Investment Strategy in Writing

Investment Strategy in Writing

Trust Structure Proposed Investment Strategy

Investment Philosophy

Picking the investments that are going to maximise your chances of achieving your investment goals is the key for success. For this reason I have chosen a strategy that has a focus on risk rather than merely return. This strategy is commonly referred to as ‘Value Investing’.

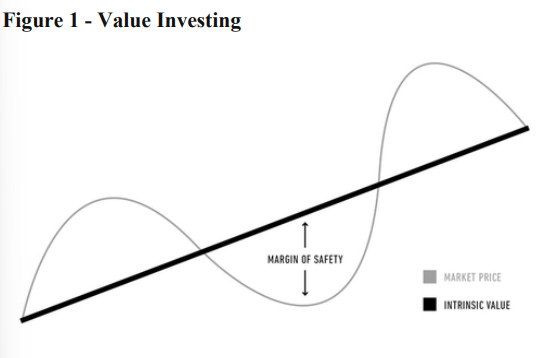

The basic concept behind every-day value investing is straightforward: If you know the true value of something, you can save a lot of money when you buy it on sale. The true value of an investment is called its ‘Intrinsic Value’ which differs from the market quoted price. Stocks, like many other products, go through periods of higher and lower demand leading to price fluctuations—but that doesn't change what you’re getting for your money.

Lastly, but most importantly is the concept of a ‘Margin of Safety’. Margin of safety is a principle of investing in which an investor only purchases securities when their market price is significantly below their intrinsic value. In other words, when the market price of a security is significantly below your estimation of its intrinsic value, the difference is the margin of safety. Because investors may set a margin of safety in accordance with their own risk preferences, buying securities when this difference is present allows an investment to be made with minimal downside risk.

I believe that following this strategy over time offers an attractive premium to the average stock market over time if done correctly, inspired by the Value Investing Gurus of old:

Portfolio Allocation

The popular saying goes “Don’t put all your eggs in one basket”. This is true of investments as is true of everything else in life. In investing this is referring to ‘Diversification’. The rationale behind this technique contends that a portfolio constructed of different kinds of investments will, on average, yield higher returns and pose a lower risk than any individual investment found within the portfolio.

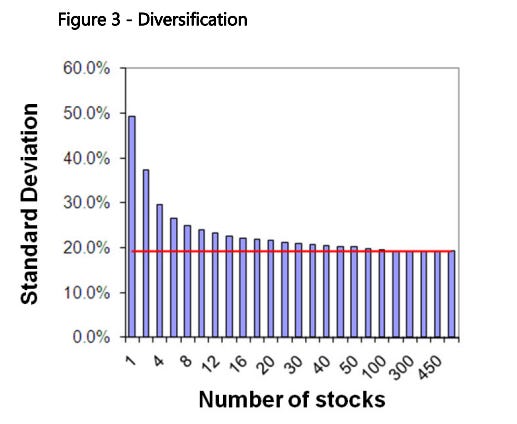

As you can see above, there is a diminishing value of adding each additional stock into a portfolio. With the vast majority of risk being eliminated by just 20 stocks. For this reason I find it unnecessary to add more than this into a portfolio. Of note is that the number of holdings is not the only diversifiable risk. You can also benefit from diversifying between industries, countries and asset classes, which I also intend to do.

However, the one caveat of excessive diversification is that the more you do, the more likely you are to match the market returns over time. Diversifying an investment portfolio tends to limit potential gains and produce average results. An investment portfolio of five carefully chosen stocks can substantially outperform the market. Watering it down with dozens of other stocks leads to mediocre performance.

For this reason there is a delicate balancing act at play here. The number of stocks you add to your portfolio should be commensurate with the level of confidence you have that a particular stock will work in your favour. This demands a thorough understanding of the business so that you can benefit from High-Quality companies and focus your time on them accordingly.

I have not completely decided on a specific number of stocks to hold in my portfolio, however I have a specific range of between 8-12 would be a sensible number of stocks to hold, which would eliminate more than 80% of the diversifiable risk.

