Hurdle Rate Unit Trust - Portfolio Update

Hurdle Rate Unit Trust - Portfolio Update

August 2023

Dear Unitholders,

This month the NAV of the Hurdle Rate Unit Trust increased in value by 1.73% to a unit price of $1.0669. Including performance fees, the Net return during the month was an increase of 1.38%. The full history of performance data can be found on the full document, along with charts detailing the contribution from each of our investments. The below commentary will be long with 6 reports to discuss and the introduction of some new ideas.

This month marks the first month using the Investment thesis tracker. This section is to house a set of 1-page succinct investment theses and a summarised table at the top to indicate generally if it is on track with expectations. The financial targets are set at the start and fixed so as not to change part-way, unless the investment transforms in some drastic way, which will be detailed if, and when I believe that has occurred. The aim of all of this is to ensure that we hit our hold and total return targets, so of course I will be looking to report on this information as well.

For most of my investments, it is my intention to target a specific return on incremental capital and payout ratio combination that would allow for both a hold return (yield + growth) of >15% and total return (includes multiple expansion) of >25%. This is done so using a matrix with implied PE by ROIC and growth. Some investments are lacking in capital and/or profitability, for which I intend to track alternative measures such as non-dilutive ARR growth for Getbusy or a combination of margin expansion and flat working capital turns for AF Legal, at least until they can also be tracked using PE, ROIC and growth. Warren Buffett has highlighted the importance of incremental ROIC. In his annual letter to Berkshire Hathaway shareholders in 1992, he said,

"Leaving the question of price aside, the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return."

I look at what LTM earnings and the last reported equity and invested capital numbers are. What I am chiefly concerned with is earnings growth, and the amount of capital required to get the earnings growth. So, I am attributing an exit multiple that is implied by those 2 figures and a 25% hurdle rate, the lower the assumptions needed the better.

Take for example, our investment in Diverger was done so when LTM NPATA was just $3.8m, Equity is $37.8m and invested capital is $39.7m whereas the market cap and enterprise value were $30.1m and $32.1m respectively. Assuming a mid-point range of managements 40-60% payout ratio we get a dividend yield of 9%. To reach a 25% return we need growth of 6.5%, which is the other 50% of earnings retained at a ROIIC of 13%. So, from here you can refer to the matrix linked above and imply that a business generating 6.5% EPS growth at 13% ROIC is worth 14.3x earnings. With the multiple being 8.4x earnings, it’s about a 70% upside from the multiple, which over a 5-year holding period annualises at 11% p.a. The total return resulting is 9% dividend + 6.5% EPS growth + 11% multiple expansion or +26.5% p.a. Now I think a 13% ROIIC is more than achievable. This approach is merely embedding the minimum assumptions required to meet a 5-year 25% IRR.

Our investment in DSW Capital is an example of the requirement to generate a 15% return from earnings growth and dividends alone, with a dividend yield of 6%, and thus required EPS growth of 9%. Although with a payout ratio of 70%, this would imply ROIIC of 30%, which the matrix implies is worth a sky-high multiple of 70x earnings. With our entry multiple this implies potential multiple expansion of +840%, an annualised rate of 57% p.a. over a 5-year holding period. Obviously, this is such an outlier I just tend to think the multiple will take care of itself when we are only paying 7.4x ‘23 earnings for it, over a 5-year holding period we only need an exit PE of 12x.

With this tracker in place, I am happy that the core is being appropriately managed, however, I now shift my focus on to formalising the research process. Whilst I have put a lot of work into research with 130 posts now on my Substack written over the span of the past ~4 years, I would like to keep incremental research under wraps for the most part, with shared ideas only discussed in direct discussion with unitholders or specific investors. This is as to recognise the highly illiquid nature of these investments, and by taking ideas into the arena we potentially risk premature price discovery and/or a tainted perspective about an investment. By avoiding excessive social interaction before an investment is made and implementing financial targets (pre-mortem) as an investment is made, external influence is minimised. With this said, if you are a unitholder, I am open to sharing my active research pipeline.

