Hitech Group Australia (ASX:HIT) - Deep Dive

Hitech Group Australia (ASX:HIT) - Deep Dive

Australian ICT Recruiter

Company Profile

The HiTech Group is Australia's leading specialised ICT contracting, consulting and recruitment organisation. HiTech provides services to Australian and international organisations and has more than 26 years experience in the industry. Our clients include Federal & State Government departments.

We have a unique recruitment & consulting system supported by an extensive proprietary candidate and client database that we have developed over two decades. We call this intelligent system or tool, HiBase. HiBase has proved, time and time again, to be the key differentiator between HiTech and our competitors. It is our leading-edge cloud based platform that allows us to serve our clients, quickly and effectively, in this rapidly evolving digital age.

The HiTech Group, via its Talent Service business, HiTech Personnel, has expertise in sourcing the best professionals in ICT, Finance, Office Admin and Sales & Marketing. We have been developing our search and selection system for more than 20 years.

As a founding member of the Recruitment & Consulting Services Association Australia & New Zealand RCSA, HiTech has pioneered many processes to improve recruitment, meet candidate expectations and ensure client satisfaction. Today, many of these processes have become industry standard.

We are proud to be of service to the Australian Government providing ICT contractors for many high profile and often highly classified projects.

We are driven by enabling our candidates and clients to succeed and will continue to provide excellence in recruitment and consulting to our clients, candidates, contractors and business partners.

Client Base

Several Federal Government Departments have apointed HiTech as a preferred panel member for the provision of ICT contractors.

We provide contract and permanent staff to over 23 Federal Government departments

Government (Partial)

Australian Bureau of Statistics

Department of Human Services

Australian Communications and Media Authority

Department of Industry

Department of Education | Department of Employment

Department of Immigration & Border Protection

Department of Social Services

Department of Veteran Affairs

Austrade

Department of Education and Communities

AUSTRAC

Department of Infrastructure

Private Sector (Partial):

AT&T

Bupa

Sage

Micropay

Sungard/FIS

The Good Guys

In addition to this diversified client base HiTech has a long history and robust working partnership with its key established clients, predominately in the Government sector

The value these long-term relationships provide to shareholders is reliability and durability of revenue. This allows Hitech to focus efforts on organic growth opportunities and client acquisition.

Strategy

So while revenue looks to be somewhat reliable in nature, the question remains, how is Hitech looking to grow revenue? This is outlined below:

Expanding service offerings comes naturally with long-term relationships. A popular mandate in professional services is particularly the 'Know your client' rule. By doing so you can anticipate and cater to their needs fluidly, keeping them pleased as a result. This has the added benefit of a network effect via word of mouth relationships. Of course this is but an ethos, the importance of knowing the clients you service can't be understated.

As would be expected their is general trend in the ICT space and innovation driving demand in the areas below:

These all provide a bucket of candidates to choose from, and with the lessening need to hire on-site employees, the project-specific contractor relationship is proving dominant

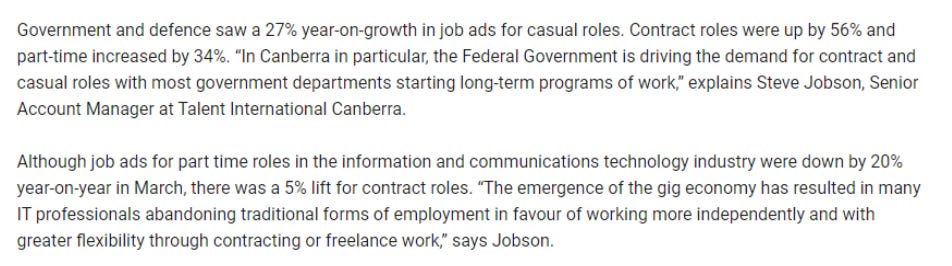

The below SEEK employment trends excerpt (as of EOFY 2018) discusses the emergence of the gig economy and importance of flexibility in engagements

As firms continue to downsize their full-time work forces, the use of outsourcing and contracted workforces will continue to grow. This combined with forecast strong growth in the ICT staffing levels ensures HiTech is well placed to capitalise on these longer-term trends.