Stock Selection

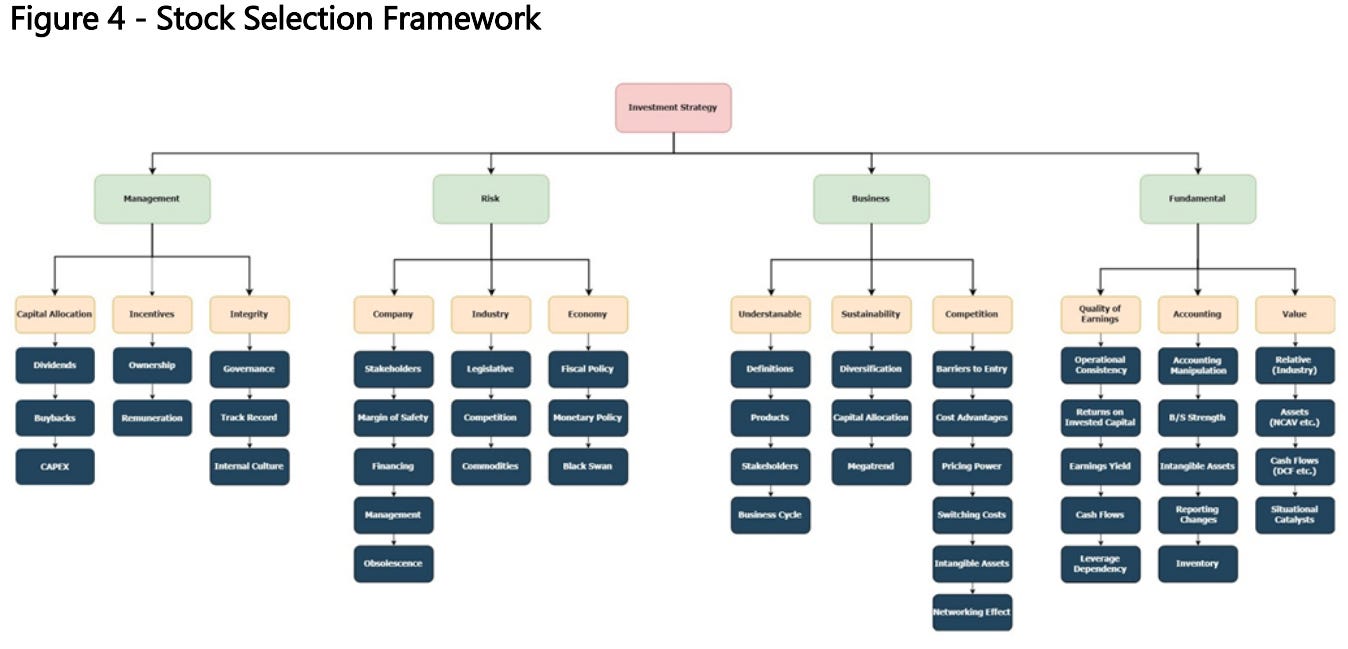

Over time i’ve tested various methods of stock selection, however it’s key to have a flexible yet comprehensive framework in which you approach security selection. For me, I use the above chart as a reference point. This reminds me of things that I may otherwise forget to cover when dedicating to due diligence, which is just another way to minimise the risk of me being wrong in my analysis.

There have been several examples of scenarios that I personally have invested in and lost money which I could have prevented if I had covered all bases. Below are some examples:

Ambertech Ltd (ASX:AMO)

This business is an Australian audio visual distributor trading at well below the liquid assets on the balance sheet at the time I invested into the stock. However, where I made the mistake was not being aware of an impending reporting change in ‘AASB16 - Leases’. This reporting change requires companies to disclose the outstanding liability of any contracted premises leases on their balance sheet. This extra liability caused the margin of safety to close rapidly on simply just reporting, foiling my thesis for holding the stock.

Collection House (ASX:CLH)

This particular security i did cover all the bases using the above framework. However, even though I had identified a red flag in executive management, I chose to invest anyway. Several weeks later the CEO abruptly left the company. Since I had a comprehensive viewpoint on the business, I could swiftly act and chose to sell my shares. Since then the business has suffered in not only share price decline, but also remains in a suspension halt at the time of writing this.

I hope this outlines the importance in the breadth of analysis required when conducting due diligence on an investment. If you fail to do so you run yourself the risk of being wrong.

Step 1 - Is this in my ‘Circle of Competence’?

The start of any analysis is reading a business description and being able to determine whether this is something you would be a good fit for your portfolio or not. The key to this is being painfully aware of your own ‘Circle of competence’.

