Kelly+Partners (ASX:KPG) - #3 - Deep Dive

Kelly+Partners (ASX:KPG) - #3 - Deep Dive

Australian Accounting Firm

Introduction

Kelly+Partners (K+P) Group Holdings is a listed holding company that owns a controlling stake in accounting firms throughout Australia. These businesses primarily provide accounting and taxation services to private small and medium enterprises along with complementary services.

K+P was founded in 2006 by current CEO Brett Kelly, a 46 year old man that grew up in the inner west of Sydney, graduating from the University of Technology, Sydney (BBus) and then from the University of New South Wales (MTax) together with completing his studies to be admitted as a chartered accountant.

Before founding K+P, Brett started at PwC as an Undergraduate where he spent 5 years before leaving to work at Schroders for 5 years in Corporate Finance. During this time he also wrote four best-selling books.

During the course of this write-up I want to first define some key competencies I believe are prevalent in the K+P model and expand on why and how that is so before outlining what this means in terms of value creation for shareholders.

Industry Backdrop

The SME and HNWI focused accounting space is one of extreme breadth and continuing complexity. To add to the foundations of tax knowledge, there are specific sets of rules in this low turnover space that make it particularly important to get valuable and informed advice from a professional. This is where the accountant stands, the interpreter of this constant stream of law change can do more than simply advise based on the lagging indicator of financial information, but also propose scenarios and plan ahead to optimise a client's situation.

The law doesn’t make starting and operating a business particularly obvious to the layman, and even if they do get a handle of it, there is a stream of ongoing reporting obligations and grants or concessions available depending on their business model and specific situation. Some niche examples include the interpretation and application of Personal Services tests, application of the SBE ruling and aggregated turnover tests, and interpretation of workers compensation and the implication of the gig economy on PAYG obligations

These aren’t some simple things that can be automated through a software program, there are minor amounts of it in software I have seen such as the TPAR reports in Xero etc. However, this requires input to provide an output, and without the proper knowledge, such a thing would be impossible for any normal business owner to constantly keep on top of.

I hope this provides an insight into the importance of an advisor and the switching costs associated due to the complexity of an individual business owners situation, especially if they are operating a multi-entity structure, which from my experience is the majority of clients I have worked with personally.

As for the industry itself, business owners are spoiled for choice when it comes to choosing an accountant that they wish to partner with, and for the most part it’s not clear as to who to choose and why to choose them. For this reason there are industry bodies that provide professional designations (CPA/CA, SMSF Association etc.) that give a hint as to each advisor's skill level in each area.

For a client a jack of all trades is likely to be what they need however, quality advice also requires breadth of knowledge. Dealing with SMEs is an engagement that requires the cooperative efforts of advice covering each area of an individual's taxable positions for maximum effect. You don’t make a big tax decision without knowing their taxable position on their superannuation, investments, business entities or welfare entitlements etc which takes us to the topic of the K+P ‘Flight Plan’ and the importance of vertical integration.

Flight Plan & The Integrated Client Advice Model

“Don’t find customers for your products, find products for your customers”

~ Seth Godin

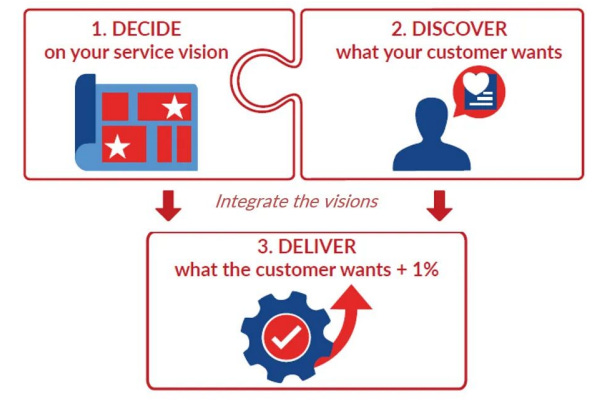

These two categories are what the company considers to be it’s intellectual property. They are separated in the prospectus, but I believe the terms are fairly interchangeable so I'll refer to them collectively as the ‘Flight Plan’ for the purposes of this discussion.

This refers to their systems to act as business advisors and assist clients to achieve their goals. Complementary services within the group provide in house opportunities for clients to achieve their goals with intimate and personalised attention. Such examples include the recently announced Insurance Broker Partnership, Alternative Investments, K+P Investment Office, Tax Legal, Estate Planning & others. These services provide opportunity for internal cross-selling, increasing the revenue for the group on a per client basis should they take up these opportunities.

