Straker Translations (ASX:STG) - Deep Dive

Straker Translations (ASX:STG) - Deep Dive

Translation Service Provider - Growth at all costs

Overview

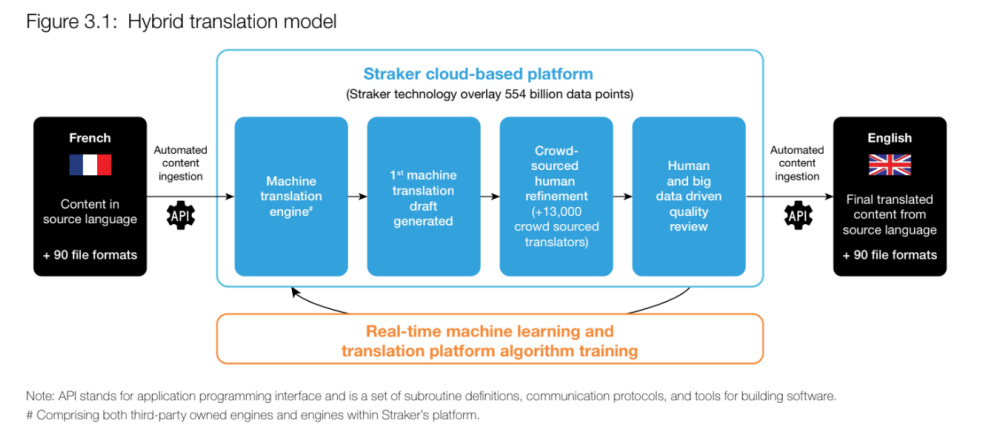

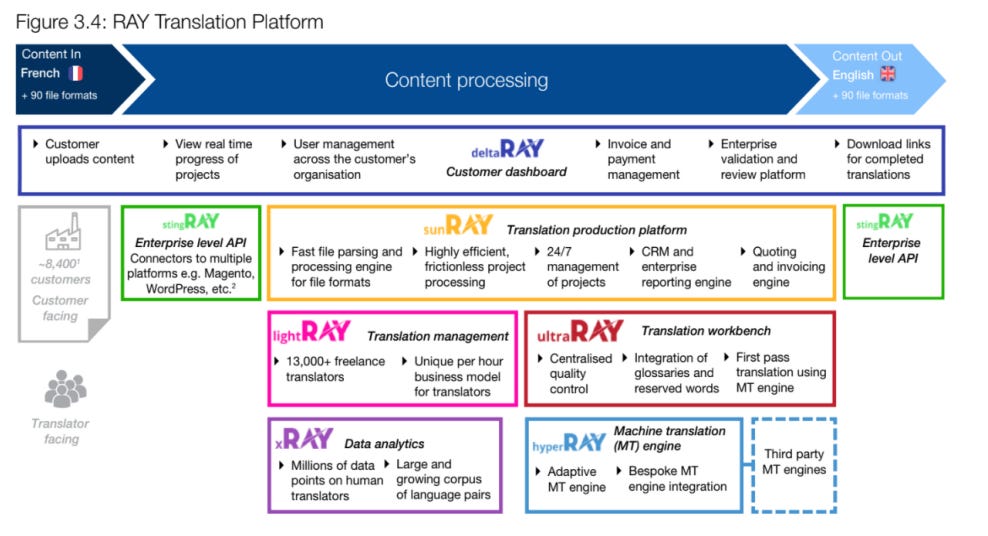

Straker has developed a hybrid translation platform that utilises a combination of Ai, machine-learning and a crowd-sourced pool of freelance translators. This is a beck and call relationship whereas a customer uses the ‘RAY AI’ platform to request a translation quote and once confirmed a draft translation is created of which the freelance translators improve upon before finalising the job. It’s a very easy business to understand at a high level and you can imagine the tailwinds from the effects of globalisation.

The company was founded in 1999 by current CEO Grant Straker plus his wife and current COO Meryn Straker. The first 10 years of operation were in Multilingual content management, which is just a fancy term for having a website that can be viewed in multiple languages. The evolution occurred in 2010 when the business commenced the development of their translation services platform which now goes by the name ‘RAY AI’.

