The PAS Group (ASX:PGR) - One Page Stock Pitch

The PAS Group (ASX:PGR) - One Page Stock Pitch

Retail Net-Net

About

The PAS Group was established in 2004 to capitalise on the fragmented nature of the apparel industry in Australia. The group has progressively acquired a diversified portfolio of well established brands as part of its strategy. As a result The PAS Group is one of Australia’s largest apparel businesses with an established business model and platform providing significant scale, infrastructure and capability to exploit opportunities.

The PAS Group covers both the retail and wholesale segments of the market and has a rapidly growing online business. The group has 280 retail stores with the key retail brands being Review, Black Pepper, JETS Swimwear and Bondi Bather. The group acquired White Runway, an online occasion wear business with a growing number of showrooms both in Australia and internationally.

The group wholesales a number of brands into department stores, discount department stores, specialty retailers as well as approximately 800 independent retailers.

Strategic Vision

The PAS Group’s vision is for every employee and every business within our organisation to never stop realising their full potential.

This is facilitated through:

The financial strength of the group

The business nous of our management

Our holistic industry experience

The professional approach taken to entrepreneurial businesses

Common sense decision making

The PAS Group aims to differentiate from its competitors in the way it conducts its business, continually evolving and embracing change.

Financial Performance

What attracted me?

The stock is trading at $0.145 per share, which represents a 50% Discount on Net tangible assets. This in conjunction with a profitable business is quite an attractive business. Although it is important to break down the business to determine any risks.

Value of their Assets

To truly understand the downside risk that is associated with The Pas Group, it is important to attach a proper value to their assets. While Reported numbers indicate that the stock is trading at a significant discount to it's equity, accounting can be quite misleading as financial information is easy to manipulate.

An appropriate method of determining value is the Liquidation value. This is the total worth of the company if it were to go out of business.

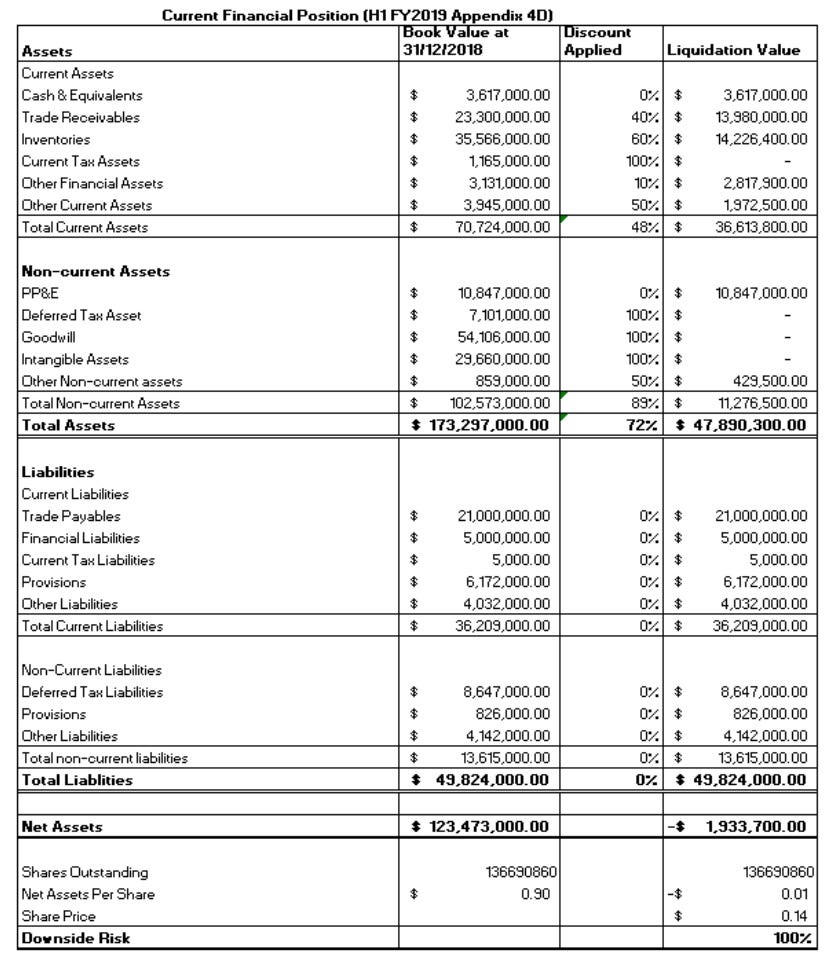

Below is a conservative Liquidation value of the company As at 31 December 2018 Financial Position).

Discount Methodology

To Follow through, please have the 31 December 2018 and 30 June 2018 Balance sheets and accompanying notes.

Cash is 100% Liquid = No Discount necessary

Accounts Receivable I determined that the majority of old debts could be written off in liquidation with maybe just the recent one's being recovered. A Discount of 40% seems reasonable using the below schedule

Inventories in the event of a liquidation could be sold below cost. To be conservative a 50% discount could be used on finished goods, while Raw materials and Work in progress could be discounted completely. A discount of 60% will be used.

Current and non-current tax assets represents carried forward losses and could be completely discounted as they won't be utilised anymore if the company were to liquidate.

Other financial assets includes derivatives used to hedge carried at fair value. A draw down of 10% I deem to be fair if liquidated.

Other current and non-current assets is likely to be prepayments for things such as licenses etc. Could be impaired in the event of a liquidation. A 50% discount will be used

Property, plant and equipment includes depreciation of $25 million, I think in the event of liquidation, no discount is necessary given it is represented at cost rather than fair value

Goodwill & Intangibles both recognise the value of the brand names that the business has. These have been calculated using a discounted cash flow model. Therefore the firm's net assets are pricing in growth. Further DCF analysis would be a form of double accounting for growth. In liquidation, no growth is going to happen, therefore goodwill is valued at $0 100% discount)

Liabilities are not discounted as they will all have to be paid first before equity holders in the event of liquidation

Liquidation Value

As can be seen above, While being extremely conservative the downside risk has worked out to be 100%. This is a worst case scenario. While not the most brilliant Benjamin Graham stock, assuming continued profitability, most tangible assets do not need to be discounted. Therefore we can say confidently that the value of the stock in normal conditions is at least $0.29 per share. By buying at a discount our minimum risk/reward ratio is 11 as the possible loss is $0.145 and gain is also $0.145.

Risks

Liquidation could result in a 100% Loss

The large carrying value of goodwill is essentially the company pricing in growth. If those targets aren't met, impairments could impact the share price. This could actually present an opportunity to us given the already depressed share price we could buy shares with a risk/reward skewed in our favor.

Fall into unprofitable territory, which would result in the NTA being affected and hence impacting the potential reward on our cost per share

Conclusion

If the stock remains solvent there is no downside risk apparent assuming they don't burn assets. The target value is their Net tangible asset value per share of $0.29 per share representing a 100% return on investment. However, with close monitoring i could decide to exit earlier than that should i have reason to believe the assets will lose value.