Subscriber Q&A

Hi Everyone,

Today’s post will be something a little different. I’ve reached out to you all for questions to which I will answer below:

Q: The Shameless Cloner

How do you separate good/bad from such early-stage companies like DSW Capital for example? The valuation seems also quite hard, given that there is no long proven runaway of numbers.

A: Tristan (Hurdle Rate)

First of all, whilst DSW is a recent listing, it dates back to 2002 so certainly not an early-stage company. There is access to financial statements back to May 1, 2017, onwards, which is almost 6 years of data. In my opinion that is ample data to be able to assess the traits of a business. If I was to put a number on what I would start to feel uncomfortable it would probably be 3 years or less. Furthermore, this video actually gives us the last decade, and 2002 + 2008 figures for fee earners, revenue and locations, which are good data points to have.

To answer the latter part of your question, it’s something I would reserve for paid subscribers so I will refrain from any specifics in this post, but I will suggest that results on Tuesday whilst not necessarily pretty given the slowdown in M&A, will be a clean set of numbers with statutory profitability.

Q: Joopajoo76

What are some sources of competitive advantage in a service business?

A: Tristan (Hurdle Rate)

Notoriously difficult question to answer, but I suppose to answer this there is 2 sources of competitive advantage financially, a cost leadership position and a revenue leadership position.

Cost leadership would constitute higher margins than peers, which in a service business like an accounting or law firm, means you have either highly productive employees, cheap employees or little to no overheads. What that looks like would differ from firm to firm.

Revenue leadership would look like easy client and employee Acquistion. Maybe you have an appealing partner and employee offering which means lateral hires naturally gravitate towards you. Maybe you have a great reputation of being consistently reliable and excellent in what you do.

It’s hard to really answer this question well, but such is the nature of the service business. It’s competitive, but by its very nature, capital light so any above system growth is highly valuable, even if only a little.

Q: Niko

What are your metrics on evaluating management?

A: Tristan (Hurdle Rate)

For me it largely comes down to intuition at the end of the day. They are people. Some things that may help reach a conclusion:

Do they do what they say the will? Look year to year at what they want to achieve.

Do they change the story often?

Track record

Tenure

Compensation Incentives

Ownership (and changes in ownership)

Aggressive or conservative terminology?

Again, this is not a question you can just land on a process for, in reality it comes down to a case-by-case basis and intuition.

Q: Trading Melons

What is your process for finding ideas?

A: Tristan (Hurdle Rate)

