Infomedia (ASX:IFM) - One Page Stock Pitch

Infomedia (ASX:IFM) - One Page Stock Pitch

Auto Parts/Service SaaS software

Today’s subject is Infomedia (ASX:IFM), a SaaS platform for aftermarket auto parts sales. Their primary product is essentially aftermarket auto parts quoting software , but have since started providing integrated data analytics as well.

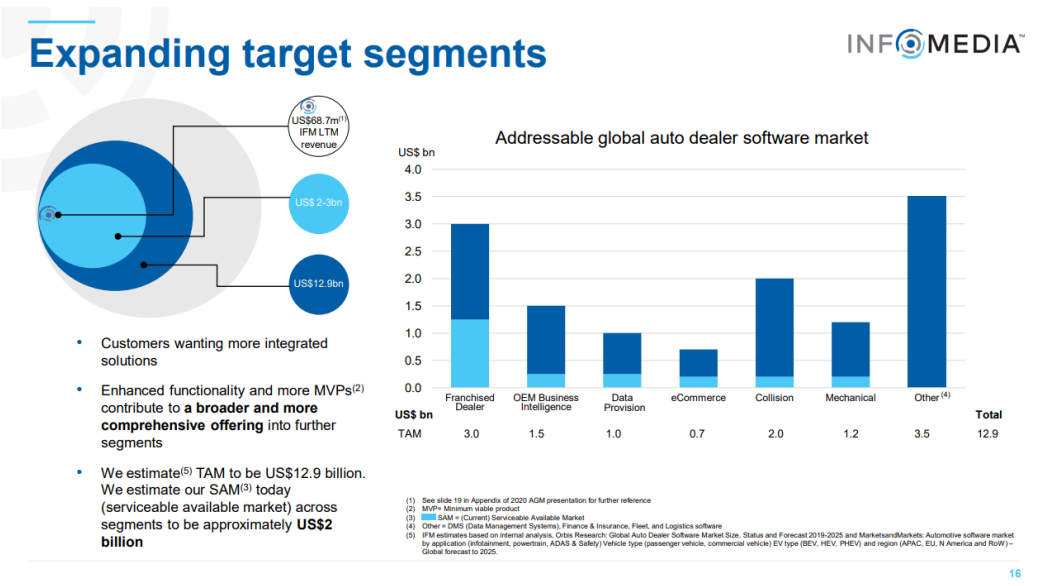

This has resulted in an expansion in their target segments, where they estimate US$2b to be directly serviceable for them.

What initially interested me was a nice stable high ROE and reasonable growth in revenue and earnings over time. No secret sauce here, anyone could have seen this and been equally interested.

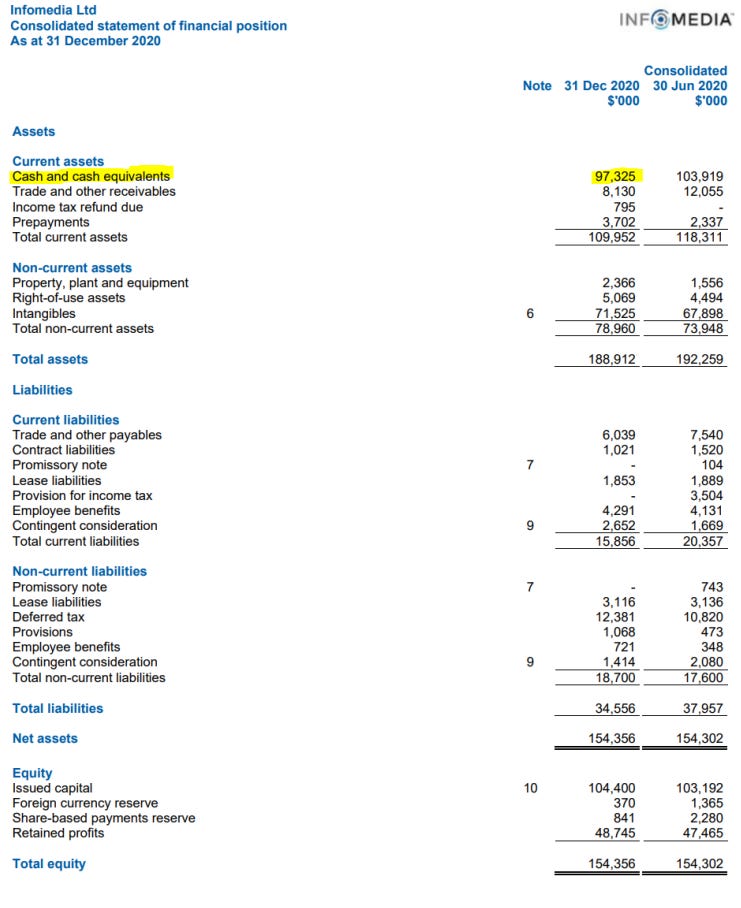

But the most important thing here is that IFM has cash unused with intent to reinvest. Even if you assumed ~15x PE for this cash, it would still be ~7m of additional NPAT in earnings power, which puts us at ~26m of NPAT on a $550m market cap (21x PE)

Recently they purchased US based Automotive Ecommerce platform Simplepart for US$24.5m upfront, has US$10m of revenue and is growing ~13% p.a. Assuming similar margins and payout to IFM this would suggest ~5% FCF Yield + 13% growth = ~18% ROIIC

Taking this into account, 2H FCF and the unutilised cash, It would be reasonable to assume >24m FCF for FY22 and $50m in cash (97+ ~10m est fcf - ~33m upfront simplepart - ~25m contingent consideration), putting us at closer to ~$28m in FCF in earnings power (19x PE)

If you take their margins that they currently have of 20%, this implies revenue of $140m, meaning that they need an additional $60m of cash to get to their aspirational target of $200m by 2025, a CAGR of ~15% from 2020 Revenues, which will likely come from some dilution as well.

Dividends are a very high % of the earnings at typically 60-80% of the earnings of the business, meaning that the current yield is 3-4% on a run rate basis and ~2.5-3% currently. So what we really need here is some source of organic growth, and for the past decade or so, it has grown at ~7-8% p.a.

Coupling this with low insider ownership and no real re-rate potential, it was at this stage that I decided not to pursue this as an investment opportunity as a business that would return high single-low double digit growth with the yield is only half of my hurdle.