Kelly+Partners (ASX:KPG) - #2

Kelly+Partners (ASX:KPG) - #2

Australian Accounting Firm

Kelly+Partners is an Australian take on the ‘Holding Company’ structure that bleeds with influence from the likes of excellent Outsider CEOs such as Warren Buffet and Henry Singleton. I say this in due part to the commonalities between them such as having a decentralised organisation, focus on cash flow, valuable capital allocation skills among others. The man behind this is none other than ‘Brett Kelly’, not only the Founder and controlling shareholder of the business, but also an established author of five books, runs a great podcast and has shown genuine interest in servicing his clients to become ‘Better off’ as the corporate slogan would suggest. This post is meant to be just as much a discussion on Brett as a CEO as it is Kelly+Partners as an investment opportunity.

Firstly, the core of the Kelly+Partners operating businesses are a tax-consulting service geared towards small & medium enterprises in the Australian domestic landscape. As the tax legislation grows increasingly complex the value of these services becomes more apparent, diluted by the cliche ‘automation’ of basic functions such as bookkeeping and individual tax returns. But rather than a thesis-breaking factor, automation serves as a shift to more complex work, cutting out the low-margin, low-skilled functions that are bookkeeping and basic taxation. Additionally, Kelly+Partners skews away from a large weighting to the ‘audit’ function as well due to its lack of ongoing relationship that causes it to act more commoditised rather than a lasting and recurring source of revenue for the group.

Additional services such as investment management and financial planning serve their purpose, however pale in priority to the core tax-consulting services. This has been reaffirmed in my opinion by Brett’s comments about wealth management in the 1HFY2020 analyst call:

“We think that wealth management is about the worst business you could possibly invest in. And that the market is obsessed with the business of this crap. It's subject to massive regulatory interference and if anyone can tell me how the value of wealth management business will then be much smarter than I am. Other than that, our internal efforts to grow that business remain very strongly on track. But we've not seen anyone make a fortune for their shareholders in this space, and it's certainly not our focus. We are 100% focused on the quality of accounting firms as the best asset that we can possibly acquire and operate to great effect. And we'll just grow our wealth management business as a derivative of that business, as a support service to that business. So there is an outline of the growth of our complementary services in this pack, Page 20. And you'll see there that the wealth management business continues to grow. I think it's growing at 48% in the period. But I cannot say that I'm excited about owning wealth management businesses. I think the days of lazy trial commissions are over. We can't grow through acquisition because the assets are still dramatically overvalued. We pay dollar for dollar for an accounting firm and people want $3 per dollar for financial planning business. Their margins are lower than ours, say, 25%, we're doing 30%. And the key person dependence on a financial planner is much higher than it is on any of our chartered accountants. So this is not -- we are not enamored of a wealth management business. I've watched all the major banks, your Mac Bank, your Credit Suisse, the Big Four, et cetera, et cetera, do that much shareholder capital on wealth management businesses, but I don't intend to take on that adventure. Most Australians can't afford financial advice, and therefore, won't get any, but they can buy a book at the public library. Go buy one.”

Brett show’s a strong lack of excitement about the business as a whole, which comes as interesting to me since another business I know called Fiducian (ASX:FID) has succeeded brilliantly in the wealth management space, however, that is a topic for another day. In any case, if these businesses can get 25% operating margins and Brett is only seeing acquisitions at like 3x revenues, that’s a poor business prospect in comparison to the 1x or less sales they can purchase accounting firms at with similar margins. In the words of Charlie Munger:

“In the real world, you have to find something that you can understand that’s the best you have available. And once you’ve found the best thing, then you measure everything against that because it’s your opportunity cost. That’s the way small sums of money should be invested. And the trick, of course, is getting enough expertise that your opportunity cost — meaning your default option, which is still pretty good — is very high.”

