Globe International (ASX:GLB) - Deep Dive

Globe International (ASX:GLB) - Deep Dive

Skate-wear Retailer

About

Globe International Limited is a global producer and distributor specializing in purpose-built apparel, footwear and skateboard hardgoods (decks, wheels, trucks, etc.) for the boardsports, street fashion and workwear markets with products sold in more than 100 countries worldwide. Founded in 1985 by three Australian brothers, Globe International’s core business is divided between proprietary brands, licensed brands and distributed brands.

Globe International is listed on the Australian Securities Exchange and operates in Australasia, North America, South America and Europe with offices, distribution and manufacturing centres in Melbourne, Sydney, Gold Coast, Los Angeles, Hossegor, Newport Beach, London and Shenzhen. The company is structured into six business divisions: Globe, Dwindle Distribution, Salty Crew, Hardcore Distribution, 4Front and FXD. The company also has a number of branded retail stores in various territories.

PROPRIETARY BRANDS

Over the last two decades, Globe International has developed its own in-house proprietary footwear and apparel brands – these are trademarks owned by Globe International Limited for the worldwide market and are sold direct and by third party distributors around the world.

Globe

FXD

Salty Crew

Dwindle

Enjoi

Blind

Almost

Darkstar

Tensor

Dusters of California

Impala Rollerskates

THIRD PARTY BRANDS

Globe International maintains diverse licensing and distribution of leading third party brands for the Australian and New Zealand markets through its Hardcore Distribution and 4Front divisions. Hardcore is Australasia’s largest skateboard distributor of over thirty leading brands.

Stüssy

Obey

XLarge

Kryptonics

Andalé

Girl

Chocolate

Thrasher

Flip

Royal

Lakai

Alltimers

Wreck Wheels

The National Skateboard Co

Key History

In 1995, Globe International established its US operation in Los Angeles, where the Globe brand is now a part of the American boardsports sub-culture and a key supplier to major retailers of boardsports apparel, footwear and skateboard hardgoods.

In 2001, Globe International listed on the Australian Stock Exchange and achieved the Initial Public Offer goals. In 2002, Globe International acquired Kubic Marketing, a holding company that owned World Industries and Dwindle Distribution, which at the time, was the parent company for skateboard brands such as Enjoi, Blind, Darkstar and Tensor. Acquiring Dwindle, a company founded by professional skateboarders Rodney Mullen and Steve Rocco, made Globe International one of the world's biggest skateboard companies. In 2003, Globe International established its European headquarters, located along the south-west surf coast of France in Hossegor. As of 2017, the European office sells directly in the major boardsports markets of the UK, France, Germany, Spain, Portugal, Belgium, Netherlands, and Austria, among others. All other significant markets in Europe are serviced by third-party distributors.

Having established a stable of proprietary brands and an international distribution network in 2006, Globe International made a strategic decision to divest itself of its licensed Australian Streetwear Division to Pacific Brands and focus on further international expansion of the company's proprietary brands. In 2009, Globe International added to its brand portfolio by acquiring Europe's number one skateboard brand Cliché and expanding it through international markets. In 2010, Globe International re-entered the Australian streetwear market and established a new division entitled "4Front Distribution", a company that is currently responsible for the Australian distribution of brands such as Stüssy, Obey and Misfit. In 2012 FXD, Function By Design, a new proprietary workwear brand is launched in Australia.

Strategic Vision

Adapt and improve traditional brands where they have underperformed, as well as aim to bring up the bottom line of American and European divisions. Continuing to invest in and leverage brands that are delivering financial performance today, we are also investing in new brands and initiatives.

This sets us up with an ongoing cycle of both seeded and growth brands, with the goal to sustain the stable, solid results improvement we have seen from the company for several years now. We are as conscious today of this year’s financial performance as we are of ensuring we are implementing branded investments to provide growth and prosperity for future years.

