The Character Group (LON:CCT) - Deep Dive

The Character Group (LON:CCT) - Deep Dive

UK Toy Manufacturer

About

The Character Group plc is the largest independent toy company based in the United Kingdom. We design and manufacture toys and games, many produced under licence and based on popular television, film and digital characters and distribute all of these products in the UK and in many territories overseas. We also partner on an exclusive basis with other overseas based toy producers to market and distribute their products in the UK.

Our diverse product ranges focus on a number of key areas within the toy sector; these include Pre-school (where we consider ourselves as market leader), Boys, Activity and Girls.

Our corporate strategy is to continue working with our core brands, where we continually look to add new and relevant products; and to develop innovative products for newly acquired brands; this we believe has enabled, and will continue to enable, the Group to increase market share in the UK and overseas. Since the year end, we have acquired a 55% shareholding in OVG PROXY A/S, a toy distributor in Denmark.

We do not own factories, our manufacturing takes place predominantly in China and is carried out on a closely managed and collaborative, sub-contract basis with reputable suppliers. The Group owns and operates from three freehold properties in the UK. Our head office is based in New Malden, Surrey and our two distribution warehouses are located near Oldham, Greater Manchester. Our Far East operations are carried out from leased offices in Hong Kong and Shenzen, China. Our customer list includes the major UK Toy Retailers, UK Independent toy stores and a wide selection of overseas distributors.

Stakeholder Relations

I would expect that being a third-party toy distributer, relationship with their suppliers Brand licenses) is key to their ongoing operations. To this avail risk can be reduced by preventing an overreliance on any one particular license. Character Group discusses the management of their portfolio in the below quote:

"We work in a dynamic market place and our business model is designed and has evolved to have the necessary agility to operate efficiently in adapting to the demands of change. We work tirelessly to anticipate and then deliver what our customers seek in terms of product, quality and price point. Our current portfolio is derived from our own-developed, inhouse ranges, including those that we produce ‘under licence’, and those of third-party manufacturers, which we distribute in our territories on an exclusive basis. Our close partnerships and ongoing dialogue with our suppliers and customers give us invaluable feedback that enables us to develop and adjust our plans to optimise our sales penetration. This informed and responsive approach to understanding and working within our market gives us a strong platform across which we are able to promote and sell a broad portfolio of relevant, in-demand products. Our blend of long-term customers and suppliers and more recent entrants to the retail market, sees our business well balanced and diversified in both its customers and suppliers, thereby marginalising any potential concentration risk."

So with this in mind, a diversified portfolio of brands and proactive approach to stakeholder management has allowed them to prosper. This is very interesting and is worthwhile exploring this portfolio further, starting with the importance of 'evergreen branding'.

Brand Strength

A large contribution to Character Group's success has been their branding, that is to create a transcendent brand, an “evergreen,” the name should align with attributes or values that never go out of style.

A particularly strong contributor to Character Group's portfolio is 'Peppa Pig', a 15 year running brand that grows well for the group, both domestically and internationally. The group states:

"This brand is a striking example of how our business model is applied to understand what the market and consumer wants from a product range and to develop it over many years, keeping it fresh, innovative, fun and educational."

Hasbro Inc Acquisition of Entertainment One

Speaking of Peppa pig, the relationship with Entertainment One remains intact for the time being despite being taken over by Hasbro. In the most recent update Character Group states:

"Following the announcement in August this year of the proposed takeover of Entertainment One Limited ("E1") by Hasbro, Inc., it was gratifying to note that our current Peppa Pig licence was extended until 30 June 2021. Additionally, we are delighted to announce that yesterday we signed an additional, new licence with E1 to produce a range of wooden Peppa Pig toys and products. This new multiterritory licence deal (which includes Europe and Australia) will run through to December 2022. The initial reaction to the concepts, product ideas and designs for this wooden range from our customers has been extremely positive. The line, likely to be launched in July 2020, seems to be assured of good retail support, given its strong sustainable, recyclable and environmentally friendly credentials."

Being a business reliant on the use of this intellectual capital, relationship with the suppliers of the brand names is key. Seeing as Entertainment One has been a long-running partner to Character Group it's reassuring to see this remain intact.