I believe these are mostly optionality as an investor and are difficult to put a number on, however, the fact remains that these are REAL businesses and could very well scale to become material contributions to the group in their own right. The best part is the minimal amount of capital required to start these and operate them on an ongoing basis. Brett can correct me himself if I'm wrong, but profitable on the first $1 of revenue and every dollar after that is to be expected from these embryonic businesses.

Having read the book “Raving Fans” by Kevin Blanchard, one of the books on the Kelly+Partners reading list I can see how the 3 step process of creating these raving fan clients is present in the business. There is the Kelly+Partners vision of making clients “Better Off” and discovering what the customer wants. But providing these additional services and business planning is undoubtedly the +1% that creates raving fans.

The annuity style revenue that K+P claim to have really is not an overstatement, with only ~2% client churn and positive net retention growth, the revenue of the group really is extremely stable and is one of the most attractive traits that the business has, thanks to the quality service that K+P provides and competitive and fair pricing.

Lockup

“Revenue is vanity, profit is sanity, but cash is king”

~ Unknown

If there was one metric I would say is the most important for an accounting business, ‘Lockup’ would certainly be a strong contender. It’s in this regard that K+P really shines, relaying that an intense focus on recruiting talent and people pays off with excellent productivity and cash conversion.

Lockup is simply the $ value of debtors & unbilled work in the business, best expressed in the number of days it illustrates the time it takes to begin a job, bill it and receive the cash. Specifically the formula for working this out is:

This can be further broken down into the number of days it takes to be paid or ‘debtor days’ and the number of days it takes to bill or ‘WIP days’. WIP days in particular is something I want to highlight as extremely important and is a clearly observable strength of K+P. To set the scene, the industry average is 24 WIP days and 53 debtor days for a total of 77 Lockup days. That means that if your business is generating $10m in sales, the average firm would be stuck with 77/365 x 10m = $2.1m in receivables and WIP, in a ratio of basically ⅔ receivables and ⅓ WIP.

As at 30 June 2020, K+P had a total Lockup of 54 days, split into just ~9 WIP days & ~45 debtor days. This tells us 2 things:

K+P employees are 2-3 times as productive and;

Cash collections are ~15% more efficient than the industry.

First of all I want to expand on productivity, as it’s a key competitive advantage K+P benefits from.

Productivity

“The power of the people is much stronger than the people in power”

~ Wael Ghonim

Employee productivity in Accounting firms generally can be expressed by asking questions such as ‘Which jobs do i have enough information to start and finish without having to wait for client turnaround’ and ‘Am I billing enough?’. Of course these are just outputs to inputs, and those inputs are determined by the culture which motivates them.

K+P approaches this by acting in a meritocratic fashion, rewarding employees for exceptional work with rapid career progression & recognition. This incentive driven environment is prevalent from the lowest level employees through to the top. This ties in with their acquisitive nature, constantly providing opportunities to step up and fill new roles.

In addition to this, there are staff amenities such as the sustenance bar stocked with snacks, the ability to work remotely thanks to their 5 year subscription with Citrix. More recently K+P has announced that they have become a certified ‘B-Corp’ company. B-Corp is a global initiative that represents leading businesses that essentially treat all stakeholders whether it be employees, community, customers or suppliers with excellent conduct. In a sense it’s a nod to sustainability, something worth deliberating over when investing over longer time frames.

Brett has always emphasised the importance of fostering talented individuals at all levels of the business. The importance of treating stakeholders as human beings can not be overstated, and this incentive driven structure is certainly reassuring long-term. Majority insider ownership of the head co with the operating partners owning keeps everyone accountable for the long term goals of creating value for all parties involved.

“The moment you feel the need to tightly manage someone, you’ve made a hiring mistake.”

~ James C. Collins, Good to Great

This quote from Mr Collins is an excellent one in which I want to explore further. I think the most important hire is undoubtedly the client director one. This person sits between Brett and the employees, they ultimately drive client retention, cash collections and push employees to improve WIP.

Monthly One-on-One Meetings that partners have with their employees encourage ongoing feedback and prevent employees from stagnating in their career path. There is always something that they can improve on. Quarterly directors meetings that Brett has with the group partners to catch up. Half yearly catch up with seniors and an annual retreat for all the partners.

