Reckon (ASX:RKN)

Reckon is an ASX-listed software holding company that currently operates across two divisions targeting Australian small businesses and accounting firms with its suite of Reckon branded solutions along with Global (particular the US) legal firms with its majority owned Zebraworks business. It currently services over 115k users in Australia and close to 500 legal firms with many of the world’s largest legal firms as clients.

Historically, the group was founded in 1987 by current substantial shareholder Greg Wilkinson and operated for a long time as an Intuit Quickbooks reseller here in Australia before an IPO in 1999 and moving into practice management software in 2004. In 2014 the reseller arrangement ceased, and the group begun to offer their own small business software using that as a foundation, shortly after Reckon Accounts and Reckon One were brought to the market. Prior to this, in 2012 Reckon had purchased the UK based Lidenhouse Software business and begun offering it’s Virtual Cabinet document management solution to it’s Australian customers, subsequently purchasing the similar US based Smartvault business in 2016 before spinning off the two document management business as the now UK-listed Getbusy (LSE:GETB) in 2017. Shortly after this Reckon was approached by MYOB with an offer to purchase its practice management division for $180m which failed to go through, 5 years later Access Group approached Reckon with another offer to purchase this division for $100m which closed for investors. This division was struggling with a cloud-transition and the sale was done at a valuation of 4.6x revenue and 8.4x EBITDA, but with burgeoning cloud development costs was closer to 20-25x NPAT. Lastly, the group acquired a majority stake in US legal outfit Zebraworks in 2020 and increased their stake early this year.

With the backstory out of the way, the group is currently managed by CEO Sam Allert, appointed in the group CEO role in 2018, but has a long history within the Reckon business originally joining in 1999, moving through various senior subsidiary management roles in the interim.

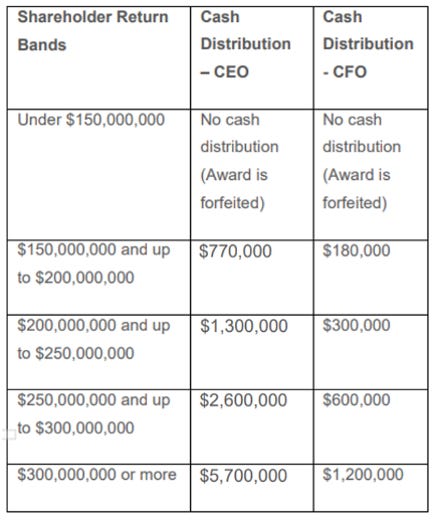

Sam does not own a particularly large stake of the company with 1.3% ownership but has reasonably aggressive ‘Cash distribution incentive plan’ which offers upwards of 1.2x – 9x his base salary dependent on ‘shareholder return’ bands. This plan was only introduced this year and is a replication of a similar plan recently introduced in the Getbusy listing on the LSE as well, given much of the board of directors is shared between the 2 businesses. This plan entitles Sam to receive a cash distribution contingent on the following conditions.

Sam remaining as an employee until the 31 December 2029

Cumulative payments to Reckon shareholders of at least $150m between 24 May 2023 and 31 December 2029 in the form of dividends, distributions, or takeovers, appropriately adjusted for any LTIP expense and capital raised.

Notably, there is also another scheme which was introduced at the time Reckon took an increased stake in the Legal group earlier this year which similarly. Which afford non-controlling interest shareholders of the Legal group to have some of Reckon’s ownership transferred to them in the case of a disposal of USD $200m>$100m>$70m. Disposal proceeds of between USD $70m - $100m will offset dilutionary impacts of the raising earlier this year and amounts between USD $100-200m will allow for a further pro-rata transfer of up to USD $7.5m in shares. For reference, Reckon’s current shareholding is 76% of the business. This plan was introduced due to the underperformance of the legal group since acquiring in 2020 and the capital raised earlier this year should allow for several years of funding.

Financially, the business mix of the 2 divisions and the existence of the incentive plans creates an extremely interesting proposition. First, segment profitability is shown on the right (not including corporate costs). The group generates a NPBT of $5.2m after corporate costs, a margin of just above 10%, although is the result of a highly profitable business group mixed with a highly unprofitable legal group. In the event the legal group is excluded, pre-corporate cost NPBT margins would elevate from 16% to 30%, which if you assume consistent corporate costs as a % of revenue and a 25% corporate tax rate, would equate to an NPAT margin of 18% as opposed to the current margin of 7.6%, more than double the current.

Not to mention that the Business Group is currently facing a masking of its double-digit cloud growth via. the flat or declining desktop-based revenue and perpetual licensing. This is made even further appealing knowing that the business group’s ARPU is significantly below any peers in the Australian market with the average cloud user paying just ~$16 per month as opposed to the average Xero user paying more than double at $34 per month. As a result, it would not be unfair to assume Reckon has some degree of untapped pricing power in their client base.

Knowing this, Reckon, at our cost basis of $0.53 trades at an enterprise value of $63m and generated a normalised NPAT of $4m in the FY2022 year, which by itself does not sound particularly appealing as a multiple of 15.6x. But, with optionality surrounding the incentive plans and the underlying profitability of the Business Group approximating a PE of 8.6x with untapped pricing power, there is many ways to throw shareholders a bone in terms of capital appreciation. It should also be noted that the group maintains a 60% fully franked dividend, equating to a 6% dividend yield on our cost basis at the current level of earnings. Hurdle Rate Unit Trust is an excited shareholder of Reckon for the reasons stated above.