“What an investor needs is the ability to correctly evaluate selected businesses. Note that word “selected”: You don’t have to be an expert on every company, or even many. You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

~ Warren Buffet - 1996 Shareholder Letter

I’m no geologist, so it makes no sense for me to invest heavily into mineral companies. Similarly, I'm not a doctor so why speculate on the outcome of a new patent? These comments make sense and will ultimately serve you specifically to protect your hard earned capital and maximise your odds of success.

In saying that, defining boundaries once and forgetting about what you don’t know is also harmful to you as an investor. Lifelong learning is key throughout all facets of life, investing included. Expanding your circle of competence over time is a necessary activity and will open up more opportunities to you.

Step 2 - Making a snap judgement

Now most people may not align themselves with ‘judging a book by it’s cover’, however to avoid wasting my time, I totally do this. Why? Because the sheer amount of companies that are out there are too much to analyse individually one at a time. It would take countless lifetimes to gain a thorough knowledge of each business in the global stock markets. For this reason I prefer to make ‘Snap Judgements’ on companies before diving into the specifics of the business.

For this step, i like to use ‘QuickFS’ or ‘Morningstar’ to briefly screen the 10 year historical financial results of each potential opportunity. What i look for specifically includes but isn’t limited to:

Consistent revenue growth.

Large profit margins that are either growing or consistent.

Cash conversion (Free cash flow/net income)

Large and consistent ROE, ROIC, ROA.

Liquid balance sheet (Low debt, high cash, low fixed assets).

Capital Allocation (Dividends, Buybacks, Debt repayment, Capex)

Valuation Ratios (PE, PB, PS, EV/EBITDA etc.)

Whilst these traits are the hallmark for what i consider to be a high quality investment, there are exceptions to the rule that can be treated case by case. An example would be a particularly valuable asset or contract that the market is mispricing.

Besides these quantitative factors i also look for a range of qualitative factors which can be found within minutes including:

Management ownership interest

Management remuneration

Substantial shareholders

Seek/Glassdoor reviews

Competitors

Catalysts

This is enough information to form a preliminary appraisal of the business. If this value offers a large margin of safety, if it then passes the filter and is worthy of a deeper look. This appraisal is usually done depending on the scenario. Some methods i use are below (Explained Later):