The monthly meetings in particular are especially helpful for managing workload, this keeps WIP days as low as possible and any inefficiencies in collection can be discussed regularly, both via conversation from partner to employee and from Group to partnership.

Brett says that the firm strives to drive internal succession/promotion and avoid lateral hires, this makes sense as I would assume it assists with employee retention, operational efficiency and keeping HR costs low.

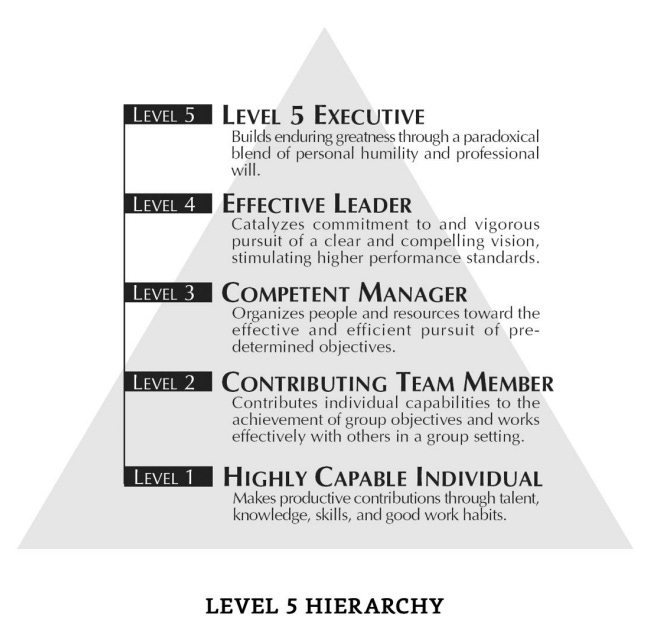

I think this is summarised best in the ‘Level 5 Leadership’ diagram that outlines the hierarchy of many ‘Good to Great’ businesses - a concept where I can see much of within K+P. Brett credits success to his ‘people’ often rather than acting self-absorbed. Another concept from this book which I see without a doubt strong influence from is the ‘Genius with thousand helpers’ model in which Brett has a strong vision and has surrounded himself with people who can help him achieve it.

Partner-Owner-Driver™

“Show me the incentives and I will show you the outcome”

~ Charlie Munger

This focus on productivity as talked about is backed by culture, but also from a strong incentive driven model. A model that K+P has dubbed the ‘Partner-Owner-Driver’ (POD) model. In short this involves the listed parent company (KPG) acquiring a 51%+ interest in each subsidiary to drive long-term strategic alignment and provide a pathway to succession.

There are many benefits to joining the network of K+P partners, lightly covering them I would emphasise Lockup improvement, expense reductions, succession planning and employee career development. I did want to avoid talking too much about numbers, however I believe a scenario illustrates the value to a seller that K+P provides.

In my interpretation the main value that K+P can provide in financial terms is:

Partial exit upfront via giving up 51% interest (Assume 1x sales - Industry Average) or ~3 years worth of historical pre-tax cash flow (~17.6% margins)

Working capital relief - Can pull some equity out of the business once lockup is reduced (77 days to 54 days)

Operating Leverage - After cost cutting and centralised Back office, not much sacrifice in ongoing profitability if any ~(17.6% margins > 32.5%+ margins). Partner gets 32.5% x 49% and also has to pay 9% x 49% to the parent company as the back office and IP fees. So they will pocket ~11.5% in pre-tax distributions. So the average partner is getting $1.1m in revenue, at 11.5% they will pocket ~$125k in pre-tax partnership distributions.

An important note on non-financial benefits here is that the centralised back office support and use of the flight plan model outlined earlier. They will also gain benefit to a single branded group and IP. But the main attraction here is as a medium of succession. Brett has said on an interview with Alan Kohler:\

“The best way to describe what they do is miniature leveraged buy-outs where the vendor is taking some risk with us to do the succession of their firm and we are providing the expertise and the succession team to allow that firm to continue for the benefit of its clients and its team.”

Value Creation

"We aim to pay moderate dividends, make disciplined (occasionally large) acquisitions, use leverage selectively, manage our capital, minimise taxes, run a decentralized organisation, and focus on cash flow over reported net income."