Delving further, I have a watchlist of now 208 companies (including the 8 we own) that are all being actively monitored and progressively researched. Many of these have been the topics of the so-called “one page stock pitches” on the Substack, but most of them are completely unresearched. All of them, however, have announcements being emailed directly to my email address as they occur, allowing me to be pivot my research pipeline appropriately as companies develop in real time. In my view, it does not make much sense to spend a lot of time and effort researching a company at a point in time, only for that business to change (such as have its management change, a transformational asset acquired/divested or drastic capital allocation changes occur). It is best to keep your ear to the ground as good companies may become bad companies, and vice versa. What matters is how things change in the future, not how they have played out in the past. And I am always looking to expand this list further. So, if you know companies that may be of interest to me including not only professional and financial services businesses, but also businesses that service these as suppliers such as software, IT, recruitment, or training among others, please let me know.

Lastly, I have recorded a special podcast discussion with James Goodwin from Firm Returns where we spoke at length about Sequoia Financial Group (ASX:SEQ). You can listen to it and more in this playlist once it is released.

Furthermore, on the 16th of September at 7PM AEST I will be on a live discussion on X spaces joined by a few Asia-pacific heavy hitters including:

· Michael Fritzell from Asian Century Stocks,

· Jamie Halse, Fund manager for Platinum AM’s Japan Fund,

· Ben Tan, an individual investor from Singapore.

The discussion is co-hosted by 2 Austrian investors which you can find here and here. It will be an open discussion and opportunity to asking questions to all of us so I would be happy to see any of you listen in.

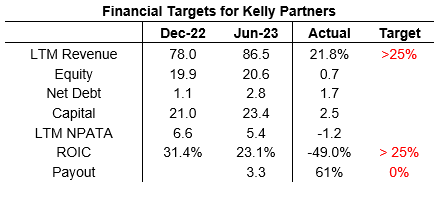

Kelly Partners (ASX:KPG)

Our newest position reported their FY23 annual results on the 11th of August which I found were broadly in line with what I had expected. Margins were slightly lower than anticipated yet lockup (Cash conversion) was slightly higher. Organic and acquired growth along with the net debt balance were within expectations. Perhaps one of the biggest disappointments was the amount they spent at the parent entity (11.9% of revenue) over and above the 9% services fee, albeit this was not entirely unexpected with the 1H parent spend being 12.3%. During my 1H results review I had said the following:

“It’s in my view that this (parent spend) could continue for a few years yet as they scale up overseas services teams which would have substantial cost relative to their actual services provided until they reach some reasonable level of scale. So that’s one thing that puts weight on those high value near term cash flows and is given the commentary in the earnings call, is likely to result in a cut dividend.”

By the way, I did mention the dividend cut here, but I really had no idea of their intentions with the strategic review just announced along with the full year results. I had seen Brett before making scattered comments about the potential for a US listing, but Brett had always denied criticism on the dividend policy up until now with the rationale that both internal and external partners deserve consistent cash flow. Also, the prospect of a privatisation came completely out of left field, and quite frankly would be very surprised to see them act on that in particular, and they received a very significant number of dishevelled questions on the privatisation in their earnings call.

Our tracking to the right includes the organic and acquired growth for the 2H in isolation where the business grew +0.8% organically and +10.1% via. M&A. Annualising of these numbers reveals growth lower than anticipated. Furthermore, the additional $2.5m in capital during the half came through with a $1.2m decline in NPATA, (primarily due to elevated corporate costs, increased interest rates and debt and a decline in both established and new firm margins) leading to a negative ROIIC. Dividends as discussed above are currently in consideration via. the strategic review, which I await keenly on news about with a preference for no-dividend compounding.

At the end of the month, I decided to trim KPG to a smaller size in favour of an alternative and opportunistic investment opportunity.