Proxy

Another important event is the acquisition of Proxy, a Danish toy distributor. Particularly interesting is that they have the exclusive rights to the distribution of Fortnite Figurines. Given the explosion in popularity, albeit somewhat mature, that relationship is still valuable in my eyes. FUNKO is another valuable asset to the group. Given they paid an initial $300k Sterling with a further $3m in performance consideration, it seems very cheap to get access to high profile branding as highlighted below.

Retailers

So how about the consumers. Where does Character sell their manufactured toys? Well simply put, toy retailers. Another recent event of which has been the decline in Scandanavian toy retailing, largely due to the failure of Top Toy (formerly the largest toy retailer in that market). You may well recognise their stores as the common "Toys 'R Us" brand. I should stress that this is only a decline in this particular Nordic region, the Toys 'R Us stores in other regions are owned by separate companies. Nonetheless it is a concerning development as a result with a clear reduction in the demand for toys by toy retailers, leading to an impact in results for Character Group.

In saying this, Character has also experienced a decline in the UK Toy market. As the purchase of toys and games is non-essential, industry demand is particularly sensitive to changes in real disposable income. Weak growth or declines in disposable income constrain the level of discretionary spending undertaken by consumers at the retail level, which results in reduced orders and lower production volumes. Real disposable income is expected to be adversely affected by rising inflationary pressures as the process of leaving the European Union continues. This is anticipated to limit improvements in domestic demand. In saying this, the stock has tend to reflect this sentiment with a re-rate and contraction of the multiple in the short term.

Management

The Board of Directors of the Group consists of:

Jonathan Diver (aged 54, Joint Managing Director

Jon Diver joined the business in September 1991 from Rainbow Toys Limited, where he was Senior Marketing Executive. He became Group Marketing Director in August 1994 and has developed close working relationships with the Group’s suppliers, including Licensors and Manufacturers. He has played a key role in determining and delivering the group’s diversified product development strategy. Jon is a past chairman of the British Toy & Hobby Association. Jon is jointly responsibility with Mr Shah for the setting and implementation of the Group’s corporate and competitive strategy and managing its commercial affairs.

Kiran Shah (aged 64, Joint Managing Director, Group Finance Director and Company Secretary

Kiran Shah is a member of the Association of Chartered Certified Accountants. After initially working in a private accountancy practice, he moved into industry and, since 1978, has been involved extensively in the toy industry, notably in his role in jointly heading up a successful management buyout of Merit Toys Limited in 1981 and its subsequent sale to Bluebird Toys plc in 1988. He jointly established the original business of The Character Group plc with Mr King and Mr Kissane in April 1991. Kiran is jointly responsible with Mr Diver for the setting and implementation of the group’s corporate and competitive strategy and managing its commercial affairs and is responsible for the Group’s financial management, accounting, tax and legal affairs.

Joseph Kissane (aged 66, Managing Director of Character Options Limited

Joe Kissane has considerable sales expertise both at retail and supplier base in and outside the toy industry, gained over a period of over 40 years, notably with such companies as Nabisco, Lego and Tonka. He is one of the founders of the Group and is a senior committee member, charity secretary, trustee and past chairman of the Toy Industry’s leading children’s charity The Fence Club. Joe has direct responsibility for the sales and operational management of the Group’s principal UK trading subsidiary Character Options Limited, including overseeing relations with customers.

Michael Hyde (aged 44, Managing Director of Far East Operations

Mike Hyde joined the Company in 2005 and was appointed to the Main Board in 2011. Prior to joining Character, Mike spent a number of years working for Mattel Inc., the NASDAQ listed US toy designer and manufacturer, where he held a number of management positions, focusing on brand management, marketing and product development. He holds a Bachelor of Arts BA degree in Mandarin Chinese and a Master of Business Administration MBA degree. Mike has direct responsibility for the operational management of the Group’s Far East operations, including overseeing relations with factory suppliers.

Jeremiah Healy (aged 57, Group Marketing Director

Jerry Healy joined Character Options Limited (the Group’s principal trading subsidiary) in 2004 as Head of Marketing; he was promoted to Marketing Director in 2006 and then became Group Marketing Director in February 2016. He has a wealth of marketing experience gained within the toy industry; prior to joining the Group he worked with Hornby Hobbies, Matchbox and Mattel, both in the UK and Europe and also at Sony Computer Entertainment Europe. Jerry holds a Bachelor of Arts BA degree in Business Studies. Jerry is responsible for setting and managing the Group’s product and customer focused marketing plans.