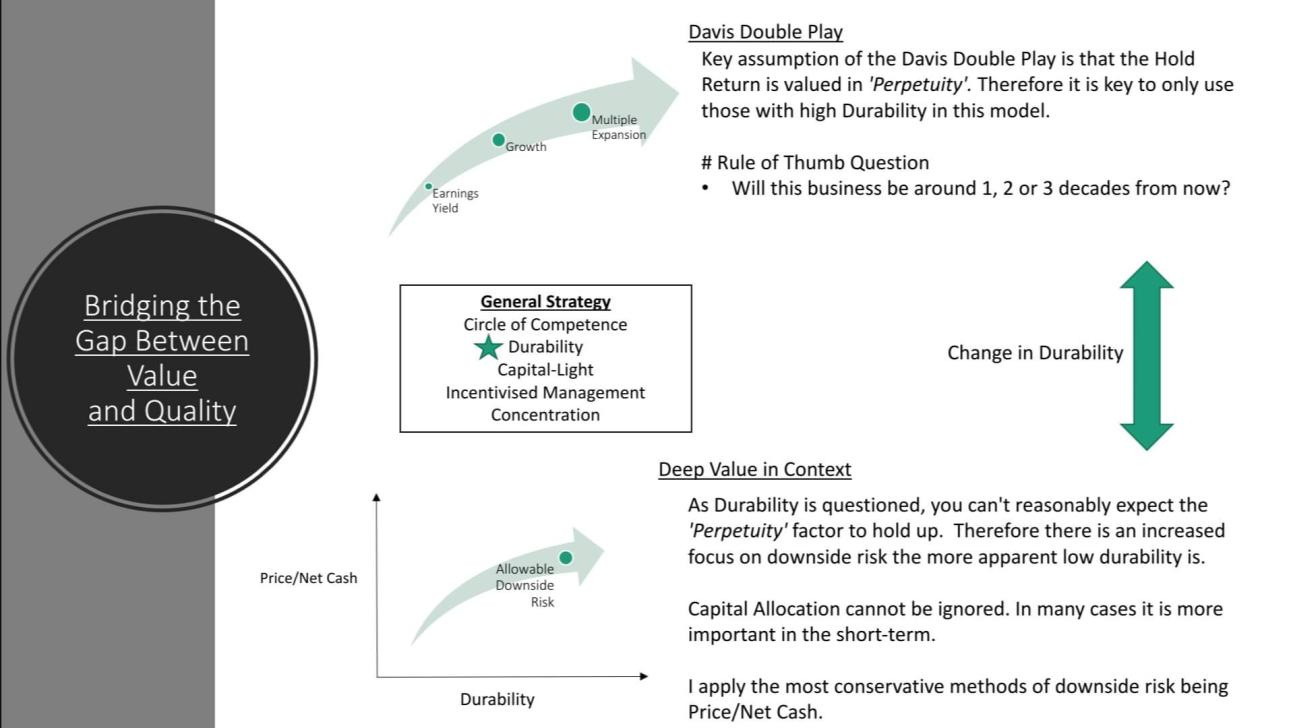

Davis Double Play (Durable Businesses)

Payback Period (Undervalued Businesses)

Liquidation Value (Deep Value)

Step 3 - Understanding the business model

Learn about how the business works. What are their products? How do they make revenue? Who are their customers? Who are their suppliers? Evaluating this is key to making an informed investment decision and determining the durability of the business model.

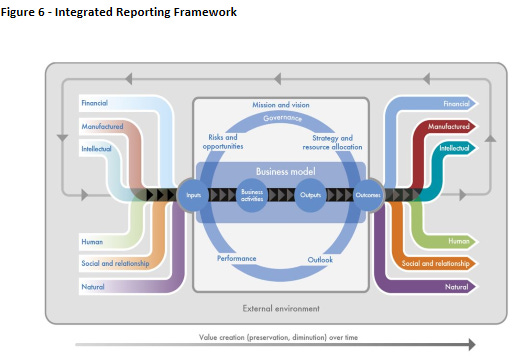

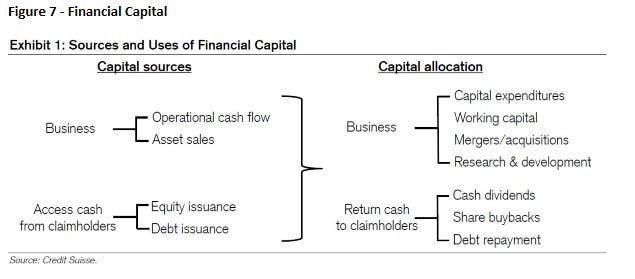

To assist in this process, i find the ‘Capitals Model’ in the integrated reporting framework to be especially useful in determining how an organisation creates value for its stakeholders. All organizations increase, decrease or transform capitals through activities. Together they represent stores of value that are the basis of an organization’s value creation, as illustrated in the below diagram.

The six capitals can be summarised as:

Financial Capital - Source of Funds

Manufactured Capital - Physical objects for goods/services

Intellectual Capital - Intangibles that provide competitive advantage

Human Capital - Capacity to innovate + Skills & Experience

Social & Relationship - Relationships for collective well-being

Natural Capital - Natural Input to goods/services

So this step involves identifying what the capital inputs are and how the business uses them to create value. The best businesses increase as many capitals simultaneously as possible, trade-offs must be made of course, however if a business neglects any one specific capital it may be creating value unsustainably. Sustainable value creation is the key to a successful business model.

Step 4 - Evaluating Management

So once i’ve identified HOW an organisation can create a sustainable source of value, the question is now IF they can create value. The key to this step is identifying management incentive to operate sustainably whilst also identifying how the capital outputs are being addressed.

For example, the easiest capital to follow is the financial capital. The organisation creates profit which is an output of financial capital. Once the output occurs, there is a capital allocation decision that management can make. This is just one of the areas in which you as an investor have to evaluate.

Firstly, i like to identify how much ‘skin in the game’ management has, which primarily relates to their interest in a company’s shareholdings. Owners’ are generally favourable in this regard. This is because if they perform well, the share price eventually moves in their favour making their holdings more valuable.

Of course, this is not without its faults. A primarily financial interest opens up a sole focus on the ‘Financial Capital’, which may cause them to neglect other sources of value for an organisation. In short, sustainability may be absent. For this reason I like to see a long tenure or even a founder on the executive team.

Remuneration can be used as a flexible tool to incentivise the executive team to act in specific areas for a bonus. Alignment with a long-term interest here is also preferable. KPIs from each source of capital, weighted accordingly to where it is lacking, is key in realigning shareholder value creation over the long term.