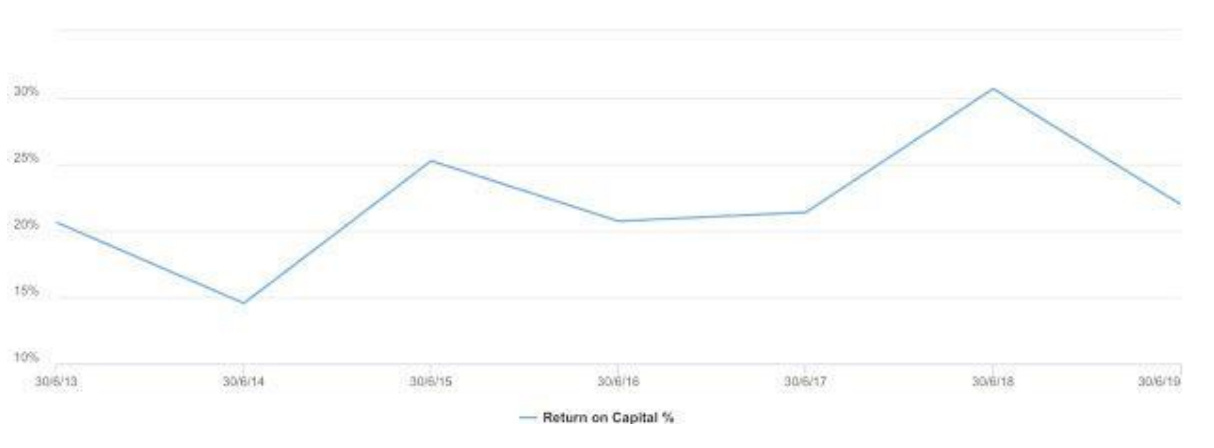

The opportunity cost to fleshing out the wealth management arm inorganically is acquiring more accounting firms. So using that as the benchmark at a industry normal multiple of 1x sales, Brett can pretty easily be earning 20c+ in the dollar if he buys an accounting firm at 1x sales or less due to their decentralised organisation structure which i will talk more about later on. In any case, these returns are 20%+ returns on invested capital which reflects nicely in the accounts (Even on a consolidated basis). Comparing these to if they had been acquiring financial planning firms, the returns on capital would be well less than half what they can achieve with accounting firms.

So talking more about these acquisitions, what makes this a sustainable source of inorganic growth? There are some important competitive advantages here that places Kelly+Partners in the position to benefit from this for years or decades to come. Namely that the average age of private accounting firms directors in the industry is roughly 50 years old. As a result there is a ripe trend of succession planning issues in the industry as the transfer of firms occurs at a rapid pace.

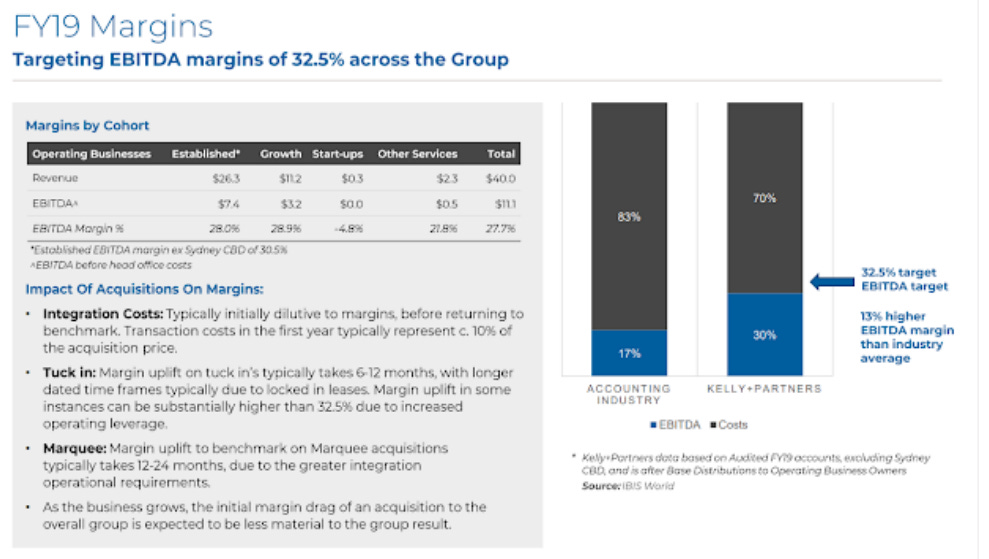

A report on succession in the industry by the CPA outlines some important trends that I think are worth a mention to support the market for acquisitions going forward. Regarding valuation, it is generally accepted that firms go for 1x sales or less or alternatively, 4x EBITDA or less in aggregate.

