Kelly+Partners (ASX:KPG) - Deep Dive

Kelly+Partners (ASX:KPG) - Deep Dive

Australian Accounting Firm

About

Growing from two greenfield offices in North Sydney and the Central Coast, Kelly+Partners now consists of 22 operating businesses across 12 locations in Greater Sydney, plus Hong Kong, Auckland and Melbourne from 1 July 2018. In total, we have a team of more than 224 people, including 40 operating partners, who service 5,000 SME clients

Over the past 13 years Kelly+Partners has partnered with numerous accounting firms and built many greenfield offices in order to create the existing network. Our proven ownership and operational structure is unique in the Australian Accounting market. All offices contrain on-the-ground Client Directors who are “owner-drivers” of their respective business in long term partnership with the Kelly+Partners group.

Our operating structure ensures we are focused on:

Careful selection of clients, primarily business owners, families and large private clients.

Limiting the number and type of engagements we undertake, to ensure a thorough and efficient client service

Having the scale to do the best work for our clients , while not losing the personal relationship

Having the depth within the network to bring the right expertise to bear, in order to solve complex business issues

Working together as a team, both internally and with our clients.

The structure and approach of Kelly+Partners attracts talented and dedicated accountants, who in turn enable us to achieve excellent results for our clients in many complex and critical matters.

Locations

Sydney CBD

Central Tablelands

Central Coast

North Sydney

Hong Kong

Northern Beaches

Norwest

Oran Park

South West

Sydney

Southern Highlands

Western Sydney

Wollongong Inner West

Services

Chartered Accounting

Tax Lgal

Private Wealth

Estate Office

Management

Incentives

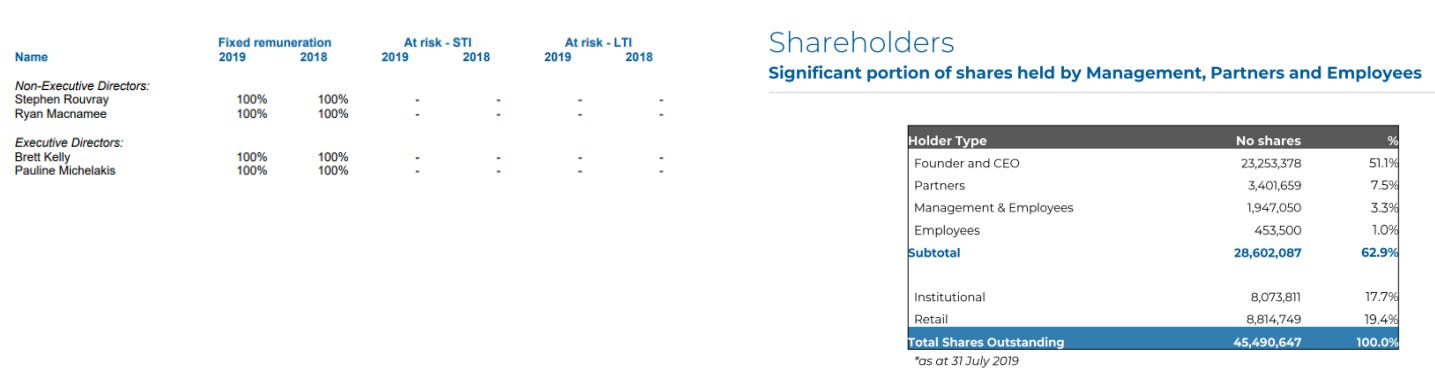

While the remuneration is Fixed completely, the ownership of shares is heavily owner-operated by Brett Kelly. This is excellent long-term alignment of interest even despite the absence of performance incentives. This keeps us away from the whim of a short term bias. It's also worth noting that instituional ownership is somewhat material although not too much so.

Corporate Governance

The Corporate Governance Statement Complies largely in line with what the ASX reccomends. With the following exceptions:

Paul Kuchta Executive Director is a member of the Audit Committee. Justified by the business in reference to the size and complexity of it’s affairs leading to an independent majority audit committee as inappropriate.

