Litigation Capital Management (LSE:LIT)

Litigation Capital Management (LSE:LIT)

November 2023

Litigation Capital Management (LCM) was founded in 1998 and provides dispute finance in Australia and the UK. Historically it has operated utilising its own balance sheet to fund proceedings but has recently delved into the asset management space with third-party funding. Its products and services include dispute finance for companies, international arbitration, and law firms; disbursement funding; enforcement funding/purchase of award; and adverse cost and security for costs. Long time readers of my work would recognise this company from (you guessed it) a previous write up I had written back at the end of 2020.

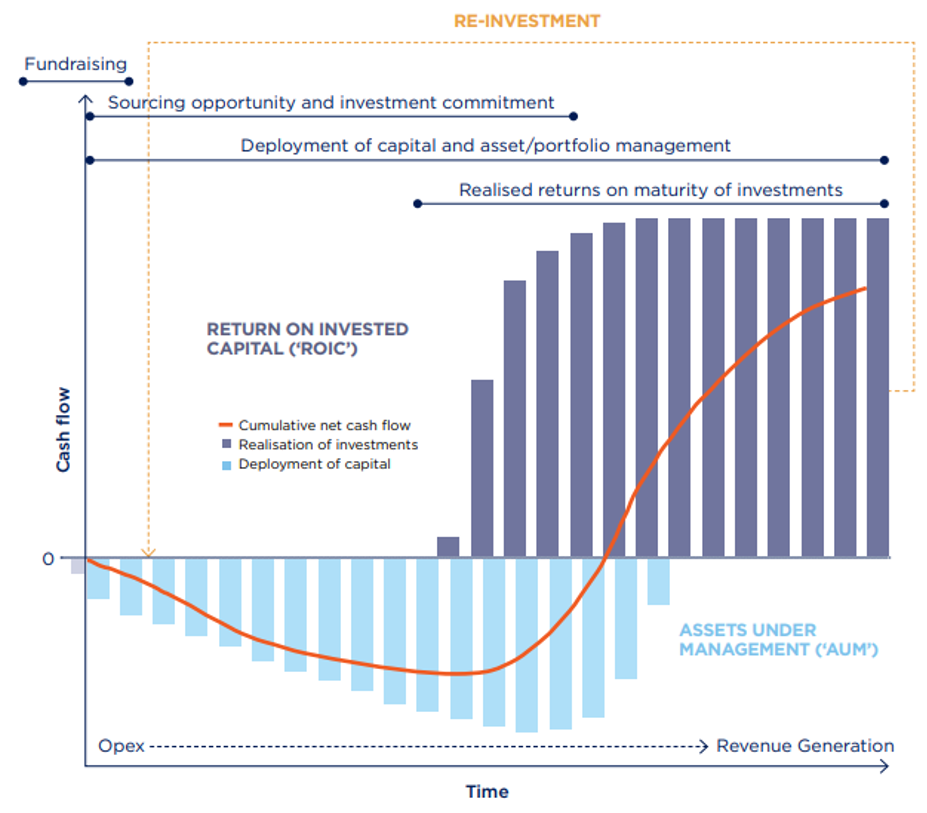

Cases funded by LCM are typically 3-4 years in length and typically they get paid on a multiple of invested capital, with that multiple increasing as the case goes on, protecting their annualised returns. Over time the internal rate of return (IRR) on these cases has been 78% p.a. with an average return on invested capital of 1.78x on their investments (both on a gross profit basis excluding general LCM operating costs).

