Onemarket (ASX:OMN) - One Page Stock Pitch

Onemarket (ASX:OMN) - One Page Stock Pitch

Westfield Spin-off Liquidation

Before I continue, the specifics of the company business model and sustainability are irrelevant in this scenario. This is due to the fact that they intend to liquidate the company. Therefore i will not use the usual checklist approach.

About

OneMarket Limited OMN is a retail technology company providing retailers and brands solutions to acquire new customers and strengthen relationships with existing customers

Catalyst

Before continuing, please take the time to read the below announcement.

https://s3-us-west-2.amazonaws.com/secure.notion-static.com/602

Strategy

The idea is to treat this as a net-net trading net cash. So a proper analysis similar to Yowie is due to realise if their is a margin of safety available here. So proper interpretation of the announcement, valuation of their assets and forecasting the potential loss of assets in the interim before distribution.

Announcement Interpretation

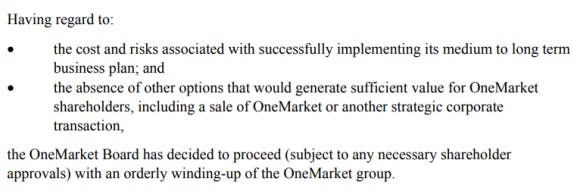

OneMarket has determined that to maximise value for shareholders the distribution of assets is the best way to do so.

Notably they also mention that their is absence of other options to generate sufficient value for shareholders. This could be a bonus however the assumption is the distribution of assets on liquidation is going to happen.

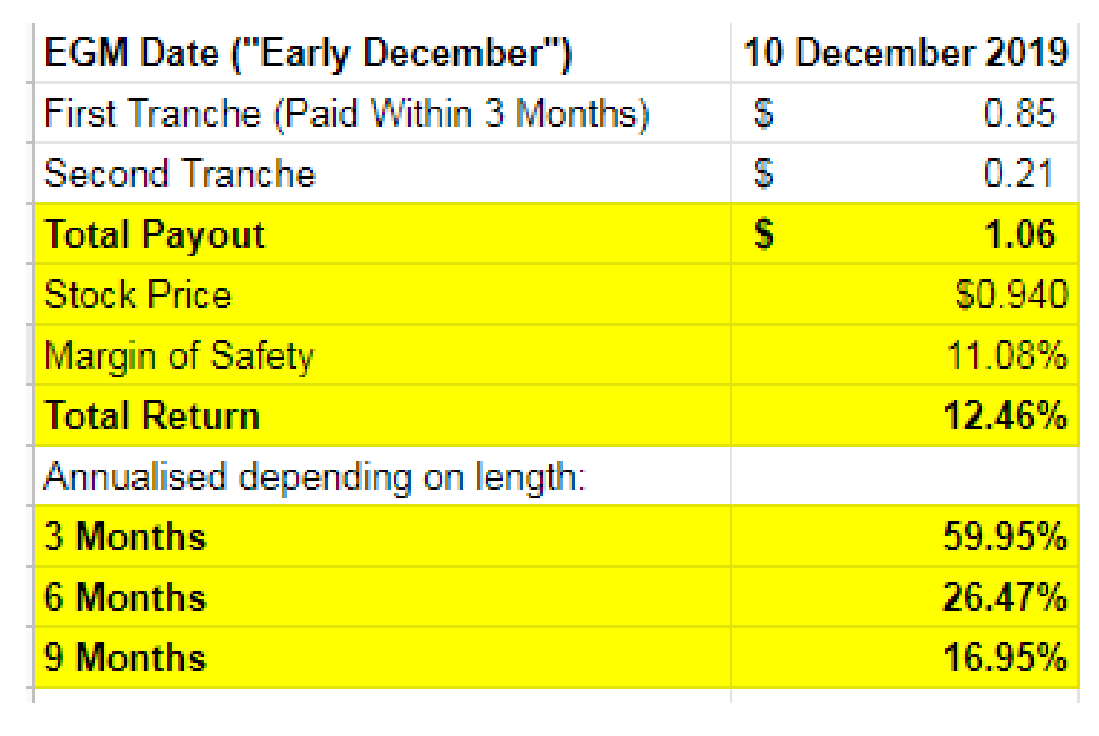

Interestingly, the distribution will be made in 2 portions, presumably the first is excess cash they do not need to pay off creditors with. And the remainder is the buffer they need to complete the wind-up process reliably. So taking this into account, shareholders can expect a bare minimum distribution of $0.85. At the current share price this represents a maximum downside risk of 9.1%.