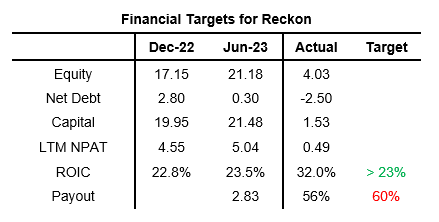

Reckon (ASX:RKN)

Reckon released its 1H 2023 results on the 15th of August which I found satisfactory. Continuing Revenue and EPS increased by 4% & 13% YoY respectively with the latter benefiting from a prior year R&D tax amendment. If it had not received that, NPAT would be down 2-3%, largely driven by increased amortisation due to capitalised R&D spend having grown faster than revenue in recent years. The balance sheet has further improved, with just $0.3m in net debt down from $2.8m in December, partly due to the group’s strong cash conversion with operating cash flow after adding back capitalised R&D, taxes, and interest at 107% of reported EBITDA.

The legal group grew its subscription revenue by +19%, but total legal revenue by +12% due to upfront and service revenue declining by 39%, but this is now just 7% of legal revenue, down by 14% last year. EBITDA was slightly in the positive but perhaps more importantly, NPBT improved by 14%, with strong operational gearing due to a near capacity cost base. All these figures can be reduced by 6% to reflect positive USD exchange rate movement. The business group fared less favourable, with it’s still excellent NPBT margin on an LTM basis (due to seasonality) declining from +30% in December in to +28% in June. However, this was partially offset by revenue growing 3% over the year. Pleasingly, they are making progress on swaying prospective clients into higher ARPU subscriptions with a big step in the cancellation of the free single touch payroll mobile app.

With the 1H result, based on modest growth in 2H revenues like the first, and seasonality typical of each division, I am expecting ~$5.2-5.8m in full year net profit after tax attributable to owners of the parent, with further optionality if they lodge an R&D claim for 2023 (Current half was an amendment of prior year). This could be upwards of $0.7m for a total of $5.9-6.5m. Given today’s market capitalisation of it would equate to an earnings multiple of ~10x. Without the legal group, Reckon, as a standalone business could trade at ~7x earnings. Lastly, the group indicated that it would move to an annual dividend payout and has declared a fully franked dividend of $0.025 per share, equating to a 4.8% and 6.9% net and gross yield respectively.

On the group’s 1H earnings call, Sam and Chris detailed their plans to transition the remaining Desktop subscription revenue to the cloud, which currently is a hybrid model where their ‘Reckon Accounts’ product is both offered to customers via. an executable desktop file along with the same thing, hosted in a Reckon server. This server (referred to as ‘hosted’) is a temporary step for clients to move into the cloud whilst they develop an accounts solution in the Reckon One infrastructure, as opposed to the Intuit Quickbooks infrastructure they own a license to as the old Quickbooks reseller here in Australia. It is conveyed that the existence of revenue on this infrastructure creates a barrier for potential takeover offers due to limited development potential under that infrastructure. This transition is expected to take <5 years, of which I suspect that the business group could well be ‘in-play’ for acquirers once transitioned.

Our financial targets are all tracking to plan, with what looks like impressive incremental NPAT margins and ROIIC, but it includes an R&D tax amendment from prior years of $0.7m. Without this, the NPAT would be down 4.6%, with incremental margins and ROIC of -17.9% and -13.7% respectively, largely due to a large increase in amortisation, however, as reported for all intents and purposes we have exceeded targets. Lastly, the dividend is an annual payment going forward, and Reckon is historically 1H weighted so will hit targets with a small amount of 2H NPAT.

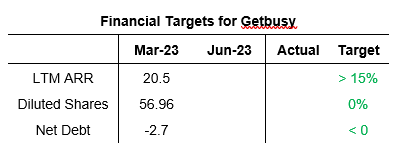

Getbusy (LSE:GETB)

Getbusy reports its half year results early next month, but just to establish financial targets, I am looking for recurring revenue growth more than our 15% hurdle rate using its own cash generation, free of debt or capital issuance.