Capital Allocation

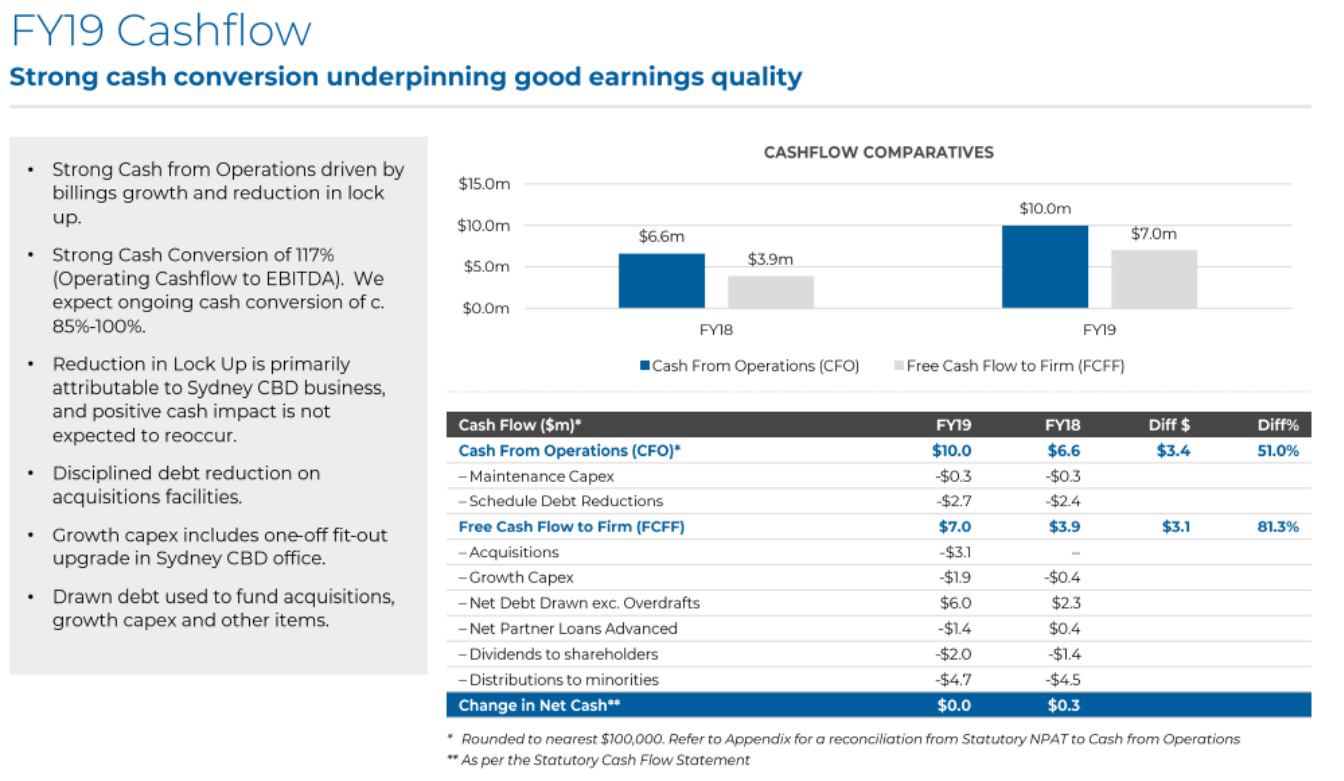

The group has a strong handle on cash flow as expected of professional accountants. Furthermore, their is some valuable information disclosed in presentations such as Maintenance and growth capex, FCFF and various other rare measures.

The Group pays consistent quarterly dividend fully franked with the prospect of paying further special dividends to shareholders when their is non-recurring income that is in excess of working capital. Normal dividends are funded out of free cash flow.