Lastly, as alluded to earlier is how the outputs of capital are used to ‘reinvest’ for the sustainable value creation over time. Examples include new hires (Human Capital), Capex (Manufactured capital), Acquisitions (Intellectual Capital), Distributions (Financial Capital) among many. The key is assessing the usage of the outputs and how it will affect the flow of value creation over time.

Being shareholders it makes sense to emphasise the importance of Capital allocation in a financial sense, since this directly impacts the results of our investment. Assuming that management maintains a sustainable creation of value, Financial Capital works specifically as below:

Step 5 - Determine the risks

Of course it’s not worth investing without a focus on the risk in tandem with the reward. Just like incorporating a margin of safety to maximise the chances of being correct, being aware of the risks that can close that margin of safety is key to getting to a predictable outcome.

Commonly, in a company's Prospectus, Annual Report or other filings they will have a ‘Key risks’ section in which they outline their own perspective on the risks that the company will face, this is always worth reading.

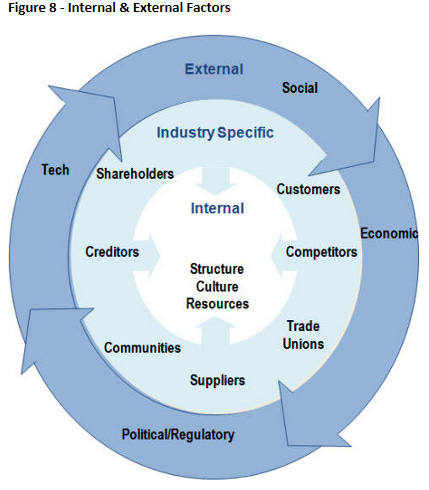

I like to break these risks up into external and internal risks. Internal risks are company specific such as employees, management, financing etc. whereas the external risks relate to stakeholders such competitors or regulators.

Being aware of the severity and likelihood of these specific risks is essential in making an informed decision. It will also help you determine how much of a margin of safety you should demand when conducting an appraisal of the company.

Step 6 - Valuation

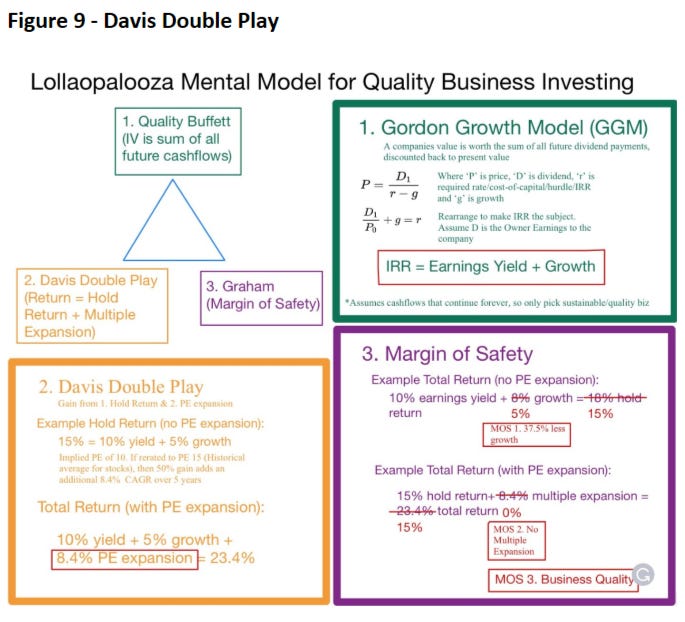

Davis Double Play

This is the primary method I intend to use for valuing highly predictable businesses. The rationale behind it is that the current earnings will remain growing into perpetuity and that you also assume an exit multiple at a specified time period from today.

For example i will demonstrate this on the current price for Hitech Group Ltd (ASX:HIT). This business is currently trading at an EV/FCF of 9x. This means that the cash earnings yield of the business is ~11%. A conservative growth figure I would estimate as 10%. A fair multiple i simply use 2x growth so 20x PE, i’ll also use a 10y time frame for the business to reach that multiple which would require an extra 6% PE expansion CAGR. With these inputs i can estimate the IRR:

IRR = 11% (Earnings Yield) + 10% (Growth) + 6% (PE Expansion) = 27% CAGR

This method is an easily repeatable method however to use it with reliability requires a particularly durable earnings profile which you should have determined in the previous 5 steps.

Given my goal of ongoing 10% investment returns I like to look for IRR’s which yield over double to give myself a wide margin of safety.