DSW Capital (LSE:DSW)

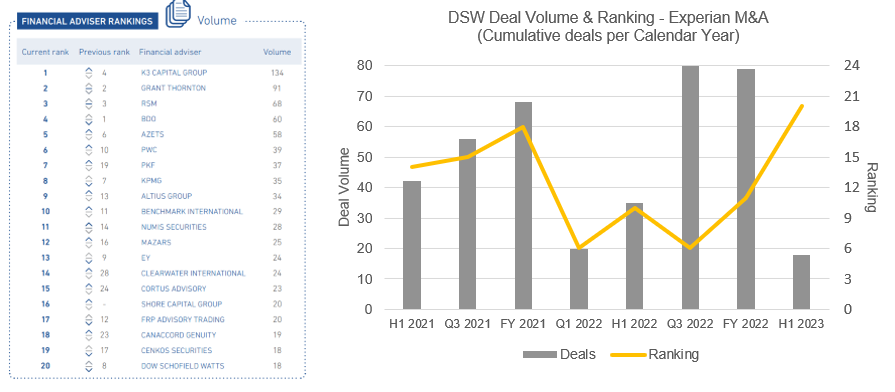

Whilst DSW Capital reported it’s result last month and there has been no subsequent announcements this month, I wanted to touch base on the Experian 1H23 M&A report which is highly important for the DSW business.

“The 2,863 transactions during the first six months of the year represented the lowest half-yearly total we’ve recorded during the last decade.”

~ Experian MarketIQ UK & Ireland M&A Review 1H 2023

As you can see below, DSW has fallen from the overall #8 ranking to the #20 ranking over the half year, with 18 deals advised on relative to 35 in the prior half comparable period. In terms of where those deals came from, 7 were from the Northwest (20 in H122), whereas it failed to rank in previous podium positions with <4 in Scotland (7 in H122) and <4 in Southwest (5 in H122). Overall, this is a decline of 48.6% in terms of deal volume, however, we are missing the value of these deals, so only get half the story. Despite a steady headcount in the M&A service lines, DSW has seen its ranking fall from a peak of 6 in the 1st and 3rd quarters of 2022 to 20 in the 1st half of 2023.

Whether this is a lasting trend or not, it’s hard to tell off the back of the financial results, but the 2H of FY2023 for DSW has been their worst in the past 3 years at the very least, and given their 2H revenue per fee earner as alluded to last month also being the worst in the past 10 years, it appears to me unlikely that things could get much worse for DSW than a 30% NPAT margin (~5-6% of network revenue). Given our purchase price of £8.4m enterprise value and a 2H network and parent revenue of £8.5m & £1.5m respectively, it would imply trough earnings of £1m, therefore we purchased at a high single digit PE multiple in what appears to be a clear cyclical low given industry deal volumes being their worst in 10 years and the addition of a drastic fall in 1H market share to a ranking they have not seen in years.

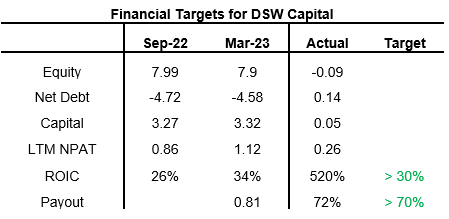

The other thing I wanted to touch on is in reference to the updated Investment thesis tracker. In the table I have stated financial objectives for DSW of >70% payout ratio and a ROIIC (Return on Incremental Invested Capital) of >30%. This is to approximate >6% dividend yield on our base earnings along with >9% EPS growth (30%*(1-70%)) and meet our hurdle rate of >15% return from EPS and dividends.

Notably, I have added back the SBP (Net of 19% tax rate) related to the Legacy/growth shares as they were pre-IPO and non-dilutive post listing. With this being the case, I reached a LTM NPAT of £1.12m & £0.86m for 2H23 & 1H23 respectively along with invested capital of £3.32 and £3.27. The business generated an additional £0.26m in NPAT with £0.05m in capital, a ROIIC of 520%.