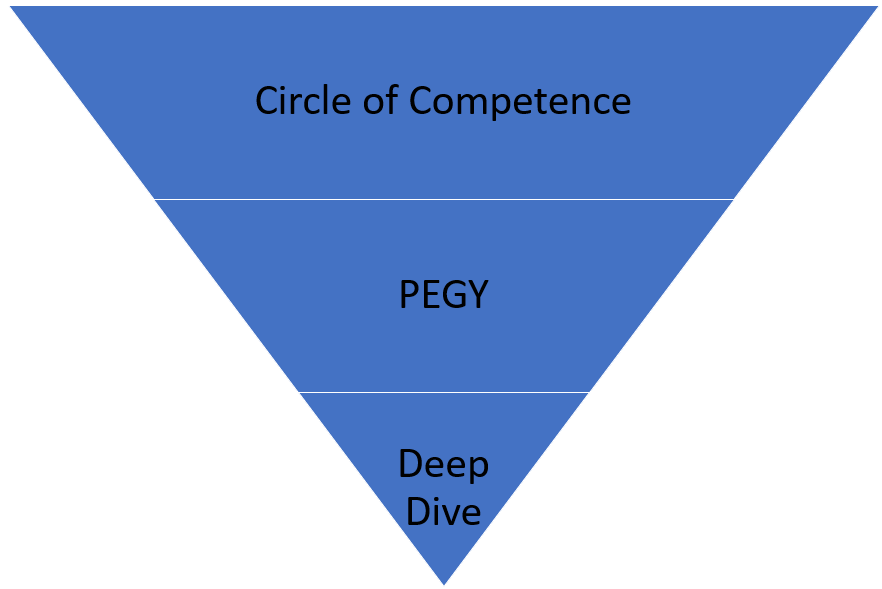

There is no process in particular, but I like to think of it as a funnel. I like to sort of add ideas in the top of the funnel on the basis that I think it’s in my circle of competency of professional and financial services. Then I only really pick it up if it’s an appealing valuation (PEGY - multiple/growth+yield), and that’s looking at perhaps trailing growth, my initial impressions or what analysts estimate as an idea of potential appeal. Only then will I start to dig into an idea. The funnel in very simple terms might look something like this.

Q: Olivier Marz -

How do you construct your portfolio? How do you position size? Do you have large caps?

A: Tristan (Hurdle Rate)

Historically position sizing for me was all equal positions at cost, as I had consistent cash flow coming into my account that was material versus the size of the overall portfolio. These days, there is pleasingly, less impact from savings and I had to change my approach.

Overall, I want a minimum 6 stocks and maximum 8 stocks. I have experimented with how many I am comfortable with and frankly, less is more (for me particularly), but I do still want the benefits of diversification so landed on this. It is about the same amount Greenblatt recommends in his class notes. For me I similarly think I will hold things for 3-5 years, so this simply means I need to invest in anywhere from 1-3 ideas a year broadly.

To put it simply, I size on relative attractiveness, but restrict myself to a a broad range of 10-20% position size. I do let it vary above and below as I am not bound by this rule, but when considering how much I want that’s generally the range I’m looking at. Lately, I have been sizing these on a forward 3-5 year PEGY ratio. I have an idea after my analysis of what growth I expect the business to be able to get, and how much capital can be returned as a dividend, then I compare that to next years PE ratio, using enterprise value as the numerator, rather than market cap. It’s crude but I think it covers all the crucial parts of a successful investment strategy. Currently my weight looks like so.

Lastly, I don’t have any such restrictions on size, so I certainly consider anywhere from pico-cap to mega-cap, it’s just all about the combination of value and growth on offer. There is a larger quantity of smaller companies, and less investor interest, it makes sense that I have tended to land in the smaller end of the ballpark due to inefficiency and quantity of ideas.

Q. Pieter Leeunwenburgh

What you look for when doing analysis of the types of company you prefer? What financial/non-financial criteria you use for buy/add/trim/sell (or equivalent)?

A: Tristan (Hurdle Rate)

To answer the first part of the question. It is highly dependent on the business I’m looking at. Not all the businesses are the same even in my small niche. Perhaps in firms it’s high profits per fee earner driven by the charge out multiples + utilisation (Productivity), low levels of non-fee earning staff that, high staff retention and successful recruitment drive. But there’s other things that I own too like Diverger which has a managed accounts business and a training business, the key drivers are different there such as FUM net flows, member firms and perhaps training hours. Getbusy and Reckon are SaaS models so again different drivers such as ARPU, LTV/CAC and so on. Basically, you want to keep an eye on the development of the say 3-5 key drivers of a business, the people involved and the valuation of that business.

And trading can be valuation driven, or it can be a qualitative development either favourable or unfavourable. It’s again to be considered on a case-by-case basis. There are no particular criteria, if earnings power raises by a lot but the price remains, I might add etc. For example, I owned Sequoia going into the announcement of its Morisson’s divestment, and I immediately doubled my position as I considered the price movement irrational for the value unlock.

Q. Alexandru Dragut

How do you evaluate the competitive advantage in small caps?

A: Tristan (Hurdle Rate)

This is somewhat similar to the second question but instead of ‘service business’ it is ‘small caps. I suppose I am really only looking at service business so broadly it’s a lot of the same stuff. As to how size impacts this, for the most part it tends to be fragmented so again, the advantage is on how well they can manage costs or manage recruitment/growth.

