Litigation Capital Management (LON:LIT) - One Page Stock Pitch

Litigation Capital Management (LON:LIT) - One Page Stock Pitch

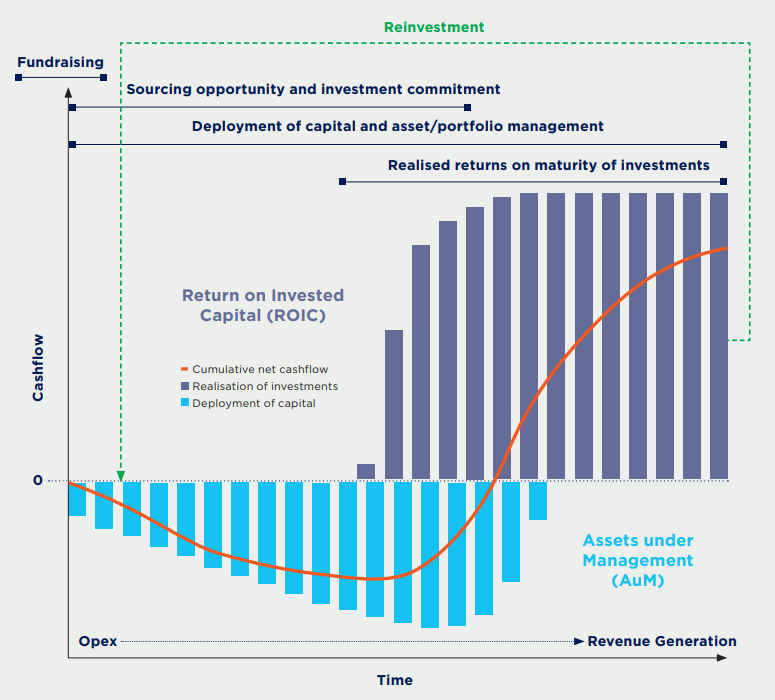

Litigation Finance - A Medium term inflection point using third-party money

Litigation Capital Management (LCM) is one of the pioneers of Litigation Finance, a concept that originated in the 90s in Australia. It involves the assumption of financial risk associated with legal claims in exchange for a share of the amounts recovered. It covers the costs such as solicitor’s fees, barrister’s fees and court fees in addition to providing indemnity to adverse costs (They insure against this).

The skill of underwriting is of utmost importance and the success of which is able to be monitored through the win/loss ratio and the returns on capital deployed over time. Before getting into the business model I will describe the accounting behind how investments work. These cases tend to last for anywhere between 2.5 and 4 years and the cash inflow isn’t received until the case is successful. This results in cash inflows that lag outflows. But due to LCM accounting on a cost basis, the capital that is recoverable is classified as a contract asset on the balance sheet until the performance obligation is met. Non-recoverable operating expenses are still expensed when they occur, so you will see those on the profit & loss.

The accounting entries would be as follows (Ignoring Tax effects and Debtors/Creditors):

Capital Invested

Debit - Contract Assets

Credit - Cash at Bank

Non-Recoverable Operating Expenses

Debit - Various Operating Expenses

Credit - Cash at Bank

Fulfillment of Performance Obligation

Debit - Cost of Sales

Credit - Contract Assets

Receipt of Invested Capital + Returns on Capital

Debit - Cash

Credit - Revenue

This means that accounting at cost can be misleading when trying to estimate future cash flows if you look at it like a normal business. Now onto the Business Model, of which there are 2 parts to this business, Direct balance sheet investments and Third Party Asset Management.

Direct Investments is largely as I explained above. Investment into cases of which a return on capital is generated directly as a result of that outcome.