~ Brett Kelly, 1H19 Chairman’s Letter

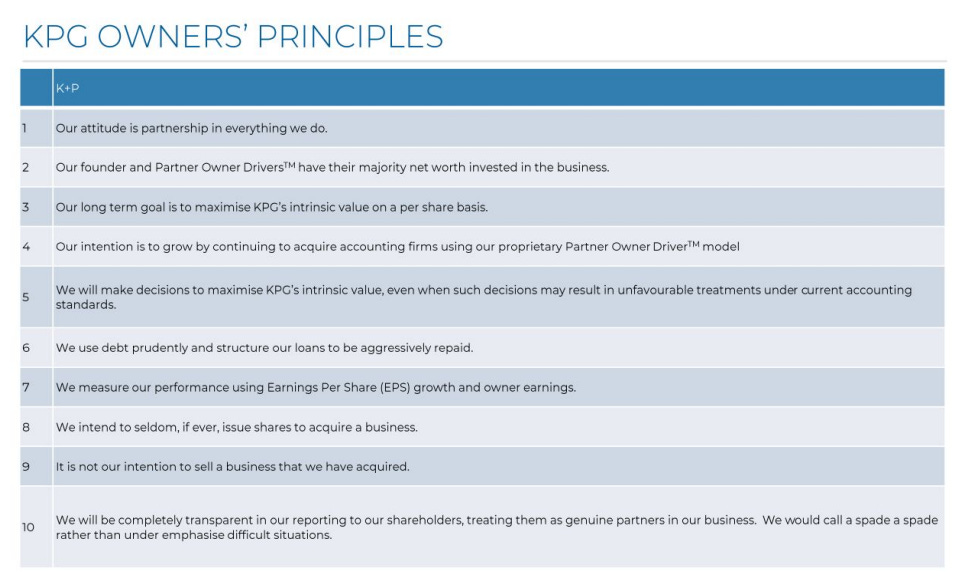

I’m sure this is what most of the readers have been waiting for, and I assure you I will try not to disappoint. Firstly the shareholders principles:

These principles I have covered in part - namely the partnership attitude and POD model. But I think what i want to talk about here is how the company uses its capital structure and operating efficiency to maximum potential to create high returns for shareholders.

As I alluded to early on in the write-up the market of SME accounting is a highly fragmented one with over 10,000 firms nationwide, this creates an opportunity for a differentiated firm to capture market share through acquisitions. The underlying industry itself is very stable and has a normal rule of thumb selling price for firms at ~1x a firm’s revenue.

This proves to be extremely beneficial for K+P as they can turn $1 of parent distributions into ~$0.20-0.25 for the parent company shareholders on a post-tax basis. This equates to a Price/Earnings multiple of just 4-5x. To top this off there are some benefits from the flight plan model and regular price elevators that means the operating partnerships can sustain ~5% growth in most years without putting additional capital into them. Lastly, their top class lockup days allows them to reduce the working capital in the business and distribute any excess as a capital distribution in the respective ownership %. This should provide some context to their stellar returns on capital deployed of 25%+.

Speaking of the ownership %, the recent results since the IPO have been depressed for a number of reasons, namely the decision to reinvest into the parent company in excess of the parent IP & Centralised back office fees which as I mentioned before is 9% of the operating subsidiaries revenues. These fees, once paid, are used to scale the operations of the parent company in order to handle marketing and support functions over a larger group network among other functions. This has led to parent company NPATA being depressed in excess of the owners earnings attributable to the parent company shareholders. Absent this reinvestment, the difference between the NPAT of the NCI and parent portions will be the tax paid on the parent (Parent is post tax company profits, NCI is pre tax partnership distributions) of ~30%.

Regarding the capital structure it is important to understand the different types of debt held in the business and management intention regarding the suitable amount of leverage to carry. The debt carried on the consolidated financial statements isn’t exactly transparent in its structure, however, thankfully they provide a coherent breakdown of that debt, the types are stated below:

Parent Debt

Working Capital Debt

Acquisition & Other Term Debt

Operating Businesses

Working Capital Debt

Property Debt

Acquisition & Other Term Debt (Includes Partner Buy-in Funding)

Especially important is the Partner Buy-in funding as that makes up a lot of what is causing the consolidated financials to look poor. These loans primarily represent amounts of money which have first been borrowed on the balance sheets of those operating subsidiaries and then secondly on lent to partners to assist them with their purchase of equity into that entity. This results in the financial statements having both a financial liability and a financial asset to the partner, however, it is only attributable to the Non-controlling interest portion of the operating subsidiaries. Similarly, the group provides the option to purchase property and use the partnership to carry the debt, however, once again this is attributable to the partner, not the parent entity. This leaves the working capital debt, which is largely attributable to both the parent and partners in their respective ownership percentages. Lastly, the group carries debt at the parent level to provide working capital and acquisition funding.

