ZIGExN (TYO:3679) - #2 - Deep Dive

ZIGExN (TYO:3679) - #2 - Deep Dive

Japanese Search Aggregator

ZIGExN is a Japanese company operating in the internet advertising value chain. The name (Pronounced ‘Ji-gen’) is inspired by the corporate vision ‘Over the Dimension’ where Jigen is roughly translated to ‘dimension’ in English, a slogan to illustrate the vast amount of white space that is associated with the increasing flow of online information over time.

To fully appreciate the roots of this business, I wanted an understanding of the intrinsic motivations behind the company’s value proposition. The ‘World-wide-web began in 1991 with a large consumption-based usage due to the bandwidth limitations preventing collaborative usage. In the early 21st century, perhaps through the accelerated innovation during this time due to the allure of lofty valuations allowing for cheap equity finance, the bursting of the dot-com bubble in the fall of 2001 marked a turning point for the web, transitioning to a new normal. This, personified by the term ‘Web 2.0’, refers to the platform-based core of the internet that is taken for granted nowadays. In essence, the interactive nature of the internet shifted from static to collaborative. Popular mediums including Facebook, YouTube, Blogs, Hyperlinks and so on.

This innovation is driven by collective intelligence, but when an assembly of such magnitude occurs along with the increasing hardware improvements, the compounding of websites is significant over time. This is where ZIGExN fits in the broader scheme of things. The value proposition here can be explained two-fold, 1) Due to the increasing volume of information being spread over the internet, filtering that information is becoming more difficult and; 2) ZIGExN aims to address this by utilising a database of information to improve their data matching system & curb the consumer towards the information they desire.

The beauty of this system is that the core service is the same no matter the industry it is applied to, the customers are an advertiser of information & a consumer of information - the subject matter does not impact the service. This provides context to the application of the data aggregation model that ZIGExN pursues. There are similar platform businesses out there that pursue more of a pure-play strategy, some big examples would be Booking, Airbnb, Seek, Domain & Carsales among many. Their reasoning for diversifying the application of this model is to smooth revenue over time and allow them to act with the flexibility to skate to where the puck is going metaphorically speaking.

The man behind this is none other than CEO & significant shareholder Joe Hirao. Born in 1982 in Tokyo & graduated from the faculty of Environment & Information Studies at Keio University. During this time during his studies, he was operating 2 companies & whilst continuing to run these, joined Recruit Co. in 2005 where he quickly climbed the ranks in the internet marketing & HR departments. Due to some commendable effort proposing a new mechanism to attract customers using blogs & SNS along with several awards, he was placed as a director during the founding of Drecom Generated Media Co. Ltd (Now ZIGExN). Astonishingly, he was the youngest director in history at Recruit at just 23, which is quite a feat in and of itself. Finally in 2010 Hirao conducted an MBO & retitled the company ‘ZIGExN’, listing on the TSE Mothers exchange in 2013.

That’s the abridged version of Hirao’s story however, after reading some specific interviews, I want to share some valuable life events that I believe shaped Hirao & why I believe he is an excellent entrepreneur.

First of all, Hirao’s family situation was a lower-class one, struggling with finances where his mother was the breadwinner of the family and his father unemployed. With 3 siblings you can imagine that this budget would have been quite stretched, It’s in this environment where you are brought up with frugality. Couple this with an entrepreneurial grandfather who despite being unsuccessful in his ventures proved to be a ‘dazzling’ existence to the young Hirao.

Secondly, during High school, Hirao was inspired by a certain TV program (He doesn’t say what one) where a Keio University Faculty of Environment & Information Studies IT student ‘entrepreneur’ presented. It seems that Hirao already had the confidence to be a leader so decided to attend that same campus. Hirao regretted this as it was different from what he imagined, this snowballed into frustration which left him wanting a new role model.

Perhaps the most influential & smart decision was what came next. From here Hirao decided to set the goal of meeting 10,000 excellent role models. I doubt he met that goal specifically, but he does mention that he met or spoke briefly with “Employees of famous companies, politicians, world boxing champions, entrepreneurs such as Masayoshi Son of Softbank, Susumu Fujita of CyberAgent, etc”. From this, he gained a rekindling to solve social problems as an entrepreneur. This activity was what drove him to start experimenting with different business ideas.

Lastly, during his time at recruit Hirao’s father had passed away at the untimely age of 53, this was a catalyst for Hirao that cultivated in him realising that he only has one life, as such an evolution of mindset to concentration on one business had occurred from where he wound up his previous ventures and consolidated his efforts on the then Drecom Media business as president of the company.