Share Price

Financial Performance

Valuation of the company is very cheap in comparison to prior years. Growing competition and a questionable position in the industry has pushed the share price down to

As can be seen here, margins have grown consistently since the 2015 financial year, as has the share price.

Dividends

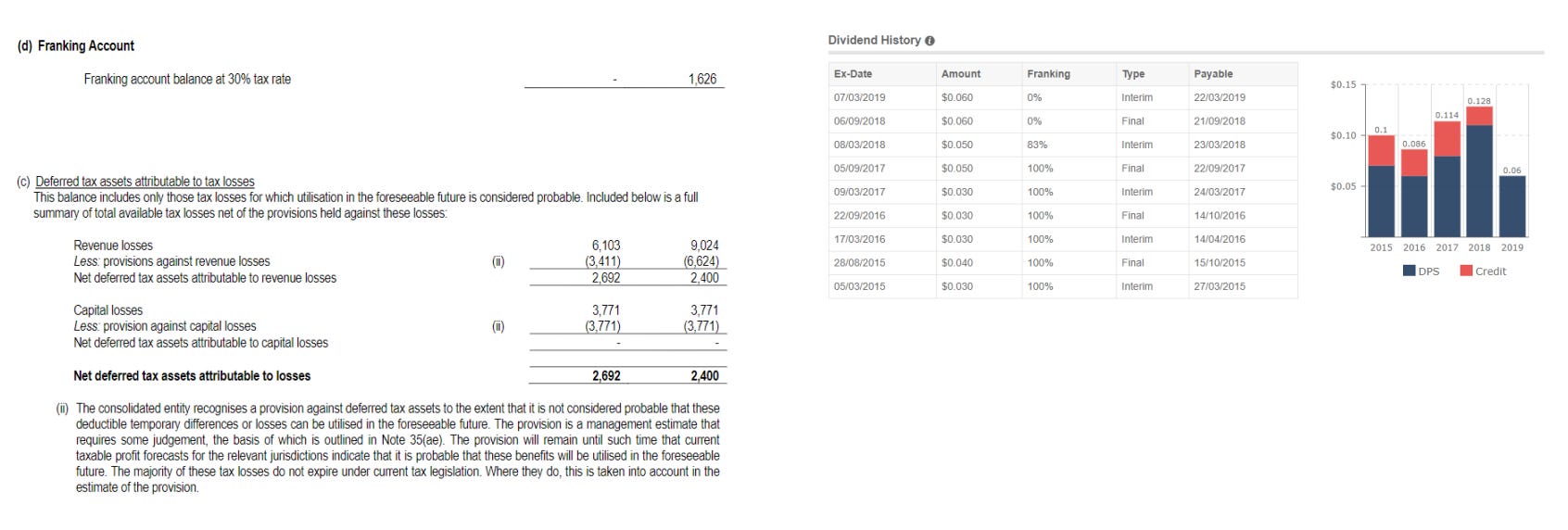

Dividend yields have been attractive remaining at about a 50% payout ratio for the last few years. However as of 30 June 2018, their franking account is $0, therefore they can not pay franked dividends. Given their international distribution of revenue, only australian tax carries the imputation policy, so it may take some time to build franking credits back to a point where sustainable franking credits are possible again.

For this reason, i would prefer to see some sort of buy-back program and deem this as a better use of capital. Or dropping the payout ratio and reinvesting more of the profits.

Furthermore, Globe has over $2.6m in carried forward tax losses to utilise. Given their 2018 profit of $8.4M, at a 30% tax rate, these losses could offset atleast another year of tax. Therefore they may not pay franked dividends for atleast another year.