This begs the question, how can Hitech capitalise on these labour trends? The answer comes down to both the services team of the company and more importantly 'Hibase', their proprietary database of ICT talent to utilise for positions. Hitech states they have over 360k potential candidates on this database with a predictive intelligence tool of which much of it is not yet monetised. In addition to this tool, they offer a service to clients called "Project Delivery as a service". The key traits of this are:

A perpetually Fit-For-Purpose Project Delivery Model, managed as a Service;

Project Delivery as a Service that offers you access to resources and tools at a flexible and predictable cost, via a fully structured Managed Service, underpinned by KPIs and SLAs;

Whether it's Skilled Resource Provision or a fully Managed Service, PDaaS can help client’s maximise their project success and improve IT project delivery times; and

We offer the ability to have on boarded resources available based on the demand curve of a clients’ portfolio.

While these technological tools are great for efficiency, Hitech insists that the human element is critical and irreplaceable whilst also being high volume/low margin with simplistic 'matching'.

Potential for M&A activity tie into the highly fragmented market that Hitech operates in. The reason for this large fragmentation is the low-barriers to entry that Recruitment offers. While this reduces pricing power, with the strength of Hitech's balance sheet, selectivity can be fully exercised when considering opportunities. This is much the same as the Accounting market and Kelly+Partners acquisition opportunity. Albeit Brett Kelly is much more active in his Growth strategy than Hitech is.

Management

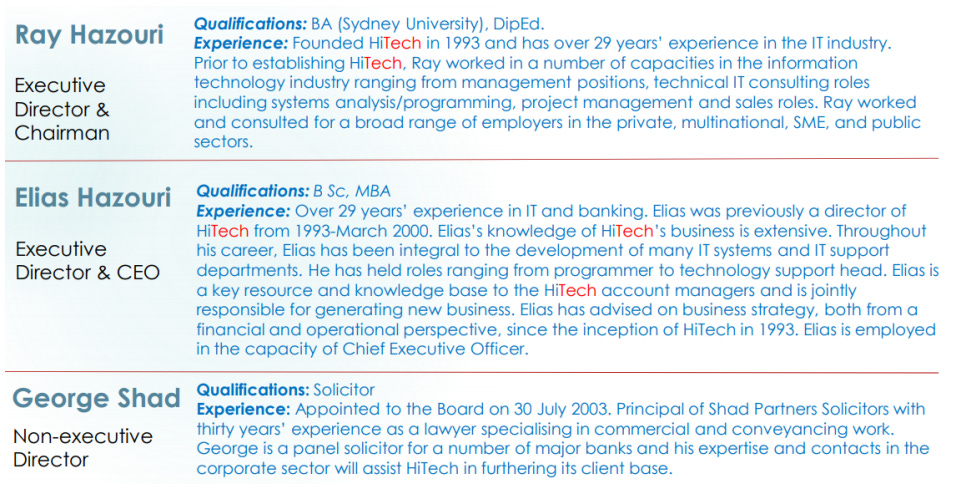

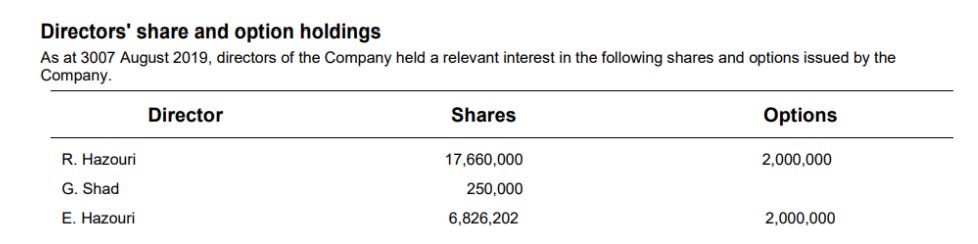

As can be seen above, the company only has a handful of directors, the majority of which are executives and have a large interest in the company as shown below:

The interest is particularly important as without the existence of an independent board/chairman their is no one to exercise objective opinion. However this can be nullified by their interest in the company operations. It's clear that the majority of the Hazouri wealth is in the company, and with founders on board, it provides reassurance that the directors are inclined to grow the company and continue to do so.