This bodes well for KPG and their acquisition strategy for lets assume that they pay 1x sales. Then the margins will gradually reach the group average of 30%, which is a payback period of 3-4 years (More likely to be 4 as they will need to post merger integrate). That's an excellent structural advantage to a roll-up strategy. The average firms margins are only 17% so a multiple of EBITDA is even more favourable for KPG and in most cases can acquire at well below 1x sales.

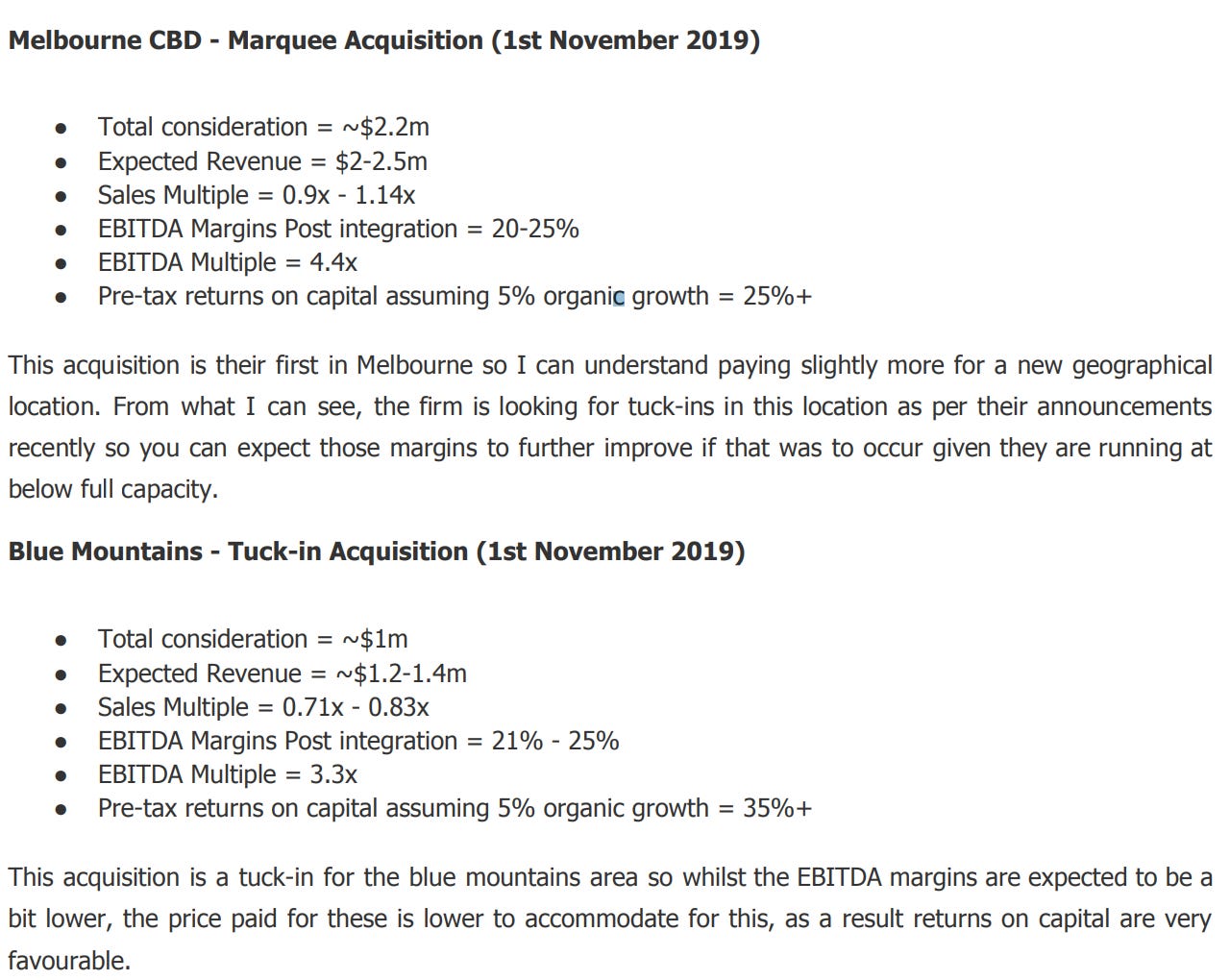

Some examples of their acquisitions outlined below:

The last thing i wanted to mention was the similarities between this business and the Outsider CEOs covered in the popular William Thorndike book "The Outsiders". The main points i wanted to mention about Teledyne are highlighted below:

The CEO as an investor - Singleton ran an organisation which allowed a focus on capital allocation

Decentralised organisations - Few employees at the corporate level

Investment philosophy - Focused investments in industries they knew well

Dividends - Teledyne didn't pay a dividend for the first 26 years as a public company

Significant CEO ownership

A shift from an aggressive acquisition strategy to a buy-back strategy.