Prime Financial Group (ASX:PFG)

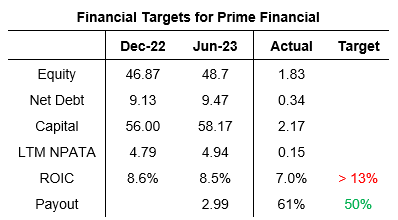

Prime reported results of +28% revenue (+19% Organic) & +15% EPS for FY2023. This is broken down in 1H & 2H growth rates in revenue of +31% (24% Organic) & +26% (15% Organic) along with EPS of +33% and +6% for each respective half year period. The drastic variance in 1H/2H EPS growth rates is due to the derecognition of an ROU asset relating to a Melbourne sublease. Underlying EBITDA growth of +11% for the full year with a decline in margins from 30% to 26%

Capital efficiency was particularly disappointing with cash conversion days further increasing from 60 in 2022 to 77 in 2023, which led to a subsequently poor ROIC relative to the growth in earnings with +7% ROIIC in LTM NPATA from 1H23 to 2H23. Luckily, this was accompanied by a top of the range dividend payout ratio, making things more stomach able. Debt is very slightly above target, but with slower dividend growth anticipated for FY2024, we should see the group pay this down to comfortably within target range in lieu of a new acquisition.

During the year Prime introduced 2 new service lines (both in the ABA & Capital division) in the form of Debt advisory and ESG consulting, with the debt advisory business being the result of the purchase of businesses assets including its business name and products. This purchase was for a total of $350k and generated $400k in revenue in the first 13 weeks alone. The acquisition and integration of Intello was also particularly successful, having contributed $500k in profit before tax in the first 9 months, implying full-year run-rate of $667k, inclusive of estimated purchase price amortisation of ~$360k, indicating that Intello would be generating EBITDA more than $1m, or $700k after tax. Considering the purchase was for a total of $4m, an earnings yield of ~17.5% for a negative working capital business is an excellent acquisition.

Interestingly, the group has introduced the intention to implement another 3–5-year plan of $100m of revenue by 2028-2030, 2 years prior to the current one being due. This points to significant confidence that they will achieve their current, which still requires 50% more revenue than they have now in the next 2-year period. The plan’s existence may well extend our potential holding period if the group remains of a reasonable valuation, but I would certainly like to see them achieve this growth at a higher ROIC than we have seen in our first half year period, that is, with stable cash conversion days. If we maintain the current ROIC we couldn’t reasonably expect any multiple expansion, whereas my target of 13% implied potential multiple expansion of up to 50% on our purchase multiple of ~10x earnings. In any case with a dividend yield of ~10% on our purchase price, even 7% ROIC still gets us to our 15% hold return (EPS Growth + Dividend Yield) hurdle.

Diverger (ASX:DVR)

Diverger reported Net Revenue +19% (9% organic) & underlying EBITA -2% (-11% organic). We refer to an underlying figure here as the bulk of the 21% decline in statutory profits relates to M&A accounting, which is non-cash in nature, shown on the right. Pleasingly, the group declared a 3.5c fully franked final dividend, bringing the full year dividend to 5.5c or 7.86c grossed up, which when compared to our cost basis of 80c, is just shy of a 10% dividend yield for on an LTM basis.

The company also took the liberty of highlighting the forward run-rate of acquired earnings, resulting in what they expect to be FY24 impacts of +15% Net Revenue (all acquired) and +19% (9% organic) underlying EBITA.

Cash conversion was highlighted by the company to be strong on a pre-tax basis, however, the group’s pre-paid it’s 2023 income tax opposed to a carry-forward balance in the prior year, resulting in an estimated cash conversion of 55% on a post-tax basis (FCF/NPATA).

