Kelly Partners Group Holdings (ASX:KPG)

Kelly Partners Group Holdings (ASX:KPG)

July 2023

Kelly Partners Group Holdings is a listed parent company which owns a majority stake (Typically 51%) in many accounting firms across the east coast of Australia. These accounting firms predominately engage their small and medium business clients with accounting services on an ongoing basis. This includes compliance with both federal and state tax obligations along with managing permanent documentation as corporate messenger. In addition to this core function, complimentary service lines are offered to clientele such as wholesale wealth services, insurance/mortgage broking and even wholesale investment.

This operation was founded in 2006 by none other than current CEO and significant shareholder Brett Kelly. Brett was born in Sydney in 1974, who after high school went on to complete a bachelor in business and masters in tax, as well as being admitted as a CA. His employment commenced at PWC for 5 years before a brief role in corporate finance at Schroders before starting Kelly Partners in 2006 with 2 other partners. From here the business has grown its top line from $1.2m in the first year to what it is today. As of 30 June 2023, the group generated $86.5m in LTM revenue and has 32 offices with 78 Equity partners (Those with a minority stake in the underlying partnerships) servicing c.19,000 client groups.

For added complexity, the group engages in frequent acquisitions to grow with a stellar track record in making them work, uncharacteristic of the many companies that have attempted similar consolidation with no success. What makes Kelly Partners different is a focused approach, exercising caution on people, structure, and price. Deals are structured utilising a partnership agreement, isolating risk to the parent by using a wholly owned special purpose vehicle to hold the equity interest in that partnership (otherwise called ‘ring-fencing’). From here, the partnership takes on any necessary debt and loans it to the equity partners for them to repay, keeping default risk isolated to that partnership. If you read that carefully, I am implying that the listed parent entity utilises no equity to enact any acquisitions, instead paying off its share of the partnership debt using incremental partnership distributions from the newly created partnership. Another benefit of using a partnership structure is that it is not a separate legal entity that benefits from the so-called veil of incorporation. Therefore, partners have unlimited liability and are all liable for each other’s share of the debt that is within the partnership, this has the benefit of partners that take on an equity loan working extremely hard to at least pay off the loan, which benefits the parent entity significantly. Before we can discuss M&A metrics, we need to understand firm unit economics and capital intensity.

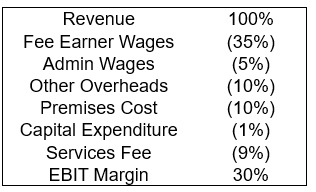

Above is my estimate of a firm’s margin profile. Underlying Firm margins typically adhere to the mantra of 1/3 direct costs, 1/3 overheads and 1/3 profit with EBIT margins of ~30% in any given year. Firms tend to run on a time-sheet billing model where hours are accrued in a practice management system when working on a client job, admin related tasks are not billed. Whilst we have assumed admin is 1/8 of total wages, admin staff are paid less and there is likely to be 1 admin head per 5 fee earners. Overhead expenses are any non-parent covered costs (relating to IT, HR, marketing, finance), stationary costs, software subscriptions, and travel in addition to the minimal capital expenditure required by a firm. The services fee is in return for the HR, marketing, finance, IT, and strategic functions performed by the parent entity.

From here any subsidiary level interest is paid before partnership distributions are made. In the event of a firm having paid off its partner loans, the parent entity would take pre-tax profits of ~15%. In an ordinary year this is unencumbered barring statutory tax, but often the parent entity expenses are slightly more than the 9% services fee, causing the parent to dip into partnership profits, In the consolidated financial statements this often confuses investors. Assuming this does not happen, the group pays 30% statutory tax and ends up with a net profit after tax margin of ~10%.

Regarding capital intensity, professional services firms carry just accounts receivable and employee creditors only. Given my prior comment on timesheets, typically unbilled timesheets are carried on the balance sheet as so called “Work-in-Progress” and billed timesheets are accounts receivable as normal. You must be careful with Work-in-Progress as it is possible that large portions of it can expire worthless as a disingenuous recording of time, resulting in a bad debts expense, this is much the same as a retailer having to write down the value of its inventory for various reasons. The sum-total of accounts receivable and work-in-progress is referred to as “Lockup”, and often capital intensity of a firm is solely reflected by the number of days it takes lockup to turn, calculated as fee income divided by the average balance of lockup through the period. In this sense, Kelly Partners has excellent focus on minimising lockup, with an internal target of <55 days, relative to peers often carrying closer to 100 days or more.

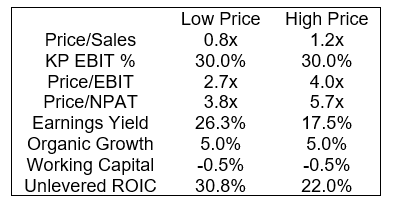

With unit economics established we can engineer M&A metrics (Shown above). To set the stage, Kelly Partners conducts several inorganic growth strategies including greenfield (new office, existing partner), tuck-ins (new partner, existing office) and marquee acquisitions (new partner, new office). These have varying appeal such as greenfield having the lowest start-up cost but needs to be bootstrapped, tuck-ins having shared operational gearing and marquee bringing new geographies and office space. Pricing is typically either based on revenue or EBIT with multiples ranging from 0.8-1.2x revenue or 3.5-4.5x EBIT, with average industry EBIT margins of ~17% and typically a 20-30% retention portion based on earnings being ‘maintained’.

The primary risks associated with the investment in my eyes are clearly that it is more dependant than most on the Founder and CEO Brett Kelly. Should something happen to Brett it would be a significant cause for concern, despite how much mitigation he has done to date. Furthermore, their intention to grow internationally is a massive undertaking and requires multiple moving parts to work in harmony, including funding partners, structuring, and expanding the services team to accommodate entirely different geographies, cultural differences, regulations, resources and so on. As the group scales, it is also dependent on if they can enforce metrics on a partnership level as well as they have to date, deterioration in margins and/or lockup for the average firm is entirely possible when Brett has 150 offices under him as opposed to the current 28.

To wrap things up, with the possible elimination of the existing dividend policy (50-70% payout ratio), there is an opportunity to benefit in full from the extremely compelling M&A economics at play here, with focused management and a lot of white space given international expansion plans, even at an enterprise value of ~22x run-rate earnings ($4.80 Cost) it seems feasible that they can double the size of their business every ~3 years (>25% CAGR) without diluting shareholders for the foreseeable future, therefore meeting our total hurdle rate from earnings growth alone.