This proprietary technology is owned by Straker is a single cloud-based translation platform that utilises 7 modules:

Delta Ray - Free customer dashboard that allows customers to order and track translations, get reports, make payments. It also has a memory bank that provides a way to customise future translations with reserved terms.

sunRAY - This is a project management platform used by straker to control translation projects, automate quotes using data from the xRAY (Data analytics) and lightRAY (Translator management) modules. These automated quotes are based on historical data points, subject field and translator availability.

stingRAY - API connection to third-party platforms such as Wordpress and Magento.

lightRAY - Translator management portal, tracks translators which allows them to have a profile of skills and pick the right translator for specific jobs.

ultraRAY - The translator workbench. This is where the bulk of the work occurs. Specifically of note is that this is accessible on a browser even though it is used with large files such as media subtitling etc.

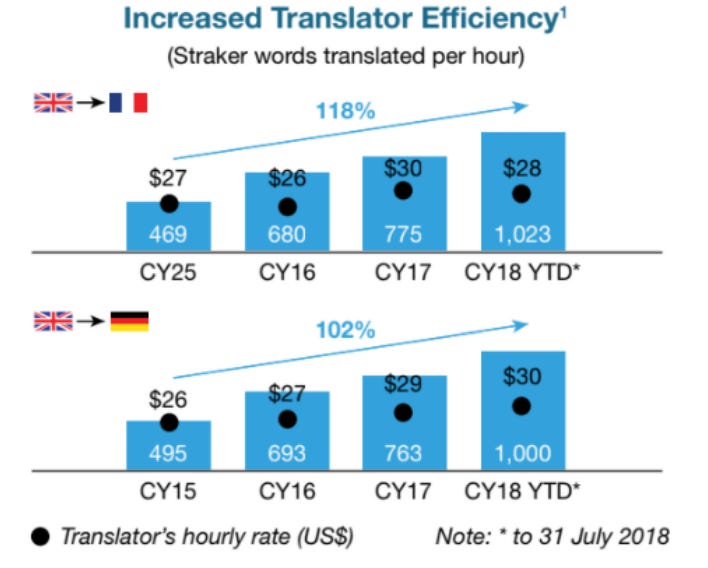

The group states that the platform’s machine learning will assist in growing the efficiency of the translation process, skewing the workload towards the system. Regarding price flexibility, this specifically is due to the revenue model. Clients are charged on a per word translated basis whilst translators are paid by the hour.There certainly is evidence that this trend is in the right direction as the cost of translators has remained relatively stable whilst the speed of translation in the 2 below pairs doubled or more over the period 2015-2018.

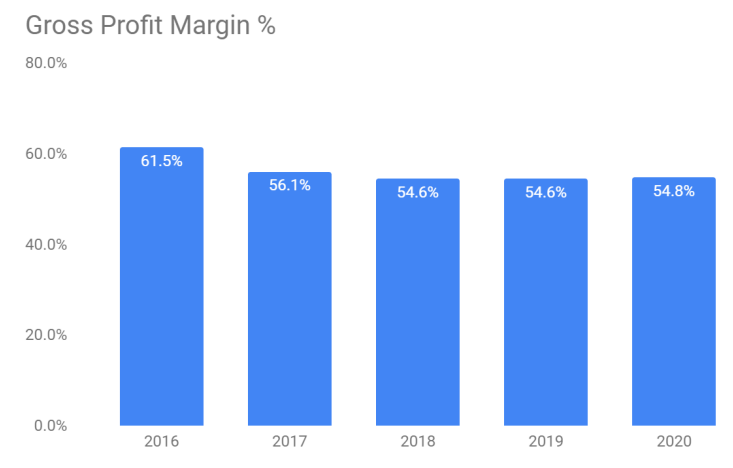

Naturally you would expect this to be reflected in a dramatic improvement in gross margin, however, that has not been the case as can be seen below. The reason for this is simple, the group has higher than industry margins and their acquisition strategy involves the integration of lower-margin subsidiaries. At the start of an acquisition, revenues are off the RAY AI platform and are lower margin as a result until onboarded. I do note that ~90% of revenue was on platform in FY20 and the platform margin is 56%.

Industry

Traditionally, the industry has relied on the largely manual efforts of individual interpreters and translators. However, the use of technology platforms that can make delivery of language services more productive is increasingly disrupting the industry. Technology platforms are becoming more widely used in the provision of language services for written content, but currently are rarely accurate enough to provide an acceptable business quality translation. Technology is therefore mainly deployed in conjunction with manual translation services (a hybrid solution) and can improve the productivity and efficiency of manual translation. However, a significant portion of translation services are still delivered on a completely manual basis

The global market for language services is estimated to be ~US$50B as of 2018 and projected to grow at a rate of 9% CAGR between then and 2022. Of this market, the translation segment makes up roughly ⅔. Furthermore, the strong economic growth in emerging markets with specific language requirements provides an opportunity to move into providing translations for rare languages that Straker has identified as higher price/word projects for them.