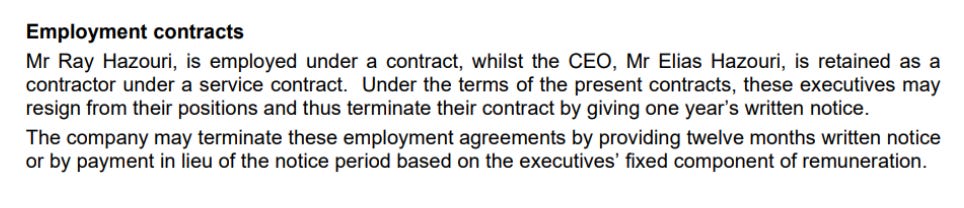

Of further importance is the employment arrangements with these directors. I will use the recent example of Collection House ASXCLH in that Anthony Rivas tendered his resignation and left effective immediately on the 24th November 2019. The market was notified of this on the 25th of November 2019 to which the stock plummeted on that day. The above disclosure that these directors need 1 year written notice is further assurance that the CEO won't exit suddenly and the transition will be disclosed well in advance.

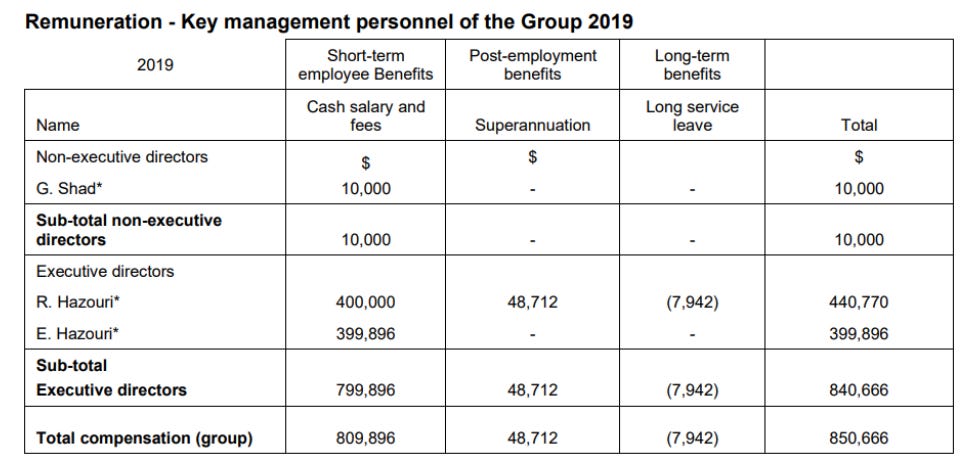

Lastly, the remuneration of directors is quite conservative on their base package given their involvement.

$400450k for each executive director is fair given their involvement in the company. Notably, G Shad and E. Hazouri are both paid to a business structure hence the absence of superannuation.

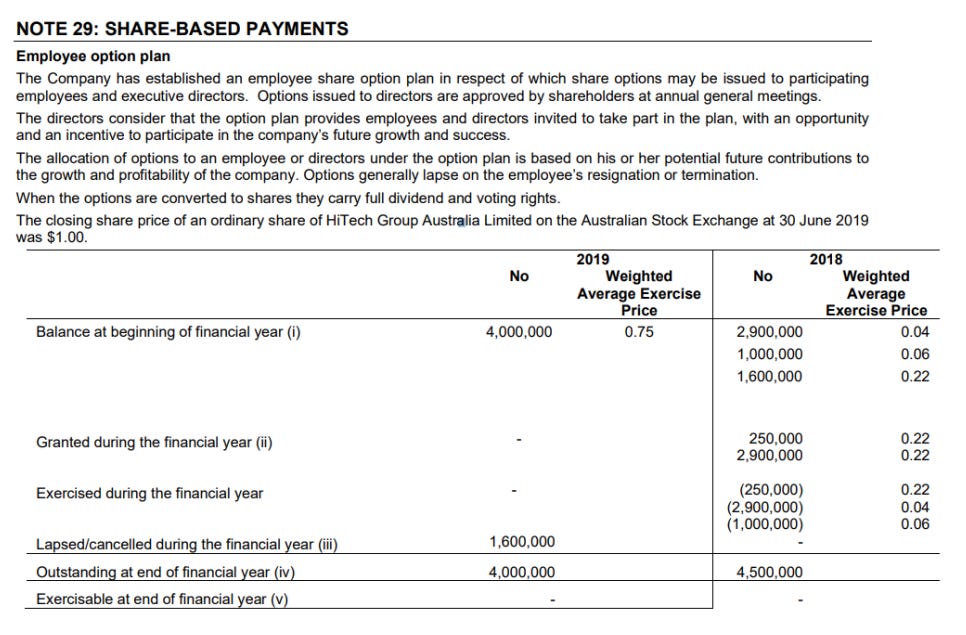

An Employee option plan also exists, of which all of it has gone to just Ray and Elias.