On a more granular level, the group saw most of its organic growth come from the CARE managed portfolio’s business, with FUM up 21% YoY, with roughly 50/50 contributions from net inflows and market returns. This number being above the 13% revenue growth CARE has seen in FY23 gives good visibility for further strong growth in FY24 of at least 8% + any increase from further net inflows or market returns. In wealth, the number of full-ARs was also flat YoY, but a massive increase in the ASIC adviser levy cost (passed on to advisers) saw this disbursement drive net revenues substantially. Accounting saw mild volume growth of 2% YoY, but a margin decline saw accounting profits down 9%, due predominately to higher wages. There is upside potential of ~12% should accounting margins return to their historic 40%.

In terms of financial targets, I have set targets as discussed earlier in this letter with the assumption of a 50% payout ratio of NPATA (mid-point of managements stated range) and 13% ROIIC for 6.5% EPS growth. During the 2H the group reduced its debt more than it increased its equity, leading to a reduction in capital whereas 2H23 earnings were higher than 2H22, increasing LTM earnings. This negative return on capital, by default is exceeding our target ROIIC, as Warren Buffett has quoted “Growth is most positive when it takes no capital at all”. The dividend was slightly below expected but not an issue.

Overall, results were broadly in line with my expectations, but beyond our targeted returns with LTM NPATA growing 22.7% vs the 1H of 2023 with reduced invested capital, along with a declared dividend 3.6% of our cost base. With run-rate EPS of 13.2c Diverger trades at 6.5x our cost base.

AF Legal (ASX:AFL)

On the final day of the month, AF Legal reported their results for the full year, which given the change in management in the 1H, really was a tale of 2 halves. This is particularly noticeable when you look at the financial results. Revenue for the full year was $18.9m, with 53% coming in the 2nd half, whereas net profit before tax was $0.16m, with $0.62m in the 2nd half and ($0.46m) in the 1st half.

Regarding our financial targets, my thesis lies almost entirely on the group reaching what I believe to be feasible profit margins, without sacrificing revenue or working capital efficiency to do so. Growth is but a bonus to the thesis, and I was pleased to see 9.8% of growth on the year, most of which however is attributable to the 51% owned Darwin based Withnalls Lawyers, so it is dilutive to possible profit margins to shareholders. Withnalls also carries more WIP through the courts, and henceforth also is dilutive to working capital. Nevertheless, the growth in the period in my view is enough to offset the decline in lockup efficiency.

The management has also provided an outlook with a focus on continued organic growth, increasing profit margins and robust cash collection. All things which align with what I would like to see, so am a happy shareholder. Our target of a 15% margin is being rapidly approached, with the group collecting a 4.3% margin in Q3 FY23, stepping up to an 8.2% margin in Q4 FY23, of the back of unprofitable 1H figures. On a unit level, employees appear to be returning to historical levels of utilisation, with gross margins showing a noticeable reversal in the 2nd half as shown to the right. Historically the group has operated in the high 40s so it would be nice to see some stability and/or further improvement in employee utilisation.

Given our profits to date, it seems prudent to reiterate that I remain of the view that the AF Legal business is substantially undervalued, and that at a price of 20c, and enterprise value of 17.5c, simply annualising the Q4 profitability of the group would equate to an earnings yield of 9%, but I still see the prospect of near doubled profit margins in the short to medium term. I remain comfortable in our holding and seek no compulsion to replace it any time soon.

Sequioa Financial Group (ASX:SEQ)

Early in the month, given the weakness in the share price I chose to trim Prime slightly in favour for adding to Sequoia. This decision was done based on a perceived gap in potential IRR from each investment with Prime at ~10x PE and Sequoia at what I deemed to be ~4x PE (Both on an Enterprise Value basis) and weightings which I felt were too similar given this disparity in valuation.