Share Register

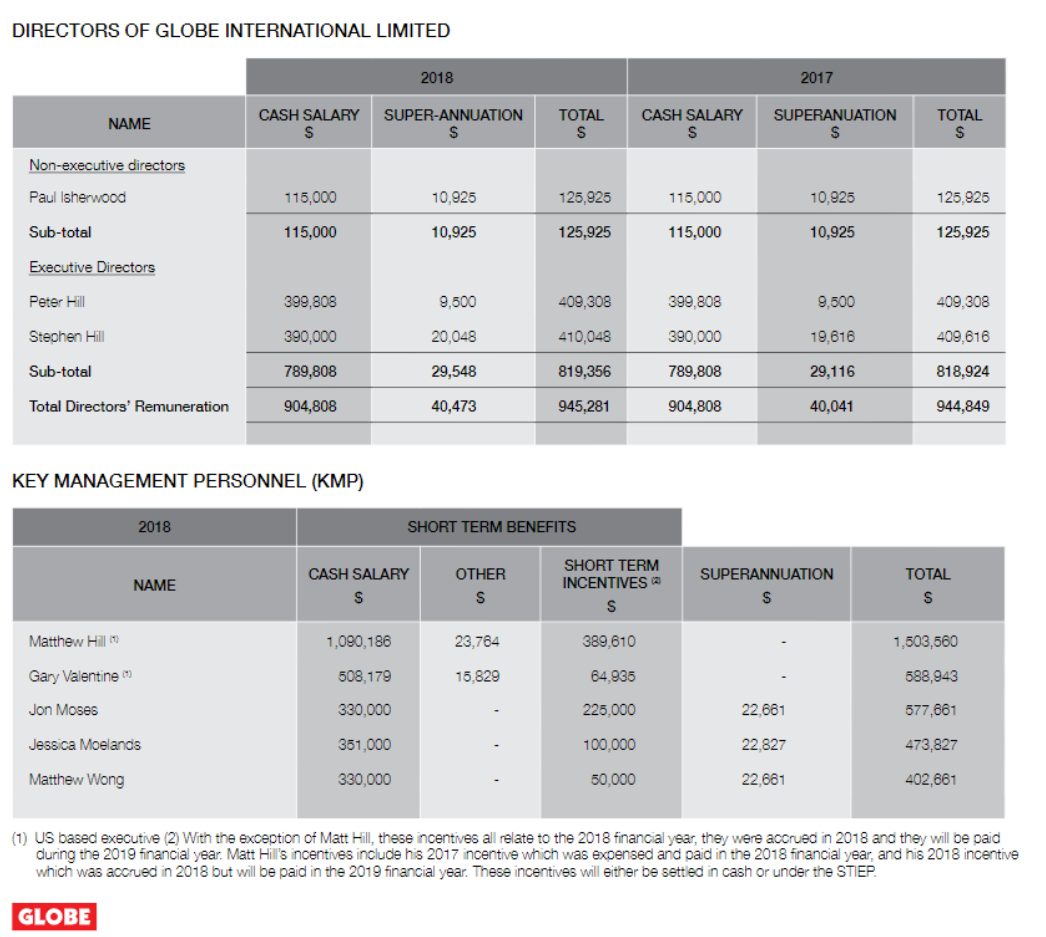

The Hill Family are all executive directors of Globe International Ltd, owning 68% of the total stock outstanding. This is excellent alignment of interest with shareholders.

Furthermore, Billionaire Solomon Lew is hold's the 4th largest holding in the company and has been on the register for over a decade. He is the Chair at premier investments, a company specialising in Retail, consumer and wholesale investments with whole ownership in the Just Group and a significant stake in Breville.

Directors also have little trading activity, given their substantial stake, it is understandable they do not continue to buy more on a regular basis. Yet despite this, the track record is still purchase of stock only.

Management Remuneration

The Management remuneration report in 2018 is an issue that has been voted against at the 2018 AGM and received a first strike in 2017. It seems a large amount of shareholders aren't happy with this policy.

The perilous actions of management in setting remunerations at borderline too high amounts is a risk that could lead to management spill in the future should they value themselves too highly. This could be justified if the business grows strongly, but still a risk to be aware of.