Furthermore, internet traffic is rapidly inflating alongside globalisation which is driving cross-border trade in eCommerce. As online content is increasingly consumed cross-border, there is a growing demand for localisation of sales and marketing content. The industry is highly fragmented, with the top 100 Language service providers estimated to account for ~15% of global revenue, with a total estimated number of providers of over 18,500. Given the relatively low competitive rivalry and high proportion of manual translators, this provides an excellent backdrop for a high margin participant like Straker to acquire and integrate in.

Capital Allocation & Growth

Finally, I will cover the basis of acquisition. The rationale and fundamentals behind the strategy according to Straker includes:

Increasing the earnings margins achieved by acquired companies through migrating their customers to Straker’s technology platform and business model;

Consolidating operating costs through utilising Straker’s centralised global technology and the support infrastructure;

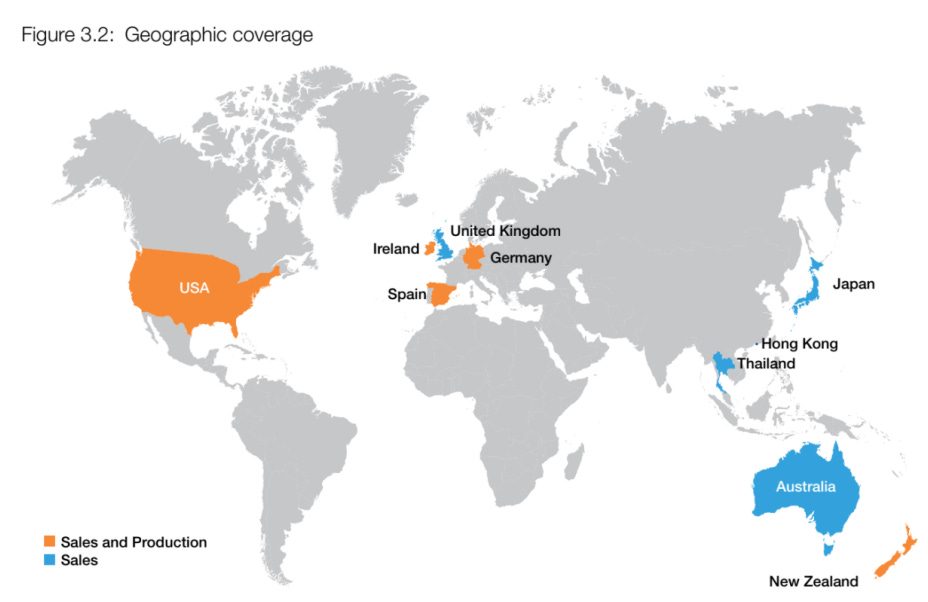

Gaining a geographical footprint in key markets with many customers still requiring local presence;

Gaining economies of scale in areas of importance such as data assets across language pairs, translator resources for domain subjects, key sales people and processes and global production capacity; and

Growing acquired customer bases through offering Straker’s technology solutions.

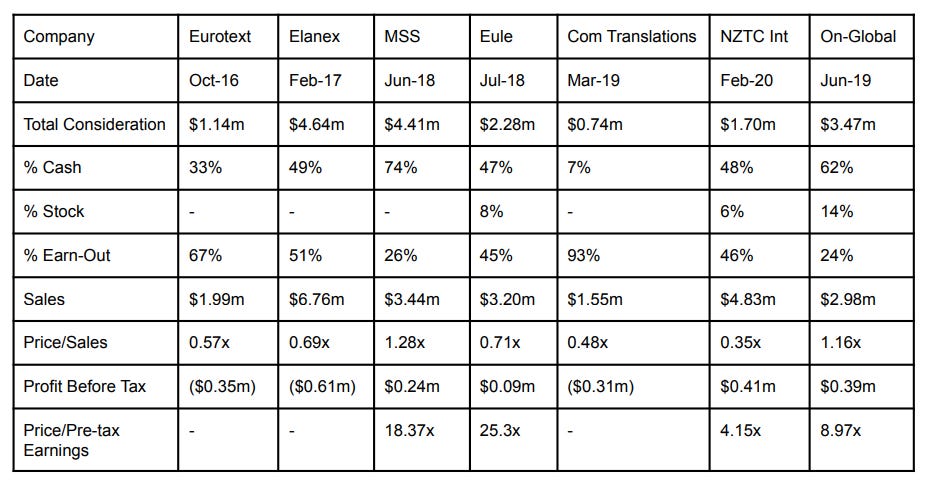

There have been 6 acquisitions undertaken by the group, below is a summary of the key information for each.

