Nuvectra (OTC:NVTRQ) - One Page Stock Pitch

Nuvectra (OTC:NVTRQ) - One Page Stock Pitch

Biotech Liquidation Play

Nuvectra Corporation is a neurostimulation company that focuses on helping physicians to improve the lives of people with chronic neurological conditions. The Company's Algovita Spinal Cord Stimulation SCS System Algovita) is the Company's commercial offering and is Conformite Europeene CE marked and the United States Food and Drug Administration FDA approved for the treatment of chronic pain of the trunk and/or limbs. Its technology platform also has capabilities under development to support other neurological indications, such as sacral nerve stimulation SNS and deep brain stimulation DBS. In addition, its NeuroNexus Technologies, Inc. NeuroNexus) subsidiary designs, manufactures and markets neural-interface technologies for the neuroscience clinical research market. Its Virtis is an application of the Company's neurostimulation technology platform and its first product for the SNS market. Its subsidiaries include Algostim, LLC Algostim) and PelviStim LLC PelviStim).

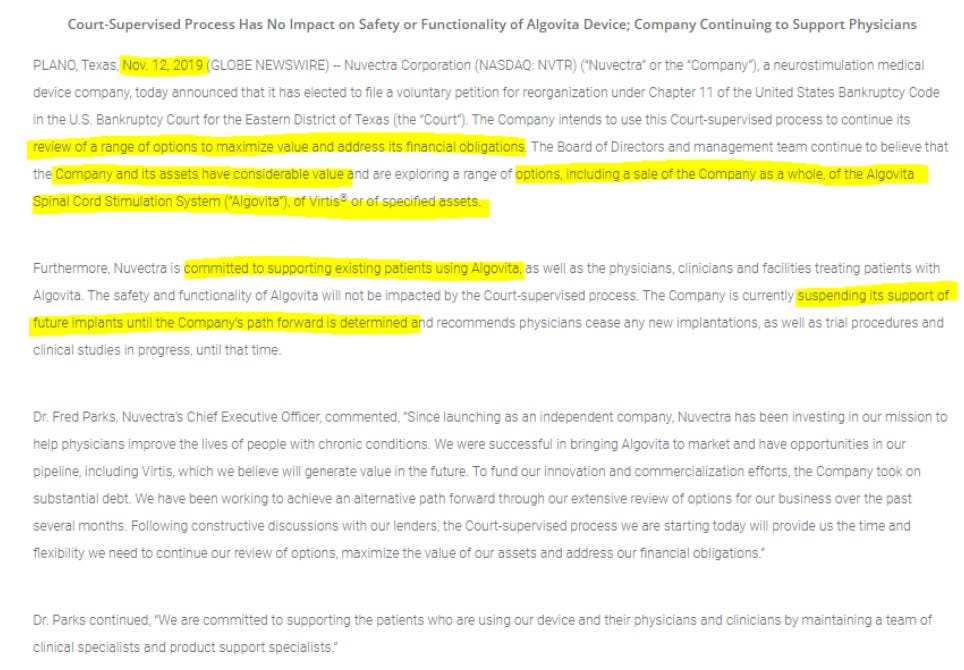

Nuvectra is an interesting case which was brought to my attention via. a net net message board. Specifically it was being talked about before the drop in price on November 12th 2019

Given discussions about it being undervalued before it's 90% fall that day, it peaked my interest as a potential turnaround. To my interest I found out that it fell as a result of the below announcement:

Given that it fell to a price/net tangible asset value of just 0.1x It seemed to be a good candidate for a liquidation type analysis.

Taking it one asset at a time, we can arrive at a fair liquidation value for the company.