As a capital allocator you have a number of choices when deploying capital, you can use internally generated cash or externally generated debt or equity. With this capital you can buyback shares, reinvest into the business, buy new businesses, pay dividends or pay down debt. Brett has a good balance of everything with priority towards network expansion, unsurprisingly as they tend to offer the best returns on that capital. A progressive dividend policy on a monthly basis has predetermined claim to some 40-50% of the current earnings, which Brett has stated he intends to grow by 10% a year or more. My guess would be to maintain a similar payout ratio and escalate the dividend in line with long term revenue growth. He also opportunistically repurchases parent company shares when it is at a discount to intrinsic value.

When viewing acquisitions, the group relays intent to keep the financial leverage of the group at certain ranges. Brett has stated that this would be ~1-1.5x Net debt/Underlying EBITDA with allowance to spike to 2x for large acquisitions. This means it’s incorrect to look at this business on an enterprise value basis as they have no intent to deleverage their business whilst there are still thousands of potential opportunities out there. It’s in my observation that for every dollar of additional debt they borrow, given the group EBITDA margins they also unlock $0.33 in borrowing power (After integration). This provides them the ability to really be quite acquisitive as a business and keep reinvestment rates quite high.

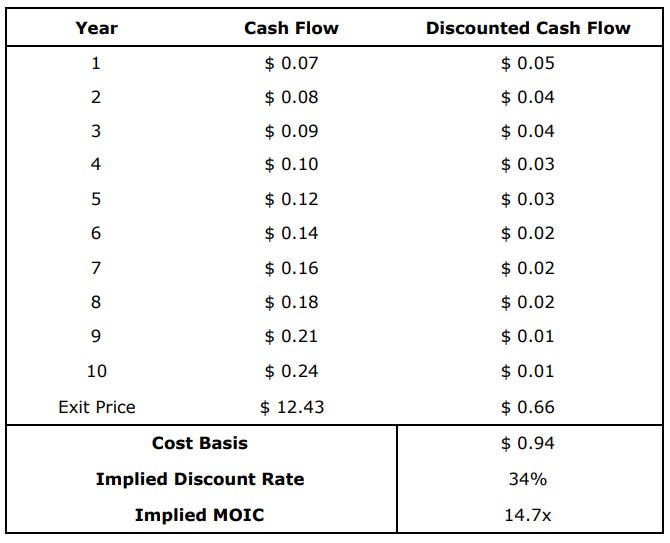

Speaking of intrinsic value, to conclude this write up I want to provide a very simple and clear valuation proposal to the keen long term holder of this business, both at the current price and at my personal cost base. I will show this in Reverse DCF form for accuracy however, it is very easy to do this with back of the envelope math.

The main assumptions are:

The business can turn 12.5% of Group Sales into NPATA for the Parent Shareholders

10 Year Holding Period

Pays out 50% of NPATA as a Fully Franked Dividend

The remaining 50% is allocated at 20% Returns on Capital

The Group can also grow organically by 5% per year

On receipt of dividends a marginal tax rate of 34.5% applies, after grossing up for Franking Credits

Exit Price of 3x the Group Sales or 24x Normalised NPATA

Interpreting this means that by paying a 7x PE for the business at cost, I am setting myself up very favourably for future returns that well exceed most investments in the markets. This is my best find to date and just so happens to resonate greatly with my core competency being an accountant in the exact niche this business operates in.

Even if this does not perform to expectations, there is an extremely large margin of safety that will allow me to comfortably hold this without cause for concern. I believe that Brett and the team at K+P are excellent stewards of capital and frankly, the returns could even exceed what I have shown above, I merely used what I think is a realistic outcome based on my research of the business.

I hope you enjoyed this deep dive into this wonderful business and stay tuned as I plan to write more short-medium form analysis as I develop my watchlist and portfolio.