The Kelly+Partners translation is as follows:

The CEO as an investor - Brett structures acquisitions to leave subsidiary directors on at a 49% ownership. This makes this more of a 'participation' decision rather than completely taking on the operation of that business.

Decentralised organisation - Group wide marketing and proprietary processes are issued at the corporate level throughout the organisation, allowing it to be more efficient and hence their margins are well above the industry

Investment philosophy - Private accounting firm focus as mentioned earlier

Dividends - Kelly+Partners does pay a modest dividend at some 2/5 of my estimate of owners earnings, however, Singleton didn't do this in teledyne as the dividends were taxed both at the corporate and individual level. With the existence of Australia's imputation credits system, the appeal of issuing dividends is increased significantly as a result.

Significant CEO ownership - Brett owns 50% of the company, allowing him to think as an owner

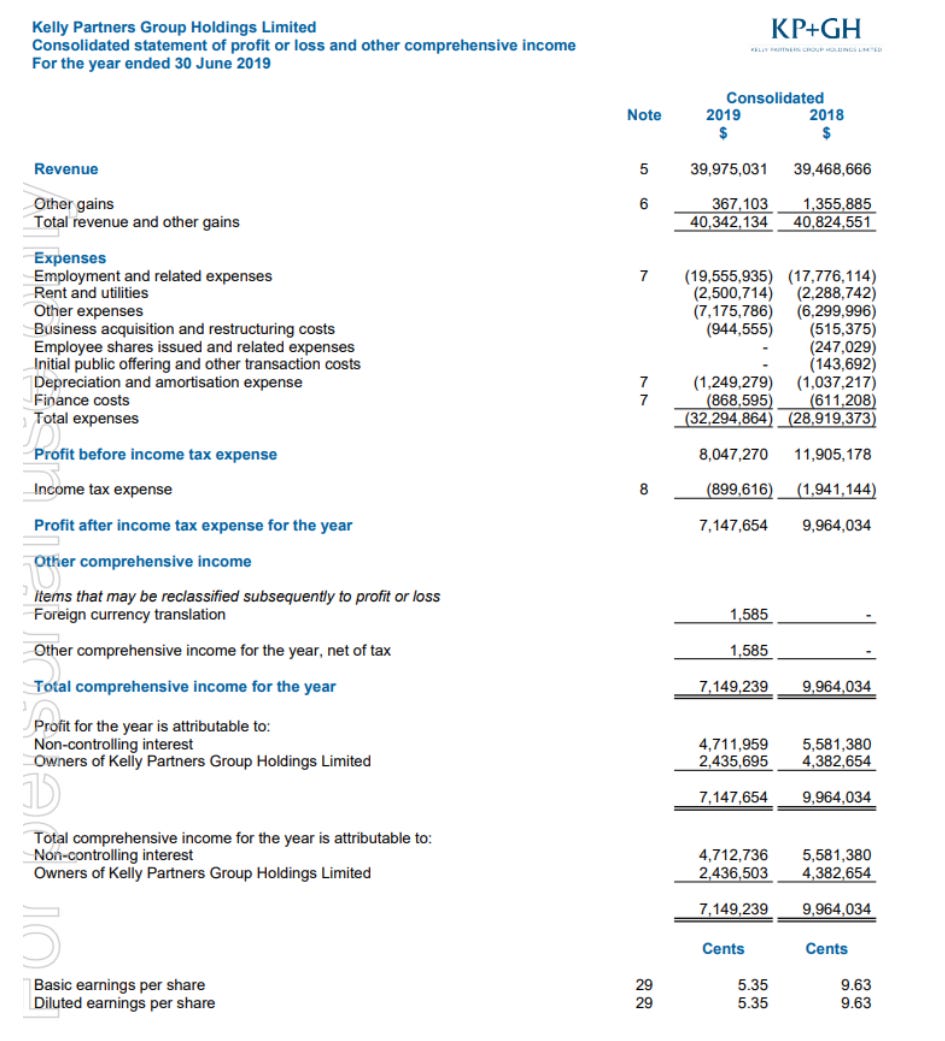

The last point I will need to flesh out more to illustrate my attraction to Kelly+Partners as a long term investment thesis. First of all I need to show the profit & loss.