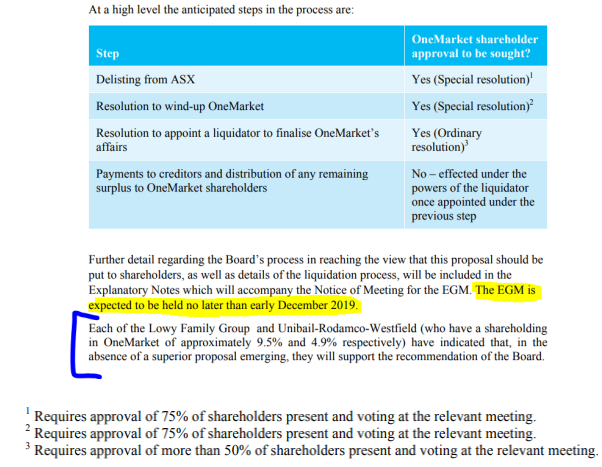

So taking this into account, the deal requires approval by shareholders. Notably the actual liquidator appointment only needs 50% of shareholder vote while the delisting & Wind-up need 75%. With Lowy and Unibail representing 14.4% of interest, a large portion of the vote is already accounted for. The liquidation is likely to occur in other words.

Furthermore, the EGM will be held in early December and release Explanatory notes accompanying.