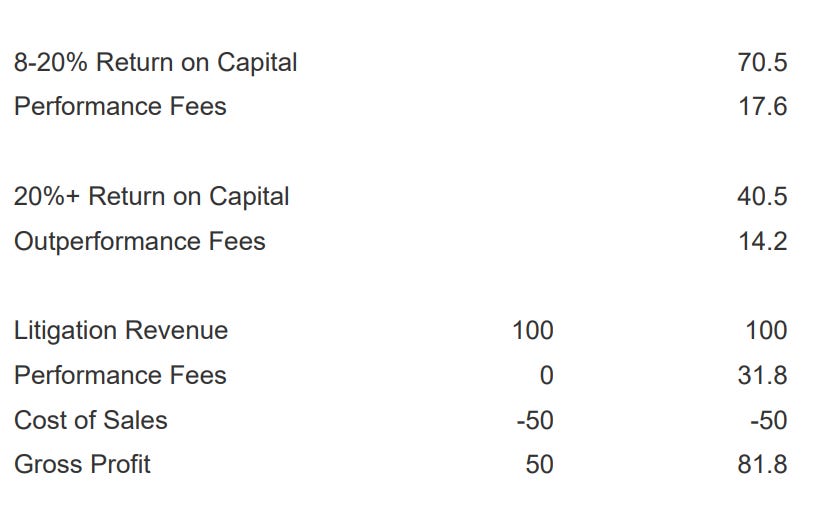

The asset management business operates on a tiered basis and utilises outside capital to grow via float. This gives them scale to pursue larger cases and increase their investable universe. On a consolidated fund basis the accounting is exactly the same however, for shareholders it is important to consider how performance fees act accretively to LCM returns. You might consider the hurdles of 8% for performance and 20% for outperformance quite high but given their 9 year weighted average IRR of 78% LCM’s claim that they expect to be entitled to outperformance fees on the majority of investments is genuine in my opinion.

An example of how I see this is if they were to invest 100m into direct orr asset management and receive a 2x multiple of invested capital over a 3 year period (25% IRR) the returns would look like such (Does not include operating expenses or taxes).

Of course with this increased scale you would typically have larger cases to elongate the average time to settlement as defendants typically fight longer and harder so that’s why I went with the lower MOIC than the weighted average of ~2.4x. Furthermore increased scale from the fund requires increased deal flow of which I can report a strong growing demand at 522 in FY2020 as opposed to 125 in FY2018. The group states that ~5% of applications get through their due diligence process.