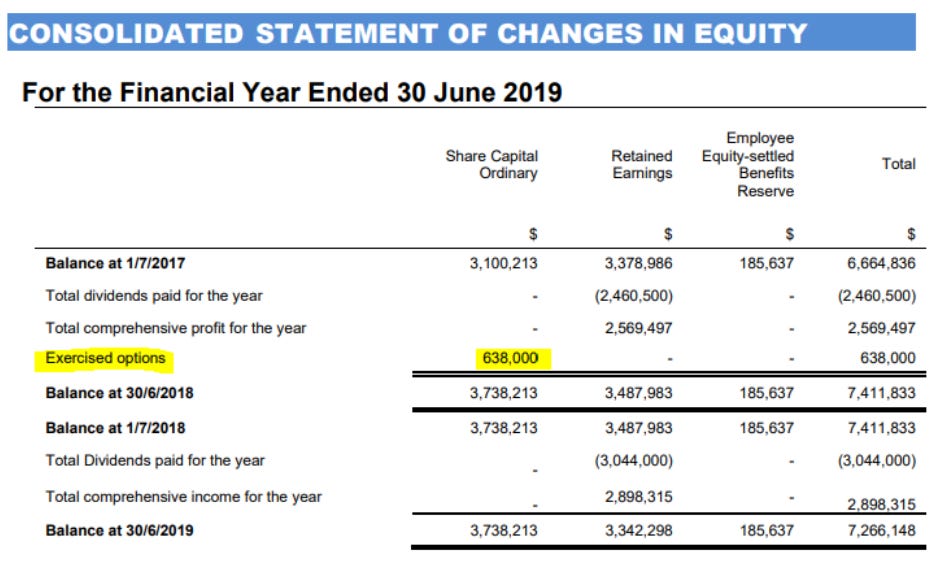

Notably, there is an absence of further dilution recently with no exercising of those options occurring in FY19. If this trend continues, it bodes well for shareholder yield in the coming years. Nonetheless valuation will take into account the diluted shares to accommodate for the options outstanding.

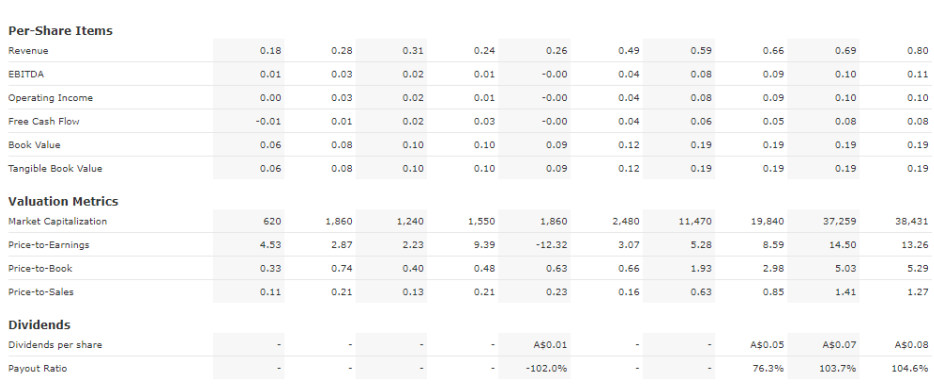

Fundamentals

Using the above information, you can see a few notable traits I consider to be valuable.