Richard King (aged 73, Non-Executive Chairman

Richard King has extensive experience in the toy industry and has been involved in importing consumer products from the Far East since 1969. He established the original business of The Character Group plc jointly with Mr Kissane and Mr Shah in 1991 and was until February 2016 the Group’s Executive Chairman. Richard is responsible for ensuring the quality and sound approach to high standards of corporate governance and the effectiveness of the Board as a working group. He is Chairman of the Corporate Governance and Risk Management Committee and of the Nominations Committee and a member of the Audit and Remuneration Committees.

David Harris (aged 68, Senior Independent Non-Executive Director

David Harris was appointed to the Board in 2004; he has very broad financial experience gained over a 40 year career in both executive and non-executive capacities. He is currently a non-executive director of Manchester and London Investment Trust plc and F&C Managed Portfolio Trust plc, both of which are quoted companies on the London Stock Exchange. He is also a nonexecutive director of SDF Limited, a private film production company. David is Chairman of the Remuneration Committee and also a member of the Corporate Governance and Risk Management, Audit and Nominations Committees.

Clive Crouch (aged 66, Non-Executive Director

Clive Crouch was appointed to the Board in February 2016. His 35-year career in media has included senior roles within GMTV, a company he helped launch and position. From 1992 to 2007, he was GMTV’s Sales and Marketing Director. He attended The London Business School Senior Executive Programme in 2003. From 2007 he served as GMTV’s Chief Operating Officer until 2010, taking responsibility for the Channel’s License and Compliance to the Ofcom Broadcasting Codes. He was a founder member of Think box, the ITV programme marketing company, and Clearcast, the quango that pre-clears all advertising copy for compliance to the advertising guidance codes. Clive now operates his own media consulting business and he remains actively involved in the toy industry, advising on such matters as regulatory, promotional activity and licensing. He brings a wealth of relevant management and industry experience to the Board. Clive is Chairman of the Audit Committee and also a member of the Corporate Governance and Risk Management, Remuneration and Nomination Committees.

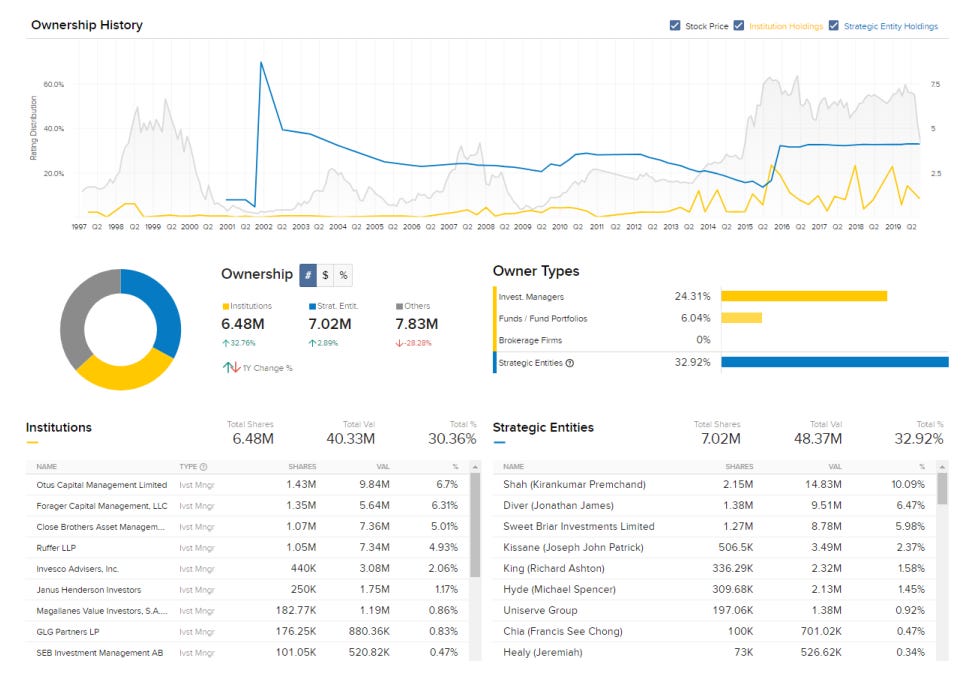

As a testament of Management confidence in the business, there is a large proportion 32% of the business held by insiders. Furthermore 16.5% of this is held by the Group Joint Managing directors. Shah and Diver are both in charge of the strategic decisions of the group of the whole, also called the capital allocation. This incentive is great for shareholders for alignment purposes. Owner-operators have shown to outperform non-owner-operators significantly over the long term.

