Pacific Current Group (ASX:PAC)

Pacific Current Group (ASX:PAC)

November 2023

After our Sky sale, I decided to take a deeper look into Pacific Current, an Australian listed but global asset management business with 16 boutiques across the globe.

This is a merger arb play with what has been a rather long-winded process of competing bids and shareholders with conveniently sized shareholdings which is making it difficult to reach a scheme of arrangement. In July 2023 Pacific received an NBIO from Regal Partners (ASX:RPL), to which a day later GQG Partners (ASX:GQG) responded with intent to make its own offer. Regal then withdrew its offer in September before GQG confirmed a price in early November with the possibility of ‘alternative’ transaction structure given the difficulty in gaining River Capital’s support (Shareholder with PAC ownership of ~20%).

The situation with Pacific has been extensively covered by some impressive investors as detailed below so I would suggest referring to these links below for a thorough overview of the situation:

Acid Investments (Substack)

X / Twitter

Admittedly I am onto this one (very) late as it dipped as low as the low $9’s in October as opposed to the $9.79 price the Hurdle Rate Unit Trust managed to secure. However, with the increased bid from GQG at $11 at the start of November, and the increased prospect of a rebuttal from Regal I don’t think we got off too much worse in terms of entry point.

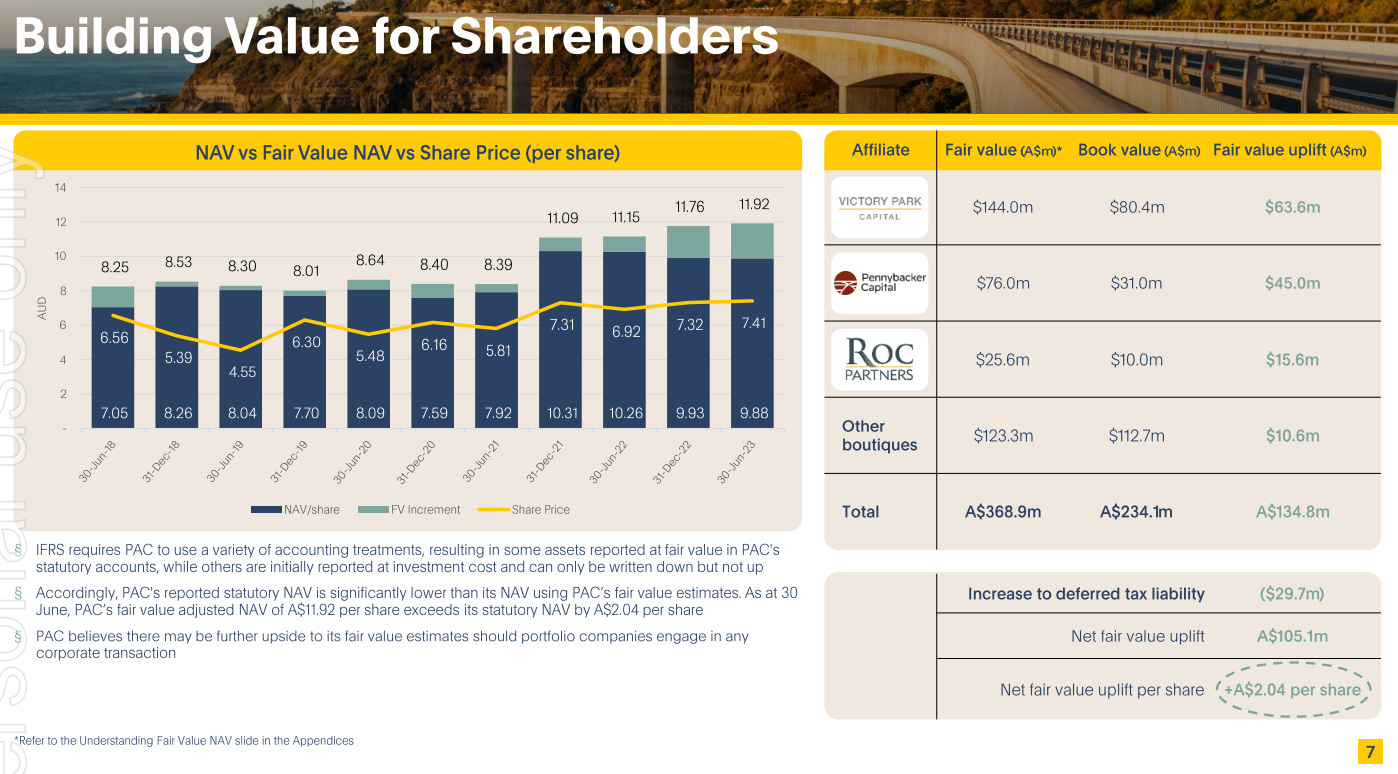

If I could just add a few points of my own, then I would delve into the nuance around the ‘fair-value-adjusted’ NAV bridge from Statutory NAV. As of the 30 June 2023 the Statutory NAV per share was $9.88 whereas the FV NAV was $11.92, a differential of $2.04 per share. This is explained by the company below in their 2023 Annual Report:

“In short, there are some portfolio companies (e.g., Aether Investment Partners, LLC, Pennybacker Capital Management, LLC (“Pennybacker”), Roc Group, and Victory Park Capital Advisors, LLC (“VPC”)) that are recorded on PAC’s balance sheet at initial acquisition cost, with investment balances marked down if impairments are present, but cannot be written up if they appreciate in value. The net impact is that current statutory NAV does not accurately represent the actual NAV that may be realised if PAC were to sell its portfolio.”

In terms of the performance year to date, in the September 2023 update the business benefited from a positive change in the AUD with aggregate FUM growth of 5.3% with the company expecting further strength in the December quarter as well. Interestingly, most of this movement is actually driven by net flows, of which are predominately coming from GQG Partners.

I believe this creates a reasonable backstop for fundamental value and observing the discount over the past 5 years the average discount to NAV has been the share price trading at about 2/3 of ‘fair’ NAV, which today on the 30 June numbers is $7.96. This is the same number that Acid uses for his probability estimation in his recent post. At $9.80 the skew is +$1.20 or -$1.80 so implied odds of 60% (1.80/3), the question is whether this is considered fair or not and do you ascribe any (if at all) value to the potential for a Regal double dip?