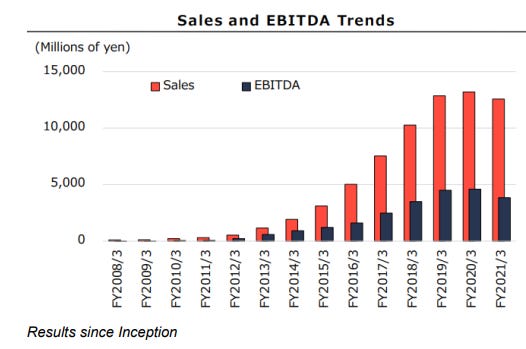

Fast forward to today having turned 21m in operating income in 2008 to 3.8b in 2020, a compound annual growth rate (CAGR) of 54% p.a. Of course this is coming off a very low base so from the time of listing this rate has risen from 925m to 3.8b in 6 years, a CAGR of 27% p.a. is still quite impressive, but has suffered from marginal pressures, particularly the unit economics have deteriorated some 10% and all passed down through the profit & loss to impact the net profit of the business. As such the revenue line has performed markedly better than operating income at a CAGR of 38% in the 6 years since listing.

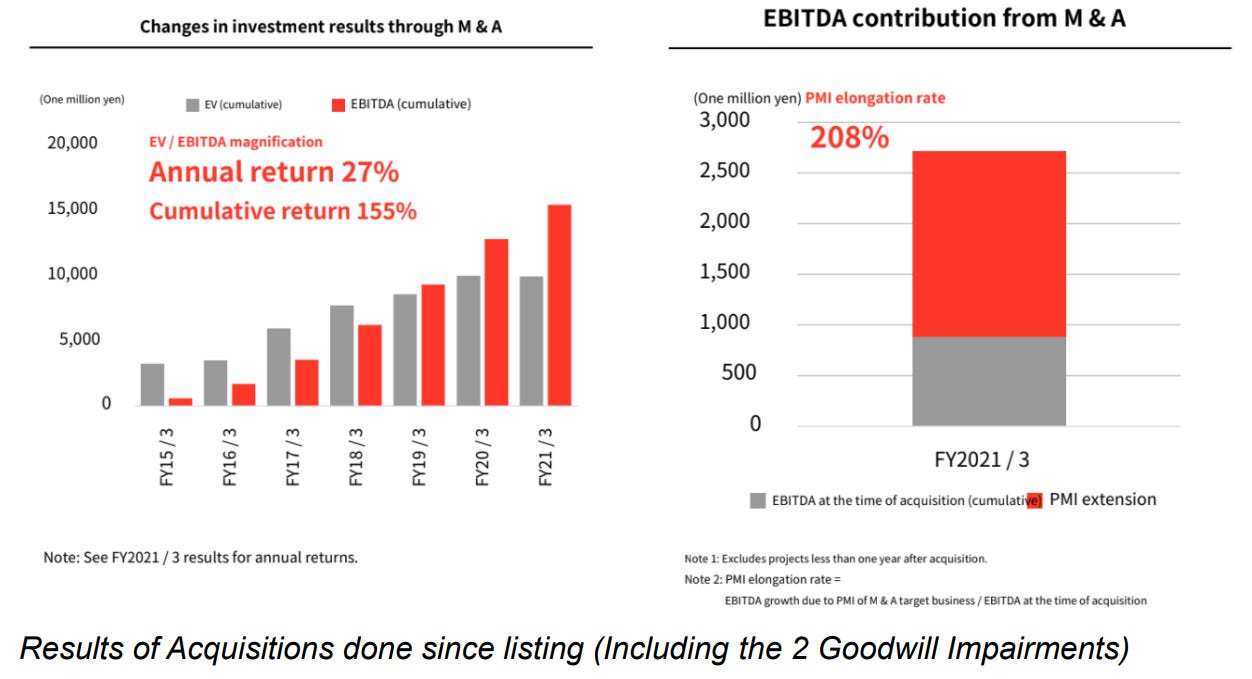

So what does this tell us, well firstly that the business is undoubtedly a fast-growing one, perhaps equal parts skill & luck due to the high concentration into HR in a period where the Japanese unemployment rate declined from 4% to 2.3% driving the organic growth rates of the business. But what I want to emphasise is the skill of acquiring new businesses. They have an uncanny ability to overlay their strategic capabilities and invest like a VC fund with investment returns varying from 2x to 10x the initial capital outlay. This has translated to a 38% CAGR on capital deployed meaning that the average investment is paid back in 2-3 years on average. Inspired by Chuck Akre it has caused an intrigue into just why that is so, what is it about the internal capabilities of ZIGExN that have allowed them to compound at above-average rates of return for such a long time and more importantly, why do I think this can continue?

To get to the bottom of this I did a large amount of reading into employee & management interviews and discovered some interesting details that strike the core of entrepreneurship that Joe is trying to cultivate in the internal culture.

First of all, the hiragana that is in the lobby of their office stands for “Businessman Group” which is effectively what the parent company operates as. To be more precise the parent company itself operates more as a talent pool and as such focuses on hiring skilled graduates and intermediate staff along with nurturing them to become successful entrepreneurs by providing opportunities to deploy these staff to new acquisitions.

In this office the environment is meticulously crafted as well, having a particular focus on collaboration and removing bureaucracy through examples such as having bulletin boards on the stairs and removing the use of elevators within the building for staff. This is to promote foot traffic and just another measure to prevent the ladder-style feeling associated with hierarchy.