In some rare scenarios you will come across a small company, which still is a dominating player. For example, I owned a company a couple years ago called Class (ASX:CL1), which has since been acquired by Hub24 (ASX:HUB). That company was not too dissimilar to the strength of Xero’s position in Australian and NZ Accounting software, but it was a much smaller and niche market, being Australian self-managed superannuation fund (SMSF) software. It was the first cloud SMSF software and had a 28% market share of all SMSF’s which continually grew stronger as clients transitioned from end-of-life desktop SMSF software to the cloud. With 28% of the market, they were generating revenue of just A$38.3m, with net profit margins in the mid 20s. If they controlled 100% of the market, they would only be generating a profit of ~A$30m. If you valued that on a 30x multiple you would still be under a A$1B company. So, I don’t think size plays a role, but rather as always treat it on a case-by-case basis. (I wonder if you can see a theme here?)

Q. therealprweaver

Could you give an example of where you like to pull data, and/or perform your own calculations, so that reader can replicate? i.e., some would say you need to adjust SG&A for a true ROIC.

A: Tristan (Hurdle Rate)

This isn’t a well-structured question, but I get the idea of it as asking for a practical example.

Take for example without giving too much away in my most recent write up on Begbies Traynor (LSE:BEG) I dug into some commentary from the MD saying they have 20% headcount capacity. I know from my knowledge of a professional services business charging on a hourly billing model (They also have % billing but you can read that in the write up) that your wages are fixed, and that the goal in a firm is to maximise what’s called the utilisation rate. It’s effectively the % of billable hours in total hours.

With 20% headcount capacity he is basically saying that they are 20% below the maximum utilisation rate they could get, which in my belief would be ~90% of total hours (employees need atleast 30-45min a day for admin-based tasks). A move from their current utilisation to the max utilisation, because wages are fixed would result in 100% incremental margins. This is important, as the group has a certain mid-teens margin. I identified that based on data scraped from the UK government (Insolvency notices are reported real-time), that there was a large increase in work demand on the horizon and that it was likely that utilisation would increase, and as such due to the mix of 20% increased work on a division that was 85% of the business, with group margins in the mid-teens, that you are basically getting ~5x the increased workflow in profit accretion (because you are leveraging 100% incremental margin) and as such profits would increase a lot more than just workflow.

So, with data analytics scraped from government leading indicators (Insolvency appointments), I derived that it would be unnecessary to hire to soak in the growth in workload and hence margins would increase due to improved productivity. Lastly, I identified their position in the capital stack and how they get paid, and how long it would take them to get paid, identifying that because of the inflow of more complex cases, that their WIP (unbilled income) would likely increase as a result, leading to increased invested capital, however it pales in comparison to the profit potential on offer.

Q. therealprweaver

How much time do you spend thinking about the probabilities of outcomes, and which financial metrics are the best to evaluate the ‘odds’ you get. (Vs just finding a good company)

A: Tristan (Hurdle Rate)

I find that probabilistic thinking is extremely difficult, in my case it is mere intuition. I sharpen my blade by focusing on a narrow circle of competency, flipping rocks and saturating my head with a few different areas of business, just so that I can garner some semblance of edge in thinking over others. It will never be perfect, and I will never pick the odds perfectly. The aim is merely to be better than average.

Breaking down odds into 25% chance of making x or 10% chance of 10x never made much sense to me, so it’s not part of my process. I think predictability is much lower than, and it would be more like there is a 20-80% chance this 10x ha-ha. In other words, I don’t think choosing a chance is a good way to think about it. Rather, I think you can just do your best to tick off the risks, and tick off the catalysts or growth drivers to the best of your ability, apply a significant margin of safety, then wait and see.

Ok I think that is enough questions for this post.

If you all enjoyed this type of post, I can consider making it a recurring thing, possibly each month I can run a poll for questions. Please give me feedback or let me know specifically if you want to see more posts like this. If you do then it is more likely I will.

Kind regards

Tristan