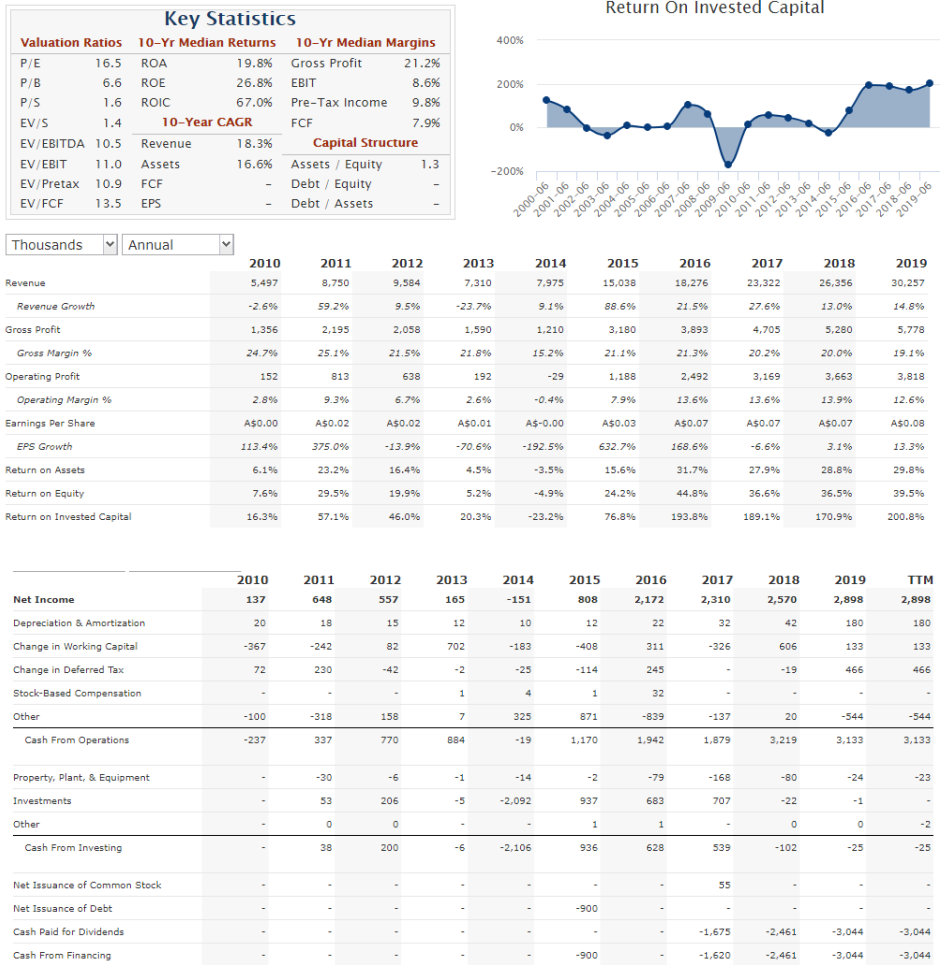

Revenue CAGR over the past 10 years is somewhat consistent, with growth particularly consistent over the past 5 years.

Gross profit margins fluctuate between 15-25%

Operating margins fluctuate between 0-15%, of which recent performance is on the higher end.

EV/S is lower than P/S, which is representative of the fact HIT is Net cash $6m.

10y Margins all are quite favourable

There is essentially no maintenance capex in the cash flow statement.

All free-cash-flow is paid out as dividends in the past 3 years and represented by no movement in book value. Despite this, revenue still grows, leading to a rapidly growing dividend yield of which is dependent on the maintenance of the free-cash flow margin and revenue growth.

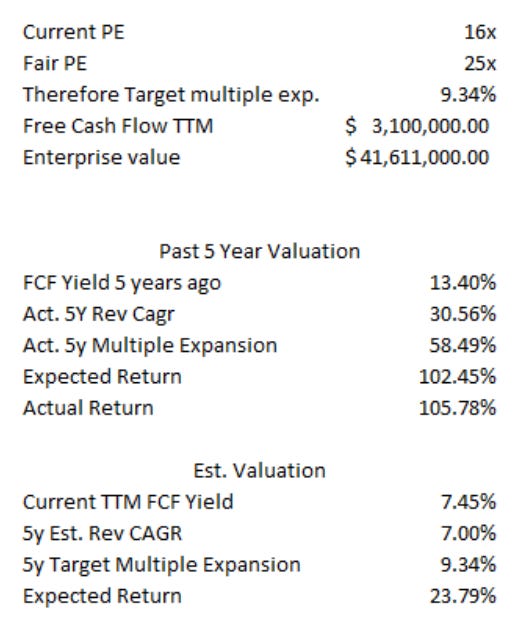

Valuation for me is FCF yield FCF/EV + FCF Growth + Multiple Expansion/contraction.

Given the prior 10y Revenue CAGR of 18%, I consider my valuation to be rather conservative. a 25x PE is also fairly conservative given the quality of the business model. The long term relationships and quality of clients probably gives it worthiness of a higher multiple, however to remain conservative I'll use what I have estimated.

As you can see there is still a huge expected return of 23.79%. The margin of safety and business quality provide enough conviction for me to make a position in my portfolio.