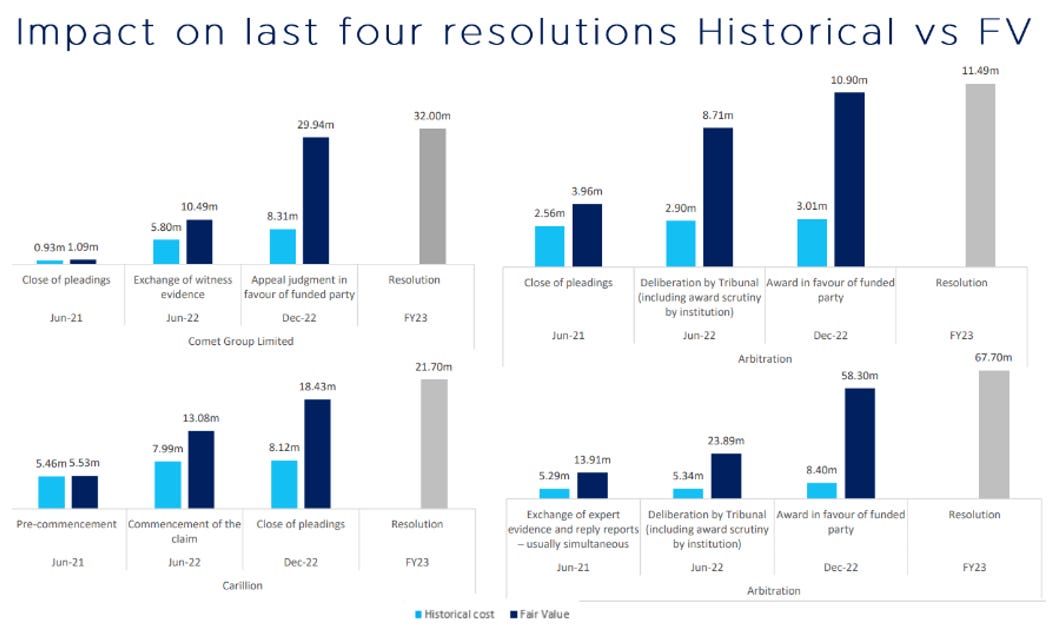

Importantly, just a few months ago the group made the decision to move to fair value accounting. If you took the liberty of reading my linked write up from a few years ago I emphasised that I thought the business was misunderstood due to it’s cost accounting. With the introduction of fair value accounting, the group will book unrealised profits at key milestones in the case. The issue with fair value accounting has been that it opens the possibility of overlaying significant levels of ‘judgement’ in the recording of these litigation assets. This increases the risk of impairment drastically and could mislead investors as to the real profitability of the business. LCM has assured investors that their approach is robust and devoid of management intervention as was quoted in the 2023 earnings call. As you can see there is most profits booked as awards or claims are concluded on.

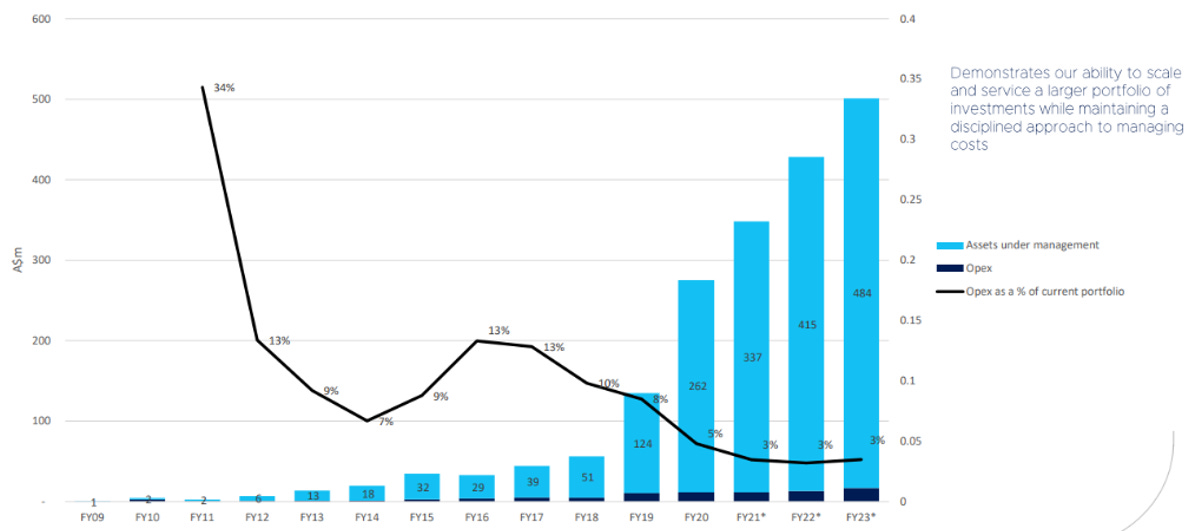

With this out of the way we can talk about the growth opportunity. As discussed in my initial write up, I was expecting a medium-term inflection point because of the introduction of the asset management business within LCM. This would allow them to leverage their performance to great effect and generate very significant performance fees. As an example, this investment announced back in June 2023 resulted in a near doubling of the gross profit to LCM due to the performance fee aspect (granted this was a particularly successful investment).

Thus, the main driver of growth for this business will primarily be the level of interest from third party investors, but also the maintenance of their historical returns on capital. However, in my view, even if they were to simply operate as a direct investment business as they have done in the past using permanent balance sheet capital, they could still represent a rather appealing compounder in my view. The asset management arm supercharges returns dramatically and should result in a significant boost to the returns on equity of the business. In 2019 they started raising third party capital and given their metrics it is paying off.

LCM is in part a straightforward asset management business, and highly complicated litigation funder, but the extremely important aspect is the ability of LCM to correctly underwrite these cases and be right enough times on average for the business to generate an appealing return, which in my view is a ‘black box’ so-to-speak and highly reliant on its internal practices. I would be more concerned if due to fair value accounting, a long-running case could lock up a large amount of capital and unrealised gains and risk impairment such as the Burford YPF deal for example, even if that case was a significant return for Burford, it was a significant part of its balance sheet at fair value (not at cost). There is always the risk that these cases do not eventuate as expected, but returns are substantial enough to offset a couple duds. On valuation, LCM trades at 1.25x book value and on direct balance sheet alone, the business generates double digit ROE. The real value is in the asset management business which allows them to operate with economies of scale, assisting margins, and generate performance fees leveraging third party money. I believe that due to this, LCM can more than double it’s returns on equity, and that the market isn’t pricing this in at all. However, with the nature of the business model, I could not justify a significant position.