the US with signed bills that have passed through government, with 41 states having no such GDPR style legislation.

The number of non-compliance fines issued in the enforcement of the EU legislation has continuously risen since the introduction of the act, which is an incentive to further increase the penalty for a breach, in turn driving businesses to take data privacy seriously as a result.

Financially, Getbusy operates as a SaaS business model where they receive cash in the form of monthly and annual subscription payments. Given the reasonably large discounting available for annual cycles, it is unsurprising to hear that some 70% of Getbusy revenue is received annually in advance. That means that cash revenue is consistently higher than reported revenue as a result, and the more growth they report, the wider that the gap should be ordinarily.

The cost base is managed so as to report an accounting profit of close to NIL as possible, with 24% of revenue invested into it’s customer acquisition associated sales and marketing expenses in order to grow it’s customer base. Furthermore, the group has historically invested some 10% of it’s revenue into non-revenue generating software, namely Workiro. I would consider these investments as a capital allocation decision and the group’s claim that it could reach >30% EBITDA margins on a group basis at maturity to be feasible as a result. In fact, Virtual cabinet is already generating NPBT margins of ~50% on a standalone basis (pre-corporate costs)

Like Reckon, Getbusy has recently introduced a ‘Cash Distribution Incentive Plan’ which for management is much more appealing here than it is at Reckon, making the incentive particularly strong in comparison.

In the event each of these thresholds is met, net of incentives shareholders would see £57m, £95m and £121m respectively. Importantly, the plan is in place for 7 years and does not specifically state that it cannot just be a partial sale, therefore any individual part is up for grabs.

Knowing this, Getbusy, at our cost basis of £0.67 trades at an enterprise value of £30m and generates ARR of $21.3m, a multiple of 1.4x ARR on a non-diluted basis. Getbusy may trade on a normalised EV/EBITDA of just 4.7x with the believable prospect of >30% EBITDA margins at a steady state. Furthermore, with management targeting £30m in ARR by 2026, the compounded rate creates a hold-return that exceeds the hurdle rate set by the trust. Optionality exists with the CDP incentive as well with a minimum CAGR of 9% in the event the business is sold for just £70m (assuming it takes them 7 years to do so, and they are at the lowest band). Either way, the odds look bright, and incentives are strong to the point that it is difficult to envision a scenario where the Hurdle Rate Unit Trust did NOT make money on this investment.