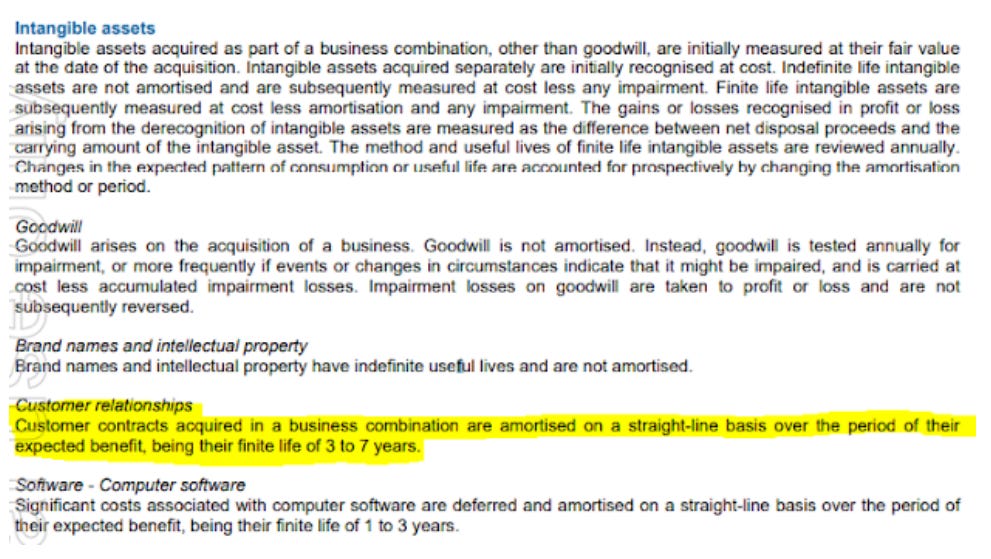

The key points of interest here are the acquisition and D&A costs that i believe are growth related and represent a misjudgement by the market of the underlying profitability of this business. For the financial years 2019 & 2018 respectively, these have made up ~5% and 2.7% of the revenue. The majority of this costs constitutes amortisation specifically Customer relationships.

