Hurdle Rate Unit Trust - Portfolio Update

Hurdle Rate Unit Trust - Portfolio Update

June 2023

Dear Unitholders,

Before we begin, I would like to advise you that there is no distribution coming in respect of FY23. No realised income has been received yet and we have only paid a minor expense of $220 for the BGL accounting software subscription to date which will be carried forward to offset future income. Besides this, I have covered all the initial setup costs of $1,460 out of pocket, which are not brought to account within the trust given they are not deductible since the trust is not a small business entity. The full history of performance data can be found on the full document.

I managed to allocate all the raised capital from the prior month, and we have closed the financial year with a full portfolio. We have new positions in Diverger (ASX:DVR), DSW Capital (LSE:DSW), Getbusy (LSE:GETB), Reckon (ASX:RKN) and AF Legal (ASX:AFL). All these businesses have been covered in detail on the Hurdle Rate Substack, which you should all have complimentary access to by now. If you do not, please contact me and I will sort it out for you. Investments have been made with an implicit “Hurdle Rate” in mind. This is a core tenet of the trust, and it effectively means to swing at only the best priced opportunities and nothing else. For me, it means I must realistically see a pathway to 25% returns annually (before the impact of performance fees).

We also received another vote of confidence with an additional $20,000 from a new unitholder. I would like to welcome you all again and thank you deeply for your commitment to the trust. This month the NAV of the Hurdle Rate Unit Trust increased in value by 3.61% to a unit price of $1.0207. Including performance fees, the increase during the month was 3.20%.

I would like to note that when applicable performance fees are levied by a transfer of units between the unitholder and myself, this is to ensure that each unitholder is treated fairly as a cash withdrawal would impact those unitholders which may have not seem the same performance (based on the timing of their purchase). For tax purposes, it will be treated as an adjustment to your cost base. I will be sending out updated unitholder statements whenever a transfer occurs.

During June there was some pressure on most of our Australian holdings to the notion of ‘tax loss selling’, where investors crystallise companies with a capital loss to offset against capital gains. Our international holdings were free from this tax loss effect with, however a decline in the conversion rate of the AUD/GBP have negatively impacted these in AUD terms. I stress that the variability in performance for our positions will be significant and is the price of admission. Performance ranged from +25% performance from the likes of DSW Capital and AF Legal to -8% performance from Sequoia Financial and Prime Financial, all of which announced nothing to the market. The primary benefit of this volatility is that it will create opportunities to add to and remove from our constituent positions over time. If a strict focus on fundamental value is maintained, I fully expect that the market will reward us over time for good valuation work.

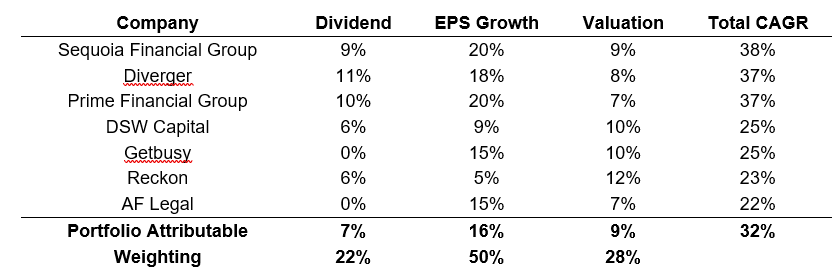

Now that we have a full portfolio, I can outline how I am viewing potential returns for our names based on their cost basis. These are merely estimations of their future trajectory, and the key is to maintain diligence on sourcing high potential opportunities for the trust, if we fall short on any of these we still end up with an excellent result. For further reference the 25% hurdle rate I would like to have >15% from Dividends and EPS Growth alone as valuation is a lot less predictable given the variability in investor sentiment as noted before.

Historically, through to the end of 2022 my own portfolio has returned a compounded +29% with a ~55% weighting to EPS Growth, ~10% to dividends and ~35% to market pricing net of currency movements. As you can see from the estimates for our current positions above, I am attributing future returns with a much larger skew to dividends, because the yield is much higher than the past investments I have made. As an individual with deeper expertise in these company industries than most, with what I believe to be a top 5% understanding of these businesses I expect my broad estimates to be much more accurate than the average market participant, and that is what gives me the confidence to estimate returns like this.

In the coming weeks going into July there’s a few things I’m looking forward to for the trust including Audited full year results for DSW Capital (LSE:DSW) on the 13th of July. August will also be an important month with our ASX companies reporting their full year results. Lastly, Getbusy (LSE:GETB) has announced it will release its half-year results on the 5th of September. Rest assured I will provide ample context to my expectations vs what we get in the coming months in these reports and on the Substack.

Yours sincerely,

Tristan Waine

Sole Director of the Trustee of the Hurdle Rate Unit Trust

Phone – +61 426 928 026

Email – Tristan.waine@outlook.com