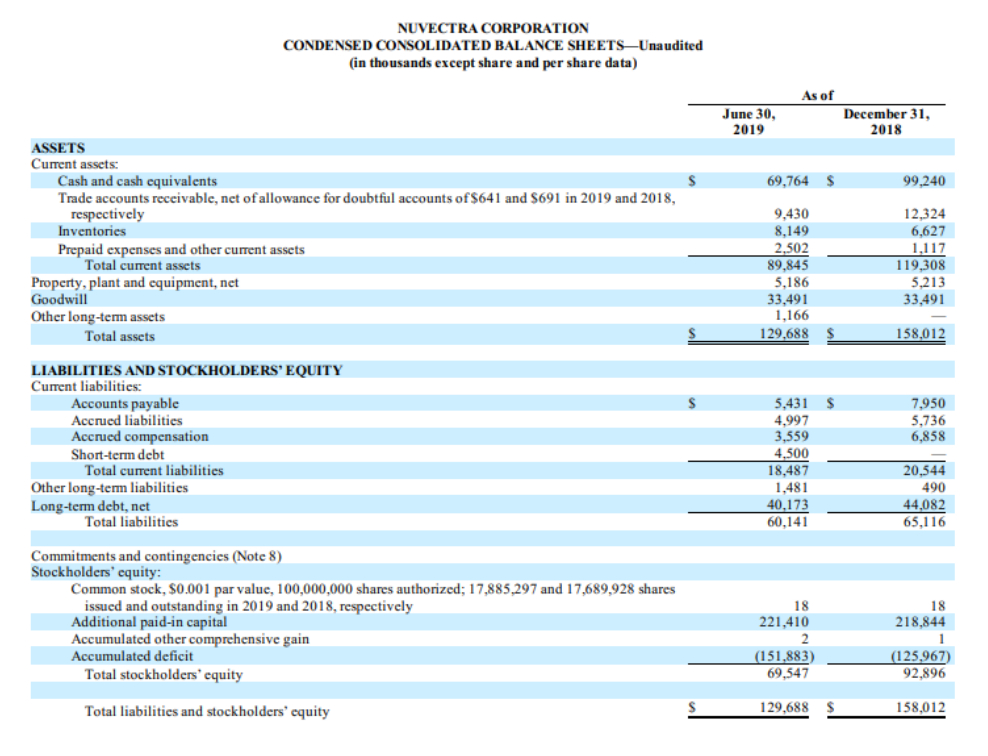

The company points out in the June interim report that their cash balance and sales should generate enough cash flow to fund their needs for the next 12 months. Now take into account their recent announcement to reduce their workforce almost in half and we can probably assume that their will be some cash leftover by the end of the aforementioned 12 month period 30/06/2020. Inventory, receivables and prepaid expenses can be assumed to be soaked up in the sales mentioned above.

Given the mention that the party is subject to various operating lease agreements, it's likely that much of the carrying value of PP&E is leasehold improvements and is hence basically worthless to us, or at least difficult to justify valuing them materially.

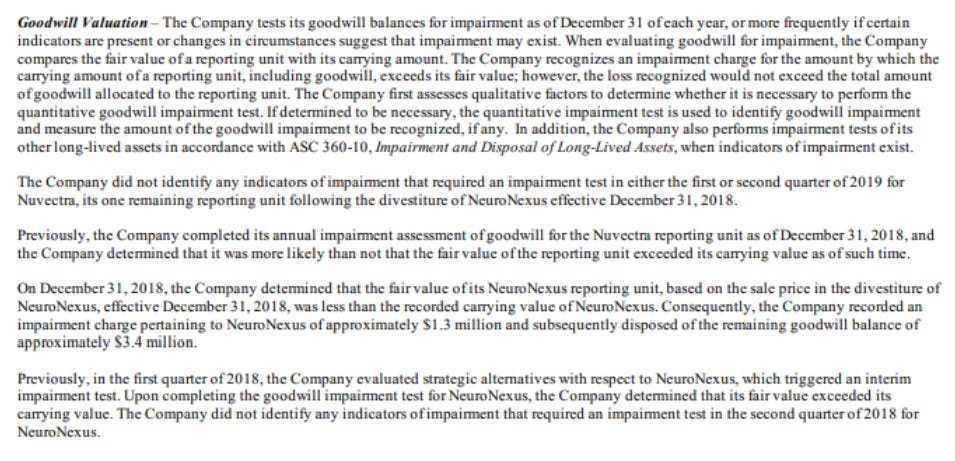

Furthermore their Algovita product has some intangible value as recorded on the balance sheet at 33m. This is tested for impairment at the end of each calendar year.

To provide some valuable context on the conservativeness of valuation, Neuronexus was divested from the company last year. The goodwill carrying value of this asset was $4.7m. Including other assets the value of the sale was $7m in total. Given cash proceeds of $5m, the intangible value recognised was 2.7m.

Given that it accounted for a fraction of Nuvectra's current revenues we could safely assume that the value of Nuvectra vastly outsizes Neuronexus as a result. FY2019 revenues are also projected to be within the range of 57-62m.

So being conservative subscribing $15m to the value of Nuvectra as an asset doesn't seem too farfetched.

Total liabilities can be assumed to have the full value as recorded for conservative valuation.

This leaves us with the following estimated liquidation valuation.

Whether or not this is remotely accurate remains to be seen however there is no doubt great asymmetry here that can make the risk well worth taking.