This culture of nurturing entrepreneurs is core to the ability of ZIGExN to grow as a company, and the listing is crucial to attracting talent to their corporate headquarters. It’s in this environment that they are nurtured and provided with opportunities to conduct PMI on new acquisitions. In effect, employees are hired to eventually become managers of subsidiaries. This might sound familiar, as this is the exact process that Hirao himself experienced being deployed as a manager to Drecom Media back in 2006 as a director.

PMI is supported by the accumulated database that ZIGExN has built over the past 15 years, which is effectively big data that smaller acquired businesses wouldn’t have ordinarily had access to.

Integral to the success of this strategy is a strong focus on asset value and the ability to utilise their ZVI process to improve the growth potential of the underlying business. The interplay of FCF Yield + Growth is what makes for strong ROI. In this case, the average upfront EBITDA Multiple for the past 6-7 years since the listing is 12x, once you adjust for taxes and the deductibility of previously accumulated balance sheet amortisation, the post-tax FCF yield would be in the range of 6%. Of these investments, the accumulated EBITDA is now equal to 27% of the invested capital, with post-tax being about 18%, which is equivalent to buying businesses and getting paid back in 4-5 years, couple this with a further focus on improving the LTV of these accumulated clients and It’s not hard to see just how high quality this business is.

Before I wrap up my thoughts on this business, I wanted to talk about the approach to strategy that ZIGExN has. If you have looked at any of the businesses I hold, you can notice that each business has a clear and focused vision and a multi-year plan. It’s by no mistake that I value this rational approach to strategy, as it’s the way that I have learned throughout my studies as a CPA. To be more precise, there is a strategic planning process originally set by Michael Porter which starts with the Why (mission, vision and objectives). From here a company would conduct an internal and external analysis to which strategic options are evaluated and therein implemented based on opportunity cost. This is much the same as the way I invest, I’m constantly evaluating which business I feel has the best strategy to grow.

ZIGExN is a bit of an outlier in this respect, as whilst they do have a plan, in addition to their rational plan, the emphasis on entrepreneurship and forming a conglomerate internet media business requires a degree of flexibility depending on the external environment. In this respect, they have embraced a more processual approach to strategy which is a style that embraces that decisions are to be made in a more reactionary fashion rather than years in advance, this is because it argues that change is continuous and messy.

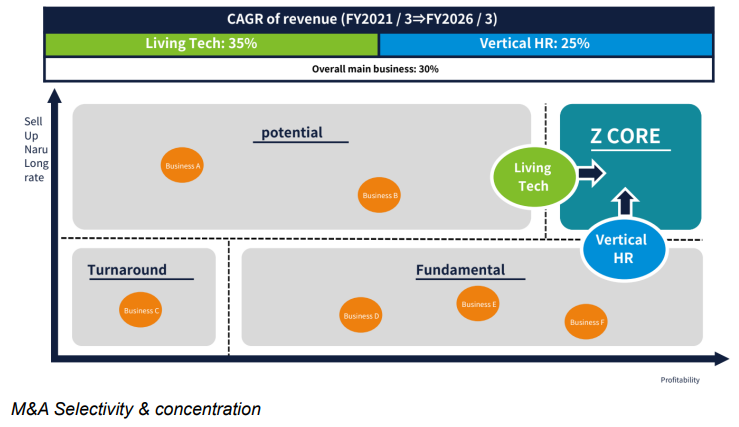

This has materialised in a “Z Core” part of their business where margins are high and sales exceed 10b yen. They aim to conduct M&A in the following situations:

Potential - High sales contribution to the group, poor cost structure that PMI can improve on.

Fundamental - Moderate-high margins, sales that can be improved upon with PMI & business strategy

Turnaround - low sales and margins, particularly imagine these would have a very low price with a clear idea of the potential.

Lastly, a note on how I’m thinking about valuation. I have held this business since April of 2020, having originally paid a price of 357 yen, since then the business has not appreciated by much despite them having added 300m+ of post-tax FCF in acquisitions during the 2021 financial year, of which 1.5b was paid. This entry multiple is equivalent to an upfront earnings yield of 20%, which is far better than their typical entry multiple. This isn’t all that surprising given the environment.

Nonetheless, I paid a price of 7.5x EV/EBITDA or roughly 12x post-tax earnings at the time, and frankly, I believe that the price is the same if not cheaper than it was at the time. If you believe that they can compound sales at 30% CAGR as their 2026 plan suggests with funding from operating cash flow. Then you are likely to see returns that when including the 1% dividend yield and some potential re-rating far exceed 40% p.a. Over a 5-10 year period. Personally, my hurdle is 25%+ and believe that this is a business that can exceed that hence why I hold it but to achieve the goals I only need to get 13%+ each year. For this reason, I don’t mind if it doesn’t work out as expected, I am comfortable taking those odds any day of the week.

Incredible to read about this business and individual. Thank you so much for your thoughtful post.