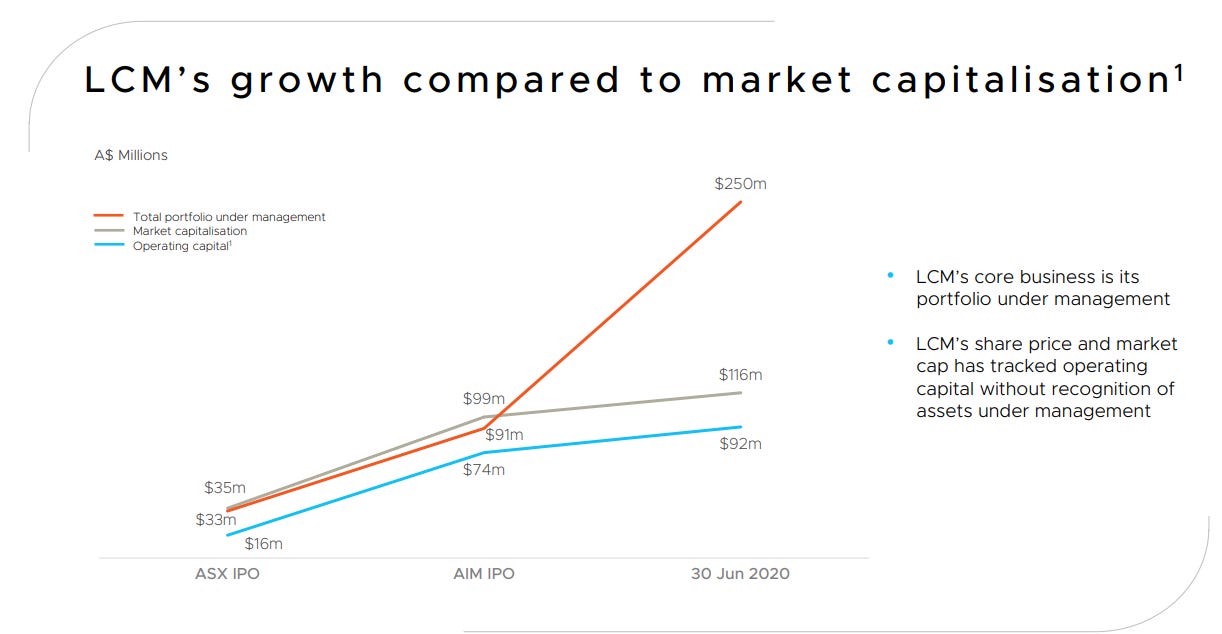

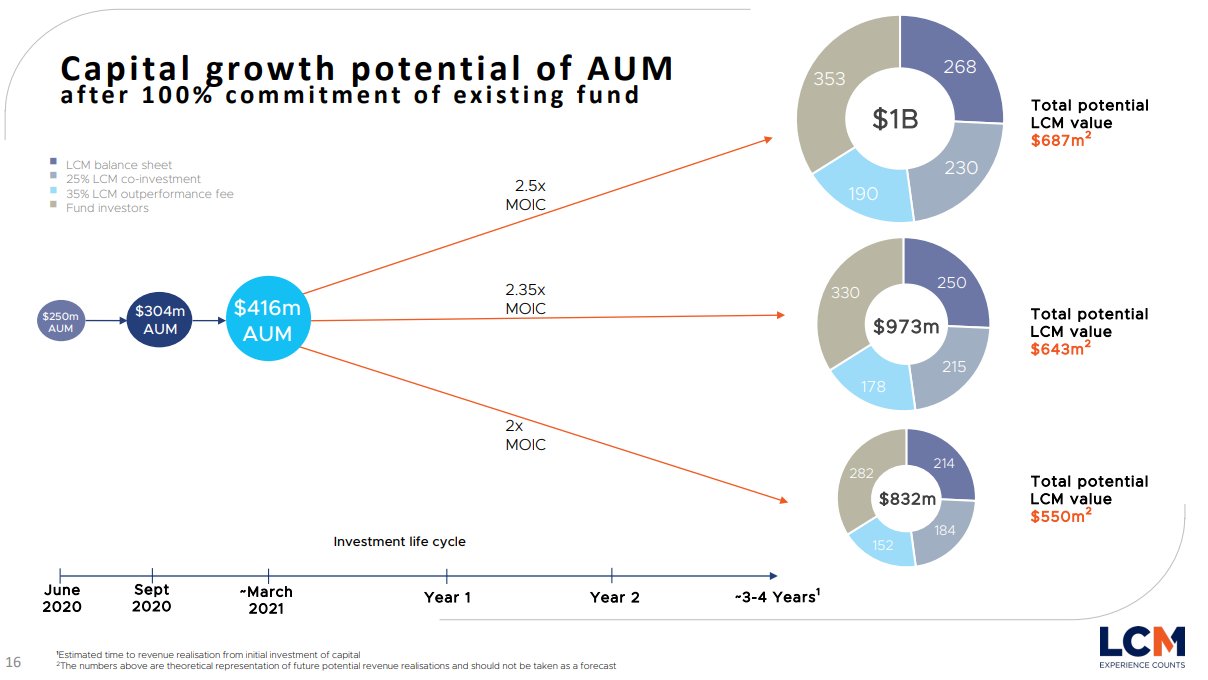

Now to demonstrate where I see the current value in LCM, the business has historically grown in line with the operating expenses of the business, but is not pricing in that their is economies of scale benefits with a larger asset base, this particular slide should give some clarity to the potential disconnect from intrinsic value and market capitalisation.

To note that of this $250m, 64m is the co-investment to the Asset Management business. Thankfully the business has given another useful slide which demonstrates the latent potential of future realisations and performance fees.

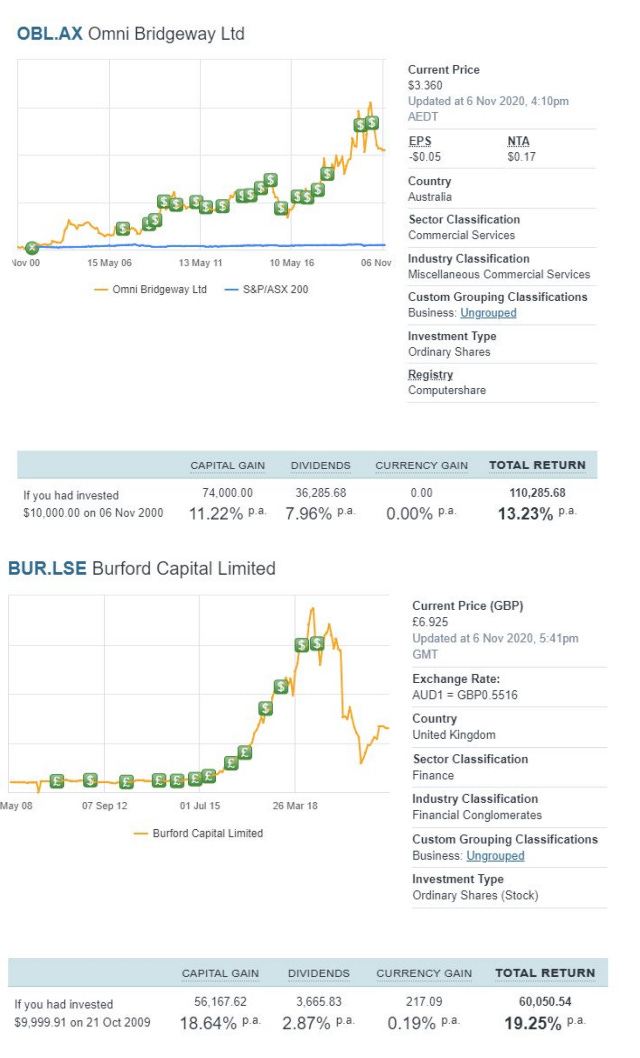

Similar businesses in this field that I have looked at include burford capital and Omni Bridgeway (Previously IMF Bentham). The Performance of each stock is below (Burford listed in 2009).