Capital Allocation

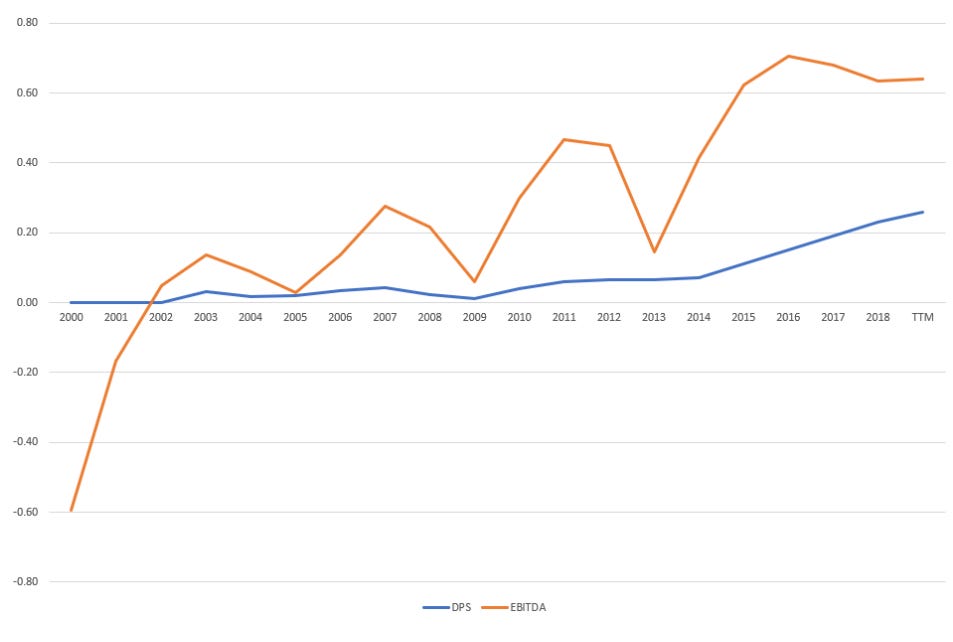

This leads us to capital allocation, what does the company do with the freecash flow it generates. Well, first things first, The earnings and revenue of the business can provide context to the capital allocation. The Revenue and EBITDA for the past 18 years are as shown below:

While these results may not seem too impressive, putting the results into the context of capital allocation may make sense.

First, capital allocation can be boiled down into 5 things:

Paying down debt

Paying dividends

Re-purchasing stock

Growth Cap-ex

Maintenance Cap-ex

One at a time we can tackle these areas:

The company majority of the time has between $1025m of short term debt. Most operations are funded with cash however, the usage of short term debt occurs, however, at just 12x EBITDA it is very manageable.

Dividend growth has been consistent in the last 10 years, currently representing close to a 7% dividend yield despite being less than half of EBITDA. These have proven to be sustainable as a result.

Repurchasing stock is a consistent policy for the company, they have also been selective about these purchases. To illustrate this I have plotted the EV/EBITDA and Shares bought back below. It shows the general allocation of large amounts of cash into reducing the register at points where the EV/EBITDA is very low or negative. Also, more recently buybacks have slowed down considerably, which as you can see above, negatively correlates with the increase of dividend payments. In saying that, recent purchases have occured in October around the 3.504 price, which is roughly where we are at currently

Growth capital expenditure is the area where Character group can leverage it's excellent returns on capital to the fullest. The most recent of which is an acquisition of a 55% interest in Proxy as mentioned earlier. As for earlier acquisitions the group has not shown a particularly aggressive approach in the past, opting to purchase stock as shown above. The shift in focus shows that incentivised management consider this to be a more value-accreditive activity for shareholders. Given the generally strong track record of Character Group in capital allocation, it is fair to be optimistic.

"The Proxy team is focused on reducing the current inventories of slower moving lines. A full review of the Proxy business model is underway with the Proxy management and it is anticipated that, in addition to tighter Group controls over purchases and a substantial reduction/rationalisation of the product lines distributed by Proxy already agreed, this will lead to cost cutting measures being implemented. Whilst the challenging market conditions in Scandinavia are continuing, the Board is hopeful of a significant improvement in Proxy's performance in the current financial year."