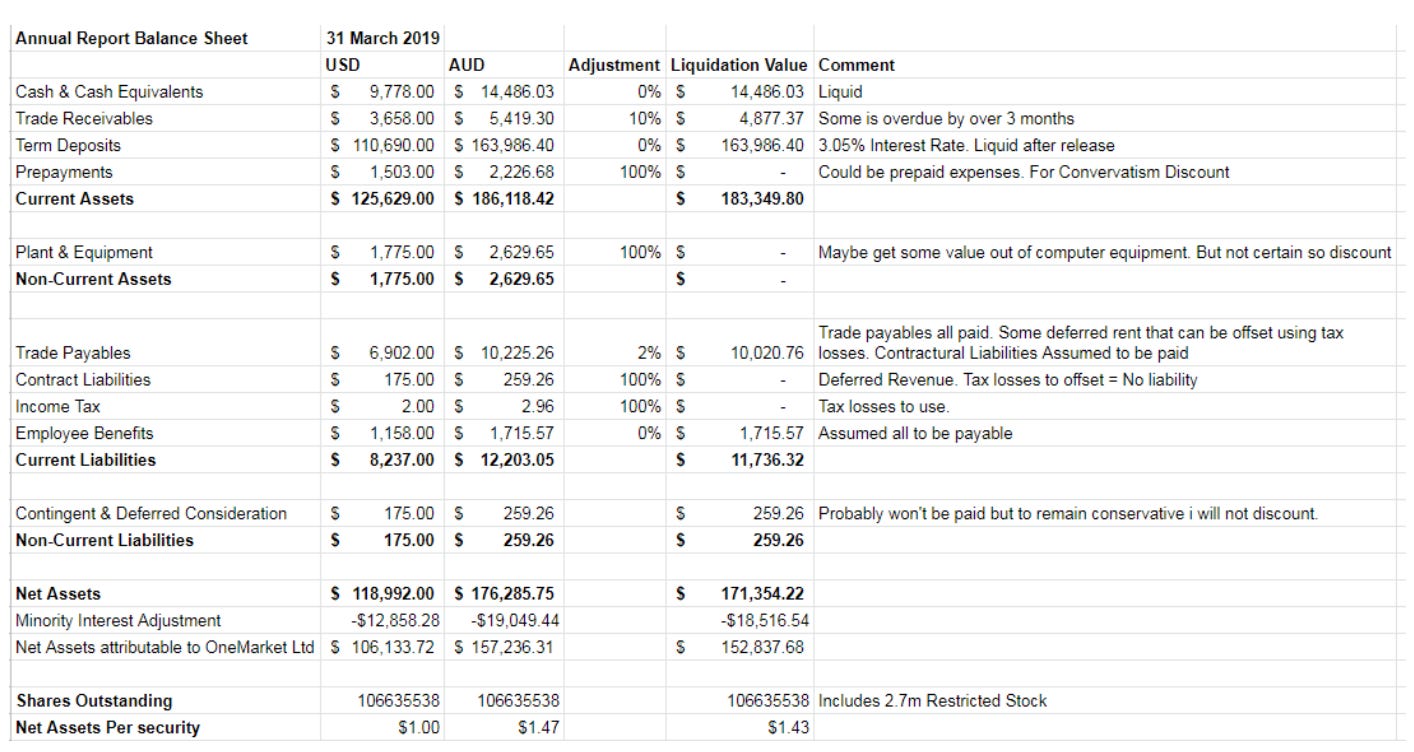

Value of the Assets

As at 31 March 2019:

The last report we received was the EOFY 2019 report. To remain conservative i will interpret a fair value of each asset on the balance sheet and discount/appraise each item appropriately with my accounting knowledge.