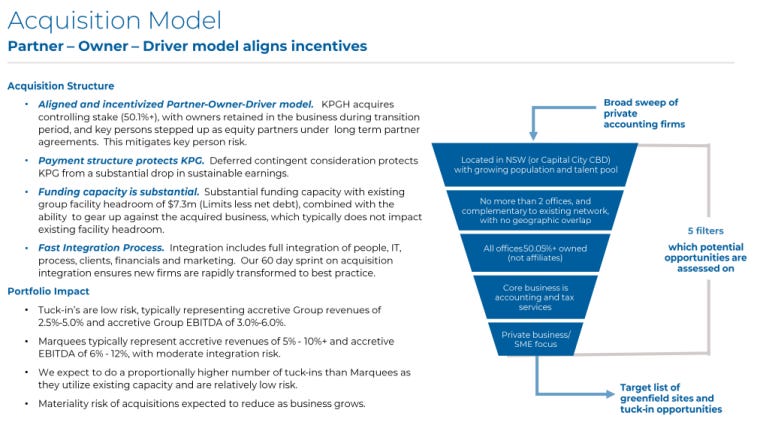

As part of their Growth Plan, Kelly Partners is engaging in aggressive acquisitions. This is aimed to ubcrease revenues but also they reduce risk and only take a minimum controlling interest of 50.1%. This is the incentivise the pprevious owner left on to run the business to the best of their ability. Ingenious.

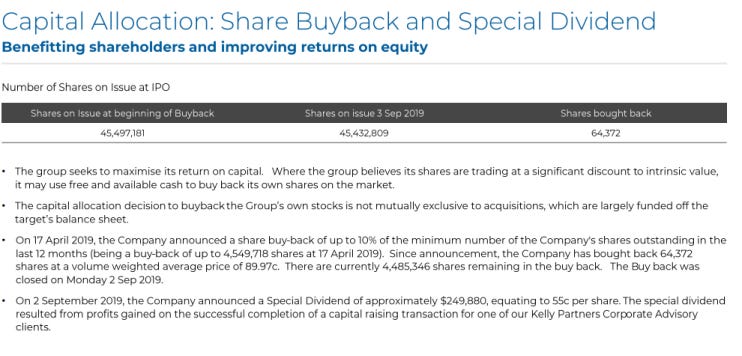

Furthermore the group has a policy to buy-back stock when it believes that it trades at a significant discount to intrinsic value. This is brilliant to see again and reassuring to prospective investors to see.

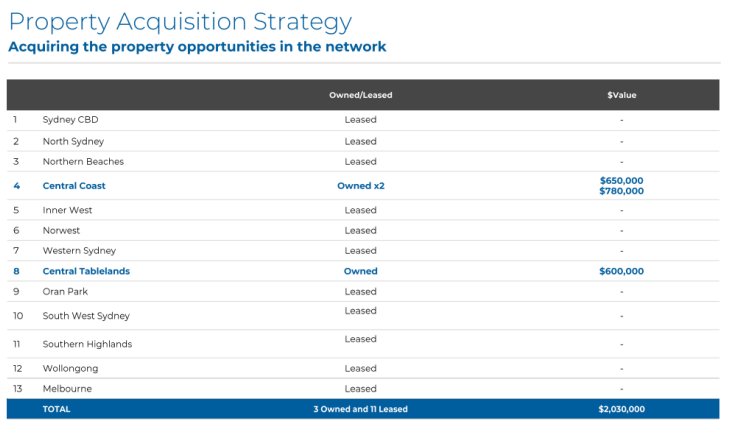

It is also implied that ownership of property is a possibility. This is outlined as shown.

Risks

Key Personnel Risk (Director/Management ability to reach outcomes)

Compression of Margins (Not achieving projected profitability (In particular risk of competition in wealth management)

Loss of key stakeholders (Client retention)

Compliance Risks (AASB, ASIC, ATO, AFSL Requirements)

Corporate Structure (While the arrangements between the Company and each Operating Business do not currently constitute a franchise, if the centralisation and uniformity of the underlying business model were to increase to give further cost efficiencies, then it may have the effect of making the Company a franchisor. If it does it may be subject to addtional compliance costs to comply with franchising law etc.)