Finally maintenance capital expenditure is very minimal, only taking a small portion of operating cash flows on an annual basis, this trend has been consistent, leading to a capital light business. This makes sense given the outsourcing of manufacturing and therefore light operations.

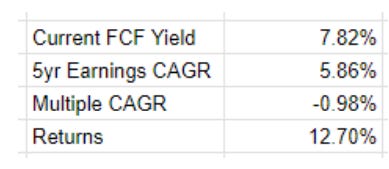

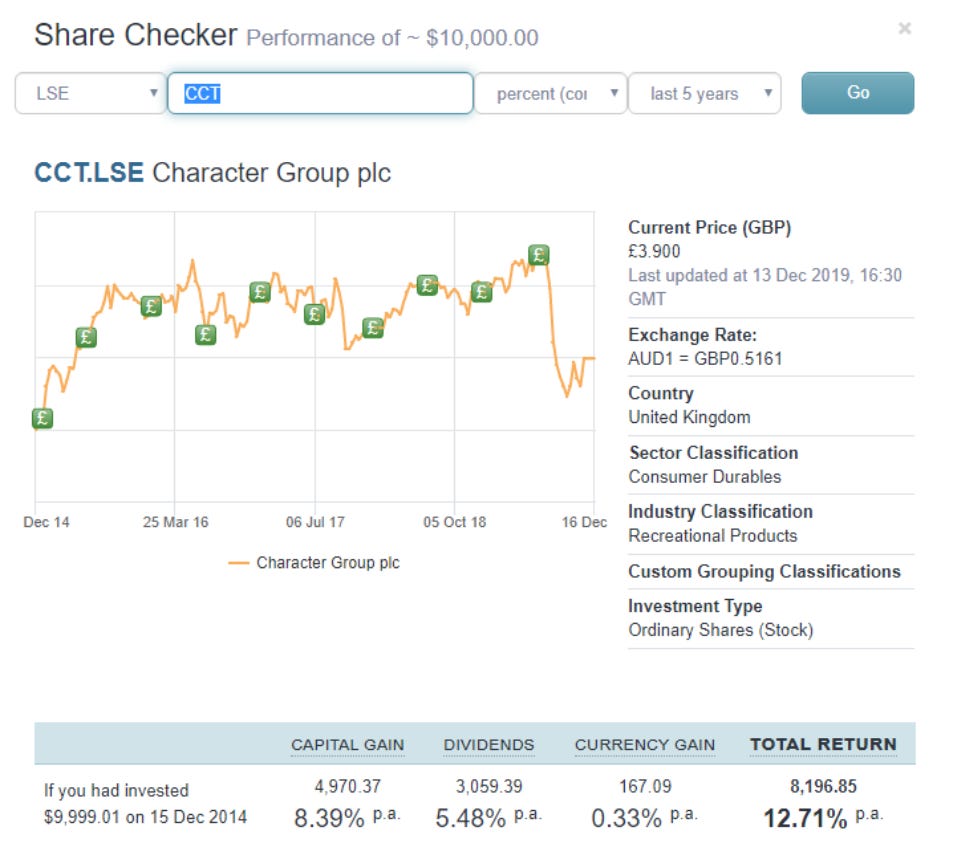

So what does one pay for Character Group? Staying with the trend of FCF yield + Growth + Multiple expansion.

Again, the accuracy of this simple valuation scares me. My reconciliation to the past returns seems to be consistently accurate. Nonetheless, these returns have been quite decent, however where real growth can occur is the multiple expansion on offer for the stock. The current EV/EBITDA is just 5.3x. Given the strength of the ROE, ROIC and recent acquisitions the business is in a very healthy position to allocate capital to add value for shareholders. With $29m in cash on hand, improvements in the Sterling as a result of the recent election, a christmas quarter upon us and maintained stakeholder relations the business is in a good environment for growth. Of course, this isn't without risk, namely the recent downfall of Toys R' Us in Scandanavia has hurt Character in the short term and further weakening of the retail market could occur. The cyclicality of this business model can not be understated and we are at the whim of the consumers' discretionary income, so with a contraction in spending, so too does Character lose revenue. Albeit this is likely short-term but still a risk in of itself.