Sequoia Financial Group (ASX:SEQ)

Sequoia Financial Group (ASX:SEQ)

May 2023

Sequoia Financial Group is a professional services business providing a variety of services to accountants and financial advisers across Australia. These service lines include acting as an AFSL licensee, provision of legal documents, SMSF administration, insurance broking, financial media and wholesale investment opportunities. The business has drastically changed over time, particularly with the reverse takeover of Sequoia Financial Group in 2015 and the acquisitions of InterPrac & Morrison Securities in 2017.

Today the group is spearheaded by Executive Chairman Garry Crole (59 years old), who came onto the board in the 2017 financial year and into the executive team during the following year. Garry has an extensive career, but perhaps most notably were the 2 businesses he founded in Money Planners in 1988 before having it conjoin with ASX-listed Deakin Financial Services where Garry was CEO from 1990 to 2000 before founding InterPrac in 2003. All these businesses relate heavily to what Sequoia looks like today. Other notable appointments include CFO Lizzie Tan and the various heads of each division such as William Slack (Head of Equity Markets), Alex Fabbri (Head of Corporate Finance), Brent Jones (Head of Professional Services), Raika Afzali (Head of SMSF). Just announced as well were 3 senior appointments in Martin Morris as COO, Justin Harding as Head of Legal and Risk and Mark Hutchinson as Senior compliance manager. Directors alone own 11.4% of the shares, with significantly more owned by subsidiary heads which many of which are past acquisition vendors.

Sequoia is a difficult business to explain financially as there is a long list of different billing models throughout their various subsidiaries. When looking at the financial statements, unlike other more focused businesses, additional revenue is more likely to be either highly dilutive or highly accretive to margins in this case, depending on the business mix within the group. Margins for each division are shown to the left in addition to the growth for the FY2022 income year.

Below the EBITDA line, we have genuine depreciation and lease expenses of $1.4m along with acquired intangible amortisation of $2.1m before a tax expense of $3m. Given customer list intangibles are like amortising goodwill, it would not be unfair to look at this business based on NPATA, for which we have $7.1m for the 2022 year. During the 1H of 2023, the group saw significantly contracted profitability, which I will touch on further below, but for the time being, we should now get the general idea of the income statement.

The majority of the Sequoia’s subsidiaries benefit from a point-in-time revenue recognition barring Sequoia’s specialist investments division which markets structured products where it offers leveraged instruments known as ‘deferred purchase agreements’ to SMSF’s (which are otherwise not allowed to take on margin debt). These instruments demand all interest to be paid upfront along with an application fee, and often this results in multiple years of interest received upfront. The group’s negative tangible invested capital after subtracting net cash is a testament to its negative cash conversion profile.

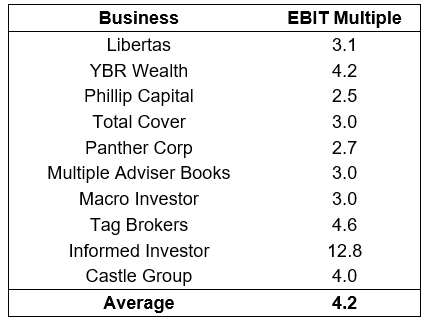

Capital allocation has shown to be reasonable since Garry was adorned as executive chair in 2018 with an average EBIT multiple paid of 4.2x over the past 5 years. With a tax rate of 30% this would be equivalent to an upfront PE of 5.9x and earnings yield of 16%. With a cumulative investment of $18.2m the group has acquired EBIT of $4.3m, 2018 operating profit was $4.3m and 2022 was $12.4m, meaning that the group generated organic EBIT of $3.8m. This equates to an organic CAGR of 14% + Inorganic CAGR of 16% for a total of 30% between 2018 and 2022. However, during this time, the share count has also compounded at 7% predominately due to acquisitions, as a result the real Inorganic CAGR is closer to 9%. This is also ignoring the movement in their net cash position from $11.6m to $14.9m. Over this period 20% of the cumulative NPATA was paid out as dividends, as a result returns on incremental capital are approximately 25%. If you consider that all incremental capital was used for acquisitions (given the negative working capital cycle), inorganic returns on capital are just 11%, leading me to believe that perhaps an aggressive dividend policy along with a special dividend of the existing cash on hand is the best possible course of action.

The Sequoia business has had a very interesting FY2023 year, with sharply declining profitability juxtaposed with a highly successful divesture of Morrison Securities. With the share price down just 8% it’s clear the market is slightly outweighing Sequoia’s current year profit decline as opposed to the receipt of some 60% of its market cap in cash proceeds, in other words the market thinks that Sequoia has lost >60% of it’s earnings power in a year, a sentiment that to me sounds absurd given it’s growing adviser network and largely unchanged headcount over the past 12 months. It is unlikely to see advice remediation costs every year with the current standards of adviser education requirements. Sequoia is not without risks with the primary risk in my view being the misallocation of their newfound cash proceeds, but also elevated and recurring client remediation, any future mishaps with ASIC regarding financial services or products, adviser attrition, vendor attrition and so on.

With the run-rate of the media business, and the acquisition of both Euree and Castle group, lost earnings of Morrissons have been replaced with just 1/10 of the sale proceeds. Should Sequoia generate similar NPATA in FY2024 as it did in FY2022, the group will be trading at an enterprise value of ~4x NPATA. Given their intentions to move to a payout ratio of >70% and abundance of franking credits, the opportunity screams mispriced even without any growth. This is all ignoring the previously announced 7-year business plan with targets of $30m in EBITDA by FY2026, 2.5x what it was in 2022, representing a 25% CAGR. Given their track record of acquiring, they should be able to acquire $10-12m of EBITDA with their cash balance alone, leaving another $6-8m to be sourced from any incremental retained earnings and organic growth.