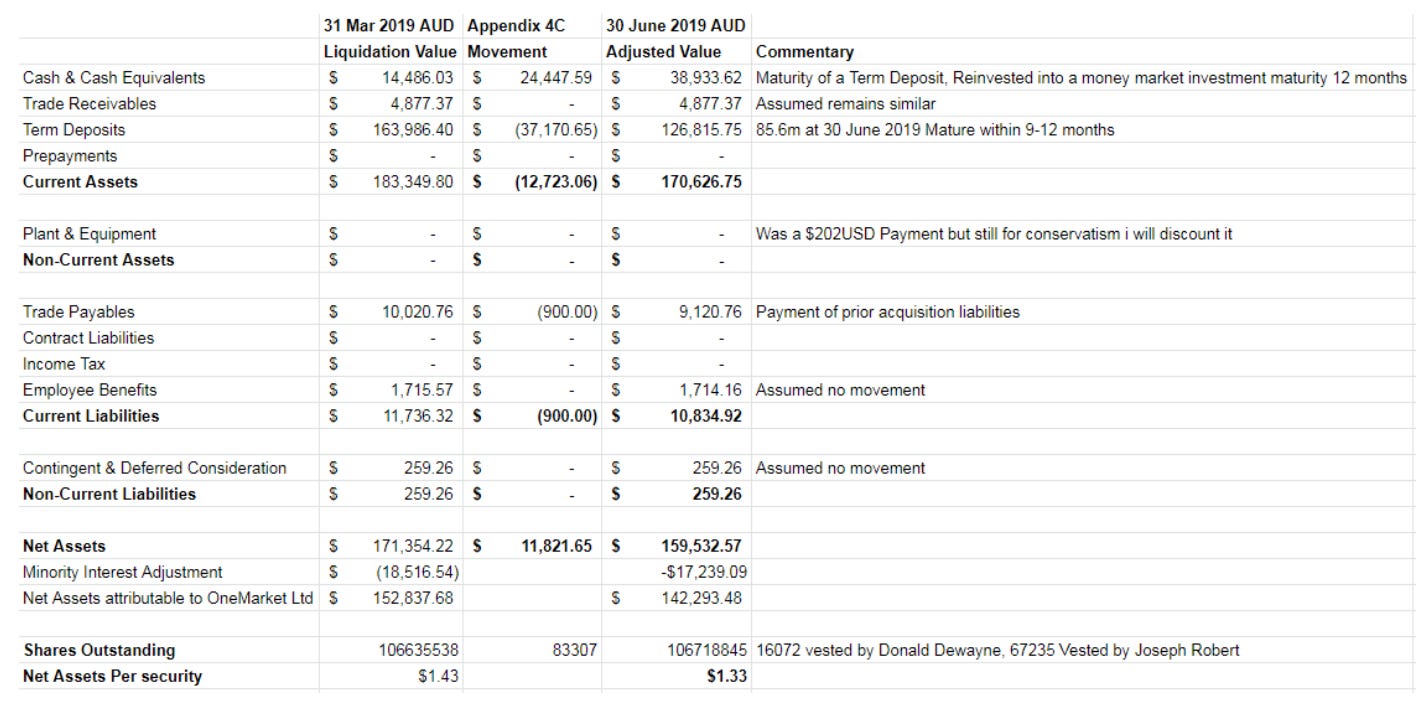

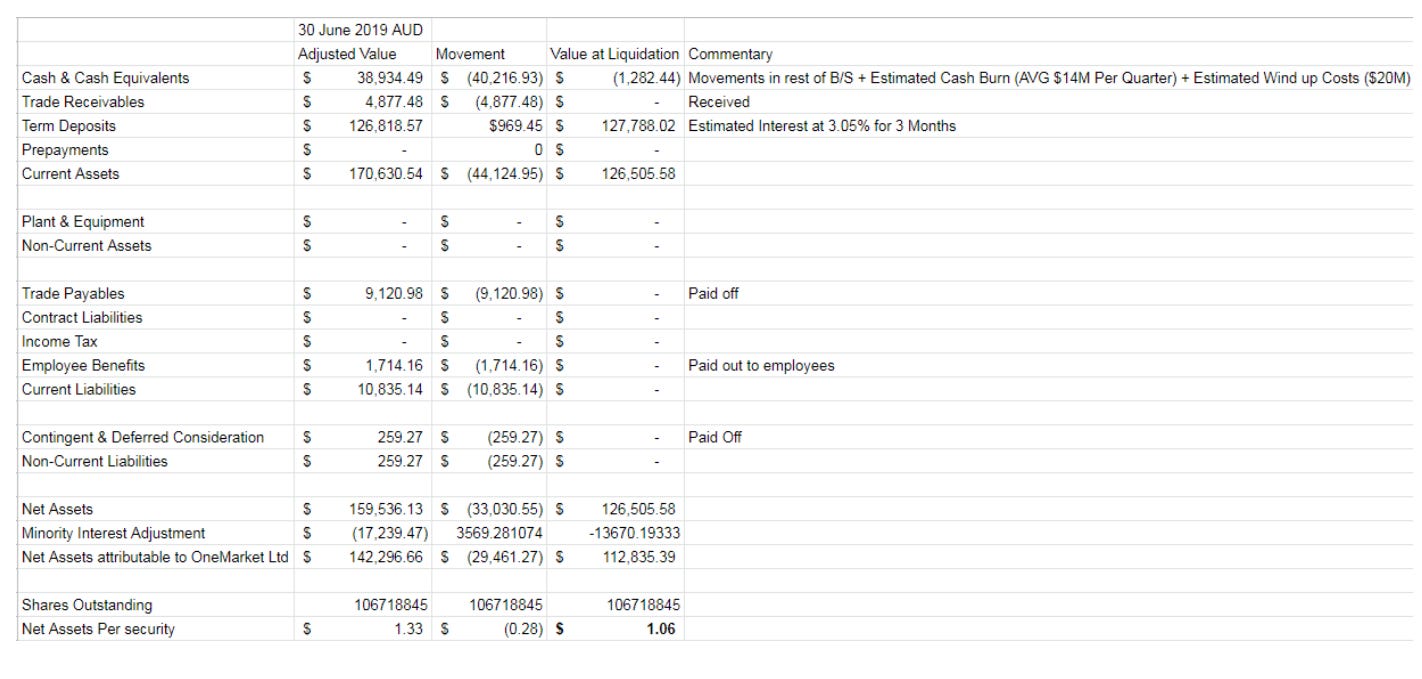

As at 30 June 2019

An adjustment to the first liquidation value is made using the Quarterly Appendix.

Forecasted Value going forward

So using the above calculated Net asset Value I can calculate a potential payout figure using conservative assumptions. I used an average cash flow from the last 5 quarters of cash flow data and made a grossly high assumption on wind-up costs.

Potential Payout

So using the Above calculations and assumptions i estimate the below payout.

Taking the assumptions into account and majority of cash on the balance sheet i am going to assume that liquidation of assets won't take that long. Therefore the annualised return is likely to be higher rather than lower. Furthermore purchase of the stock at a price lower than quoted is possible and could further improve returns. The opportunity represents one with little to no downside and a capped but attractive upside with a margin of safety built in. Further potential is possible if an outsider makes an offer to acquire the assets for more than liquidation value.