Payback Period

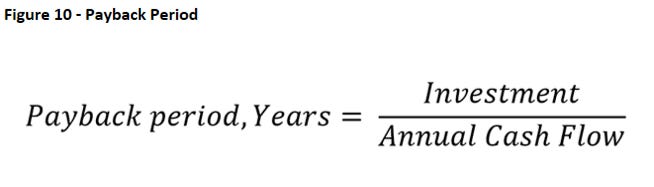

The payback period refers to the amount of time it takes to recover the cost of an investment. Simply put, the payback period is the length of time an investment reaches a break even point. The desirability of an investment is directly related to its payback period. Shorter paybacks mean more attractive investments.

As this method doesn’t take into account the time value of money, I only use it for short term payback periods to minimise the effect of the absence of discount rates. Furthermore it ignores anything that happens after the period.

The Formula for payback period is very simple:

Where:

Investment = Market Cap

Annual Cash Flow = Free Cash Flow

Whilst this formula doesn’t factor in growth, it’s easy enough to intuitively assume that the payback period will be slightly shorter.

"It is better to be approximately right than precisely wrong."

~ Warren Buffet

For example, Plus500 currently has an Enterprise Value of around $600m. The 2019 FCF was ~$140m. Without growth assumptions the payback period would be 600/140 = 4.3 years. So I can simply assume that adding growth will shorten this time period, I don’t really care by how much because it’s already cheap without the growth assumptions, it’s just sweetening the deal.

Similar to the IRR hurdle of 20% i look for stocks that will pay back within 4-5 years rather than the implied 7 years for 10%.

Liquidation Value

These are the classic value investor stocks that were popularised by Benjamin Graham in his book “The Intelligent Investor” referred to as ‘Net-Nets’. Essentially a net net stock is a low Price to Book stock but where the “B” in the P/B ratio has been stripped of all long-term assets. I like to go one step further and strip all the assets except for the most liquid (i.e. Cash and Cash equivalents) as i believe this yields the largest margin of safety.

For this reason, I don’t expect to see many of these at all, but when I do I can be assured that it’s the most conservative way of using a conservative strategy.

Calculating this is simple enough:

Net Cash = Cash & Cash Equivalents - Total Liabilities

Net Net = Net Cash > Market Cap

While this might look valuable, it is not enough to simply find a stock that is trading net of cash on the balance sheet. It could be trading at this for good reason, such as off-balance sheet liabilities or a dramatically negative cash burn. These will quickly close the gap, so it’s preferable to only be interested in Net cash stocks that are accurate and not burning cash, possibly even remaining profitable.

Besides accounting it’s important to be skeptical of countries not reporting under IFRS or those with questionable governance practices. Insider selling or those in particularly unpredictable industries such as biotech or mining are difficult to get conviction in as well.

Catalysts are key in realising the value of the discount on offer, this might include buying back shares, improving operations, takeover bids or simply returning cash directly to shareholders.

The most important thing I have to keep in mind is that the vast majority of stocks at a net cash price can be assumed to be a terrible business. From there you have to convince yourself that it’s worthy of your capital.

Liquidation type valuation is the most difficult to define in terms of forward returns, but generally i like to see a tangible discount to net cash. Say <70% of net cash.

Trading

Position Sizing

This section relates closely to the portfolio allocation mentioned earlier. But differs in that it relates to the management of positions in the portfolio.

Being value investors it might seem rational to overweight the best ideas, which I can align myself with strongly when there are heavily stacked odds of working out.

“Heads I win, Tails I don’t lose Much”

~ Mohnish Pabrai

In general I believe it’s best to ascribe an equal weighting to your positions. This keeps the emotion out of it and most importantly, over time your best ideas should become a larger portion of your portfolio without direct intervention.

Selling Stocks

We’ve spoken about how to buy but not how to sell. The way i look at this is dead simple, it’s merely when either the stock is heavily overvalued relative to my expected returns or more likely, when an attractive alternative would result in it being worthwhile to switch from one to the other. Note that tax consequences are rarely a reason to or not to sell, only really in the case where you are close to receiving the CGT discount would you defer the sale of a capital gain. Basically where it’s obvious to do so you can factor in tax.

Financial Products

This I won’t go into detail but it’s always important to consider the various ways you can take advantage of an investment opportunity. The common stock is not the only option you have as an investor. Some other examples to be aware of include preferred shares, bonds, margin or various option strategies. These are things I'm looking at exploring over time and will consider their value on each decision I make.