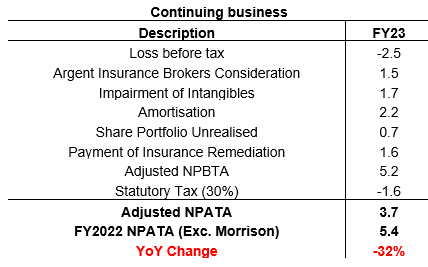

The group reported on the final day of the month, and to be frank the operating results were not good at all. However, they did receive the final tranche of the Morrison Securities divestment, closing that door at the very least. Now with $40m in cash on a $73m market cap, the market is valuing the continuing business at $33m. To approximate the economic earnings power of this business, we can do some adjustments to the financial results (shown to the right). Working back and ignoring certain management normalisations such as the decline in structured products, I approximate NPATA of $3.7m for the year, which would equate to 9x EV/NPATA.

Furthermore, during the year due to the decline in structured products revenue (which receives cash up front, and revenue is recognised over time), there was a significant working capital outflow. If the structured products revenue grows once more, there should be a rather substantial working capital inflow, so the cash flow statement looks atrocious this year, but it is largely due to that.

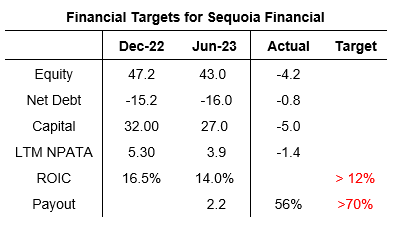

Regarding our financial targets, I have removed the insurance remediation from the above, but added back $1.3m for the Discontinued profit of Morrisons to reach full year NPATA of $3.9m. Due to the loss for the year, and the various non-cash effects, both the equity and the profitability are down, the net effect of which is dilutive to ROIC, leading to a miss of our target return. The group didn’t declare a final dividend, leaving the payout ratio less than we would of hoped as well. But given the intent of a special dividend that is 11% of our cost base later this year, and the board has reinforced FY24 budget NPATA of $7m and that the special dividend is consistent with an ordinary go forward dividend.

Of all reports this month, Sequoia would have to be the most frustrating given the home run that was the Morrison sale. Thankfully, the stock still looks cheap even on my adjusted and the companies’ budgeted earnings, I am hopeful of a rather strong recovery and good capital allocation in the year to come.

Finexia Financial Group (ASX:FNX)

Finexia is a new purchase this month, of which you can read a single page thesis of here. Assuming you’ve read that thesis I will spare you the details. Finexia reported this month with +35.4% revenue and -16.7% earnings per share, largely driven by a rights issue made during the year from which we have a part-year of income along with the favourable recognition of tax losses in the prior year which are now exhausted. On a profit before tax basis, the group grew +12.1% from the prior period. Interestingly, Finexia announced its inaugural dividend as $0.02 per share, 25% of the year’s net profit after tax, but 6.7% of our cost basis and 8.9% including franking credits. Perhaps even more interesting is that the group generated $0.08 in EPS for the year, whereas the valuation we purchased the business on was a market price of $0.30 and enterprise value per share of $0.16, or about 4x and 2x EPS respectively. With a valuation like this you’d expect the business to be a chronic value destroyer, but in recent years the group has generated returns on its equity of 25%, 47% and 29% in each of the last 3 years. The dividend policy for me was the tipping point.

In saying that, in line with our trust requirements of >15% hold return (EPS Growth + dividend yield), we are demanding 5% EPS growth from a 2/3 retention rate, or a ROIIC of >7% p.a. This appears to be more than achievable given returns in recent years and the prospect for further increased dividends due to majority of the AUM growth in the FY23 year occurring in the final months of the period (as shown to the right), embedding a lot of implied net interest margin into the FY24 year, which in simple terms should lead to a very strong FY24 growth rate as well. With these targets in place, and its miniscule valuation multiple, I view the hurdle rate is easily achievable should the business maintain its current performance and growth trajectory.