Finance Risk (Funding)

Competition

Litigation/arbitration/prosecution

Disruption of business operations (The Company and its clients are exposed to a large range of operational risks relating to both current and future operations. Such operational risks include equipment failure, accidents, fraud, process error, information systems failure, external services failure, industrial action or disputes and natural disasters)

Management and integration of acquired businesses

Relaince on Company's Subsidiaries to distribute a share of profit and pay monthly fees (Intellectual property)

Impairment of intrangible assets (This may be caused by a range of factors, including a failure to achieve expected profit growth, higher than expected expenses, loss of clients, loss of key employees, or the impact of unforeseen events.)

Increased competition for future acquisition opportunities

Information Technology systems and infrastructure

Default in loans

Property leases

Client Satisfaction and Loyalty

Inability to meet forecast financial performance

Registration of trademark and brand risk

Data breach, misuse and breach of privacy

Fundamentals

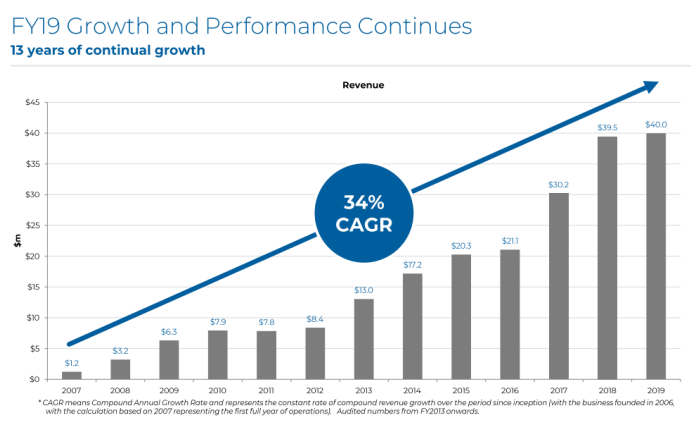

The consistency of revenue growth is very attractive and paints a positive picture for the effectiveness of management. With the 5 year growth plan sales could continue to see strong growth.

The group intends to lower the operating cost of central management services. This will increase the EBITDA margin as a result.

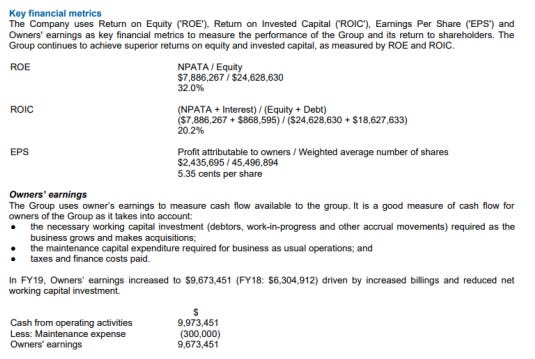

Again, i am impressed with the Key financial metrics the group is focusing on. These are all strong determinents of profitability including Returns on invested capital and also the Warren Buffet coined metric "Owners' Earnings", which is similar to Free cash flow however with some accuracy adjustments. These can be seen as the true earnings attributable to shareholders rather than earnings per share. Which they also track.

These have been strong over the years. If you had focused on Earnings per share you would have been put off by a negative in 2017. However, keep in mind that the firm is full of talented accountants and the best outcome for shareholders is less tax to pay. For this reason the group has used owners' earnings to illustrate the true profitability of the firm. Given a Market Cap of $41.8M, Owners earnings just shy of $5m on a growing company is extremely attractive and can pay back shareholders in just a few years alone.

Conclusion

Kelly+Partners is an Founder led business with a strong incentive lead culture prevalent throughout the business. Brett Kelly is focused on the development of people, which long term represents sustainable value creation. The Tuck-in and Marquee inorganic growth acquisition plan represents a strong development of brand name and awareness, with a hopeful end result of a word-of-mouth/network effect throughout Sydney. This network effect will assist organic growth from customer referrals etc. This combined with a diligent capital allocation turns this into an opportunity i would be glad to hold over time as i watch the business develop. Cash flows are strong and the price seems relatively cheap at 8-9x Owners earnings Adjusted for NCI. Assuming some growth a payback period of 47 years is not outside of imagination. Of course their is some strong competition however, with a fragmented market building market share should not be too hard with significant opportunities abundant.