Given 70% of the register is held internally, displease on remuneration could be linked to internal conflict rather than business performance. but the question is whether that distracts management from running the business properly, or merely creates an opportunity for investors

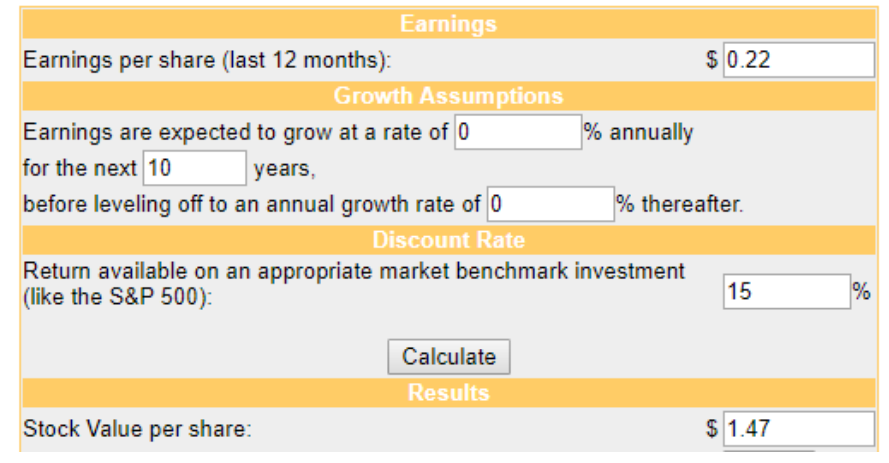

DCF - No Growth

Assumptions:

EPS TTM = 0.22 Per share

Earnings growth = 0%

Discount Rate = 15%

Discount Period = 10 Years

Globe is priced for no growth. I say this because despite my conservative assumptions, i still receive a price that is only slightly below the current share price.

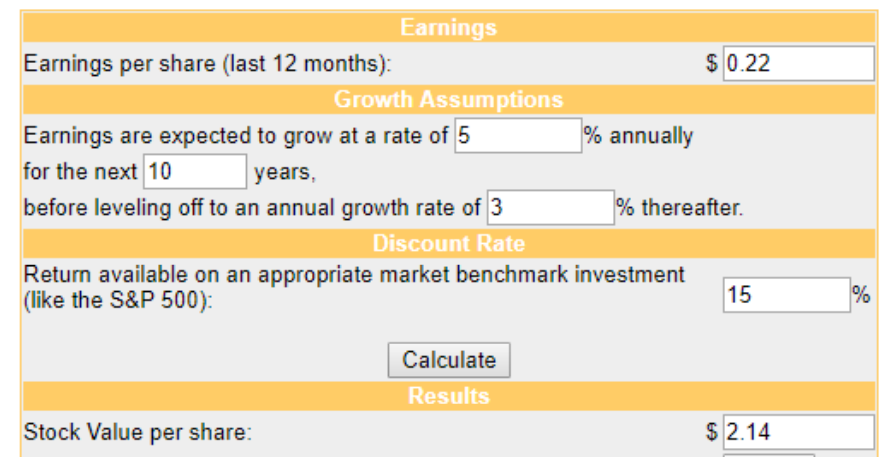

DCF - 5% Growth

Assumptions:

Same as above

Earnings Growth = 5%

Inflation = 3%

If i were to attach a small 5% earnings growth with growth that equals inflation thereafter, the company value represents a margin of safety of 27%

DCF - 50% Margin of Safety

Assumptions:

Same as above

Earnings Growth = 11%

Inflation = 3%

To meet my preferred margin of safety of 50%, 11% growth is needed.

Conclusion

Globe International Ltd is currently trading at an attractive price given it's recent growth prospects and brand transformation/introductions. Management is predominately Family owned with the Hill family owning almost 70% of the float, proving reassuring in incentive alignment. I would like to see allocation of free cash flow flow into reinvestment into the business rather than unfranked dividends. Some risks that are involved are general aggressive competition, declining skate brands, macroeconomic conditions and executive remuneration.