Special Situations

During the month I participated in 2 unique investment opportunities outside of the trust. Whilst 100% of my investable equity is inside the trust, I retain empty brokerage accounts outside of the trust. With emergency savings and an interest free credit card facility, I funded both a tender offer from Trinet (NYSE:TNET) and split-off between Johnson & Johnson (NYSE:JNJ) and Kenvue (NYSE:KVUE) of which I bought an odd-lot sized position in both. These generated returns of +3.7% (+78% IRR) and +9.7% (+1,588% IRR) respectively. I have put single page theses for both in the thesis section of the document.

These are appealing as they provide a unique opportunity for smaller investors due to the preferential treatment of odd-lot holdings and provide a known timeframe, making them particularly appealing to conduct with credit cards, as I have a 55-day interest free period, leading to the retention of both interest-bearing assets and exploit of non-interest-bearing liabilities, an ideal way to juice household income in my view. The reason I’m mentioning this is not to boast, but to talk about the prospect of incorporating this into the trust, without having to sell our core holdings. The idea came across from this Substack post where the author mentions:

“While this idea won't make anyone wealthy, we appreciate these opportunities as a chance for EPC to offset some or all of our clients' management fees and trading costs, depending on the account size.”

I really liked this perspective, as a way of offsetting the trust’s minimal operating costs and part of the performance fees it may be worthwhile investigating forms of low/no-cost finance in order to generate consistent cash flows from special situations in addition to those generated by our core holdings, ideally with the grand goal of offsetting part if not all of our fees (an odd-lot in both of these opportunities alone would of contributed +1.03% to our opening NAV for the month), although that would be more difficult as we scaled in size, requiring not only increased financing facility, but also additional accounts to purchase multiple odd-lot sized positions for example.

To enable consistent flow of ideas in this area, I have purchased an annual subscription in Special Situation Investments (SSI) (0.05% of NAV), a website dedicated to sharing special situation ideas. The cost has been paid by me and will be reimbursed with part of next month’s cash dividends. Rest assured I am fully expecting this investment to pay itself off multiple times over, and I will be loaning my own money into the trust to do so for the time being (until we find the trust’s own finance). We are looking for consistently low risk ideas so it is unlikely that I would take speculative options, but every and all odd-lot tender offer or split-off ideas are fair game, and any particularly appealing liquidations, merger arbitrage or option strategies. Basically, anything that a) has a defined time span and b) is low risk, utilising derivatives wherever it makes sense to do so.

Opportunistic Tail

The idea of incorporating a tail end weighting of the trust has also been floating around in my mind, whereby I maintain a core of 6-8 positions at ~80% of the trust and a longer tail end of up to 10 ideas accounting for the final ~20% of the trust. Such things that would suit this are multi-month special situations that could not be financed as discussed above or unique ideas in my circle of competence which may not carry the conviction of a core position and could eventually be elevated to the core.

Furthermore, by having additional positions, it would allow us to access more leverage on Interactive brokers if we would want to use it for special situations. If I was to implement this, I would do so via. allocating incremental cash dividends and inflows rather than crystallising our investments to avoid unnecessary CGT.

Along these lines, after listening to the X spaces with successful micro-cap investor Paul Andreola this month I am thinking much more about the prospect of incremental ‘discovery’ in my portfolio and would like to plant some seeds on the earlier spectrum of discovery (Shown to the right) that have some early but fundamental strength in their business.

The largest returns are available at the pre-discovery and catalyst stage of the process. Given its sky-high multiple I have decided to trim Kelly Partners down to a smaller sized position (~5%) in favour of much cheaper undiscovered businesses. I still maintain a strong belief in its future success, but I believe that I captured the best possible returns in my 2019-2022 holding period where it was executing not only fundamentally but saw itself go from pre-discovery to institutional shareholding in its largest shareholder.

Yours sincerely,

Tristan Waine

Sole Director of the Trustee of the Hurdle Rate Unit Trust

Phone – +61 426 928 026

Email – Tristan.waine@outlook.com