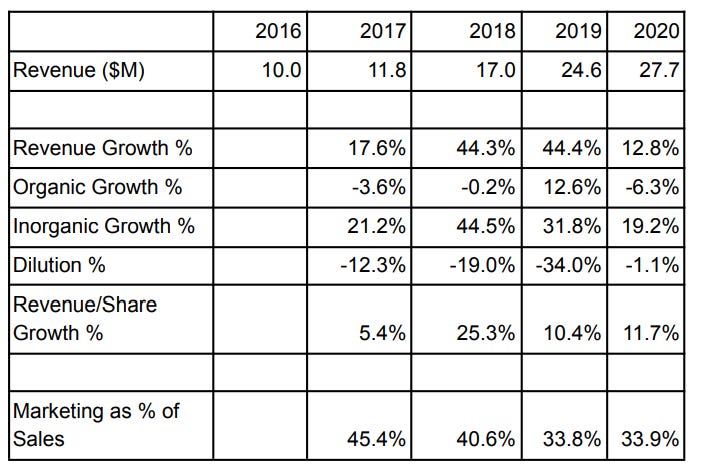

Growth isn’t complete without organic growth, in which case the company's strategy is to spend almost half of the group’s revenue on aggressive marketing strategies. Specifically there is a focus on enterprise level sales. These sales are more recurring and of higher value. I’m much more skeptical about the sustainability of these sales but for further context I will show the split in revenue growth organically and acquired.

There is a noticeably low level of organic growth, despite the company investing heavily in marketing to drive enterprise level sales. They don’t talk much about the results of marketing, however they love to selectively choose data that looks good. Such as the revenue growth, not on a per share basis but just revenue.

Management

Whilst this business does have co-founders, they only own some 13.8% of the shares outstanding, or roughly $7.5m. This contrasts with Grant’s wage of $365,000 and an undisclosed amount of $1.24m to other Key management personnel which includes the COO and co-founder Meryn. Assuming this is split equally among the members of the team that would mean Meryn takes home roughly $250m in wages as well putting the ratio of founder ownership to annual wages at some 12:1 which is an adequate but not incredible premium. Putting wages aside, the management incentivises key management personnel with options, another lacking policy with these having 3 year vesting periods.

So you can tell whilst management do have a decent amount of skin in the game, there are some weak incentives to think long term for the majority of staff. This leads to the lack of per share emphasis for example or maximising the share price during the vesting period. Another point of note is that the Co-founders have 3.6m shares in escrow until the release of the Half yearly 2021 results, a key date to monitor as given the seemingly low lack of incentive, it’s possible they could reduce their holding. It’s in my general opinion that this lack of corporate responsibility is why the business dilutes the way it does

Further fuel to the flames is that there is a noticeable history of overpromising to shareholders apparent. A few examples are highlighted below:

“As I have publicly stated we believe that we can achieve $100m+ valuation and we have been given no reasons as to why this shouldn’t be the case from our recent engagement with potential investors and with comparative IPO and company sale valuations.”

~ Grant Straker 2017 Annual Report

The actual IPO managed a market capitalisation of AU$79.4m market cap, slightly over 20% less than eluded to by Grant the year prior to the public offering.

“The Group’s forecast cash flows indicate they will be in a position to pay their debts as they fall due in the foreseeable future being a period of twelve months from the date of signing the financial statements. The key assumptions to the forecast are that the Group will achieve a breakeven operating cash flow for the year ended 31 March 2019 based on sales growth across all subsidiaries and from synergies arising from the integration of the Eurotext and Elanex acquisitions.”

~ 2018 Annual Report Note 25: Going Concern

Whilst this only a forecast, i would expect them to get relatively close to operating cash flows, however, this is not that case as they again over promised with a result of a ($1.07m) in operating cash flow, even with a reduction in working capital of $0.75m.

Time and time again the management loves to give a rosy outlook attached with overwhelmingly one-sided positive material rather than talk about their problems and how they will address them in the future.

This business I was initially significantly interested in due to the success of the acquisitions, an owner-operator, industry with several other strong multi-baggers and an undemanding relative valuation. However, after taking ample time to research this business, i’ve uncovered low/no return marketing expenditure at a high % of sales, shareholder funded acquisitive growth and an overly optimistic management with short-term incentives causing them to dilute needlessly. I leave you with this below meme to summarise my thoughts on Straker Translations.