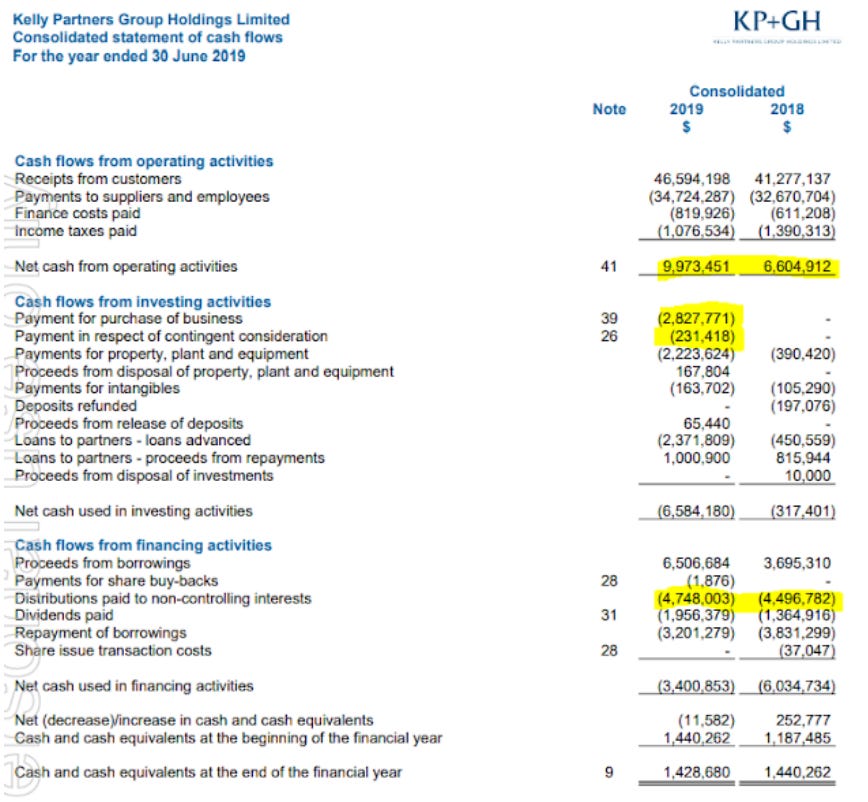

These costs only arise because the group is acquiring new firms, and they don't constitute an impact on the cash flow of the group. Speaking of the cash flow, the cash flow statement looks confusing at first as well, however with some context you can see the claim that the business is indeed capital light.

I reached this conclusion after reading the notes and some commentary around how the partners can act at the subsidiary level. First of all, the cash flow from operations is your starting point.

Moving down the statement, the purchase of business & Contingent consideration is exactly what you'd expect, with the purchase line being the cash consideration up front on acquisitions through the year, and the contingency being settled in cash. That can stay at the parent level as attributable expenses to owners.

The property, plant and equipment in the investing activities are growth related capex for the fitout of the Sydney CBD Office and a new IT System. These are one-off in nature.

Loans to partners are amounts borrowed by minority interest to help them purchase their stake in the business. These amounts are typically repaid over a 4-8 year period.

Lastly, the non-controlling interest distribution is the 49% interest to the minority partners. Importantly this is them drawing on their equity account, it may not exactly equal their profit dist. for the year.

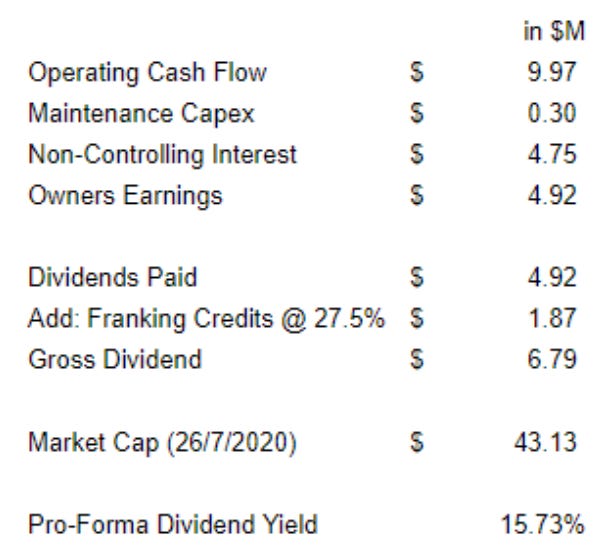

So the easiest way to illustrate the disconnect between price and value would be to assume no acquisitions were made and the entire owners earnings was paid to shareholders of the parent company.

So why does this discrepancy exist and more importantly, what is going to make the market realise the underlying profitability of Kelly+Partners? Well in my opinion the business will continue to look cheap until the business reaches a point in time where the group stops acquiring businesses and the removal of the acquisition costs creates some relief on statutory profit margins. We saw this relief briefly in 2018 as the net profit margin spiked to 11%, which in my estimation is about the correct owners earnings margin on a normalised basis.

In general periods of no acquisitions will show stronger margins on a statutory basis and it's in those periods where i expect the market to get excited about the stock, conversely the opposite will be the case, so long as an investor knows this dynamic they can have to conviction to expect these volatile bouts of activity in the stock

This creates some difficulty in the appropriateness of buybacks for Brett as it's in periods of high levels of reinvestment where the stock i expect will get cheaper, however the cash is being utilised for acquisitions. In any case, the relation to Teledyne is that if these acquisitions stop, the market would appraise this appropriately to account for the unusually large dividend yield. If organic growth was to be estimated at 5% a year, it would be appropriate for this business to be trading at a 20-30x multiple of profits depending on what the market does with the pricing of franking credits.

The way i derived this is with the assumption that the market long term average return is 10% p.a. If a business grows 5% a year without the requirement of reinvestment, the remaining % can come from the payout of excess profits to shareholders, assuming the reinvestment of these dividends and no further movement in the multiple, the investor would receive market matching returns long term.

So there you have it, an excellent business with above industry margins that allows for structurally cheap acquisitions trading at a depressed valuation due to deductible acquisition costs. What more can an investor want?