Subscriber Q&A - Reviewing Prior Investments

Subscriber Q&A - Reviewing Prior Investments

October 2023

Q:

Hi Tristan! Love your blog, it’s been very helpful as a student. Could you walk through (a very high level is fine) some of your favorite case studies of prior investments? E.g., what the initial thesis was, how it played out, if your thesis was the reason for any price discovery, why you exited when you did, etc., One of the things I struggle with the most is getting that “tight feedback loop” going post-investments.At a high level I picked out several investments:

Kelly Partners (ASX:KPG)

Initial investment in October 2019, Thesis evolved further over the next year as I learned more about the business.

From October 2019 Write up

“Kelly+Partners is a Founder led business with a strong incentive lead culture prevalent throughout the business. Brett Kelly is focused on the development of people, which long term represents sustainable value creation. The Tuck-in and Marquee inorganic growth acquisition plan represents a strong development of brand name and awareness, with a hopeful end result of a word-of-mouth/network effect throughout Sydney. This network effect will assist organic growth from customer referrals etc. This combined with a diligent capital allocation turns this into an opportunity i would be glad to hold over time as i watch the business develop. Cash flows are strong, and the price seems relatively cheap at 8-9x Owner’s earnings Adjusted for NCI. Assuming some growth a payback period of 4-7 years is not outside of imagination. Of course, there is some strong competition however, with a fragmented market building market share should not be too hard with significant opportunities abundant.”

Sometime between late 2020 and mid 2021 current substantial shareholder PR Real Value begun accumulating their position in the company. I myself was mentioned in their H1 2021 letter. Their notice was given in June 2021. Given the volume of shares in that period it appears the vast majority of their shares were acquired in April and May 2021 (see below).

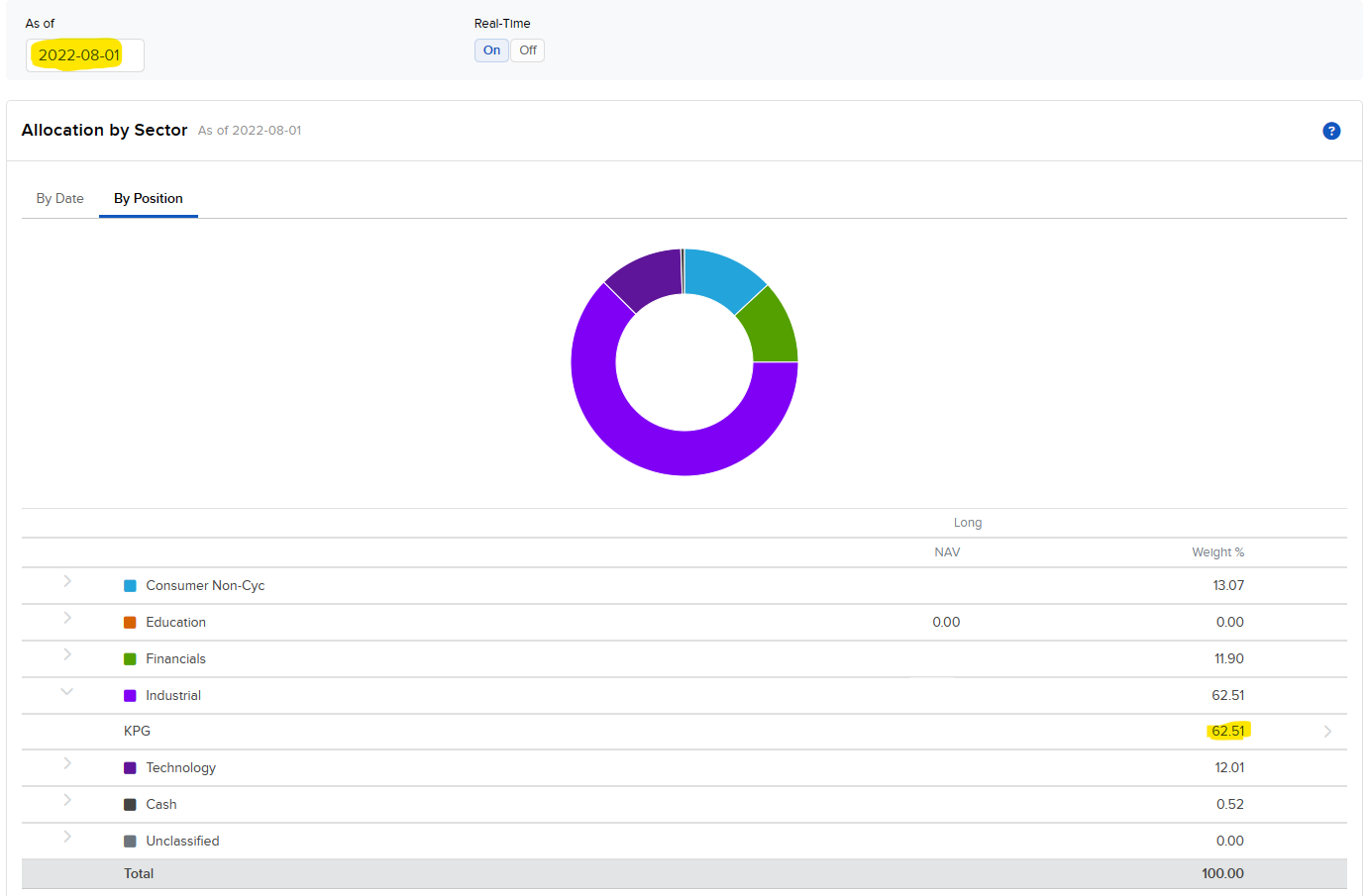

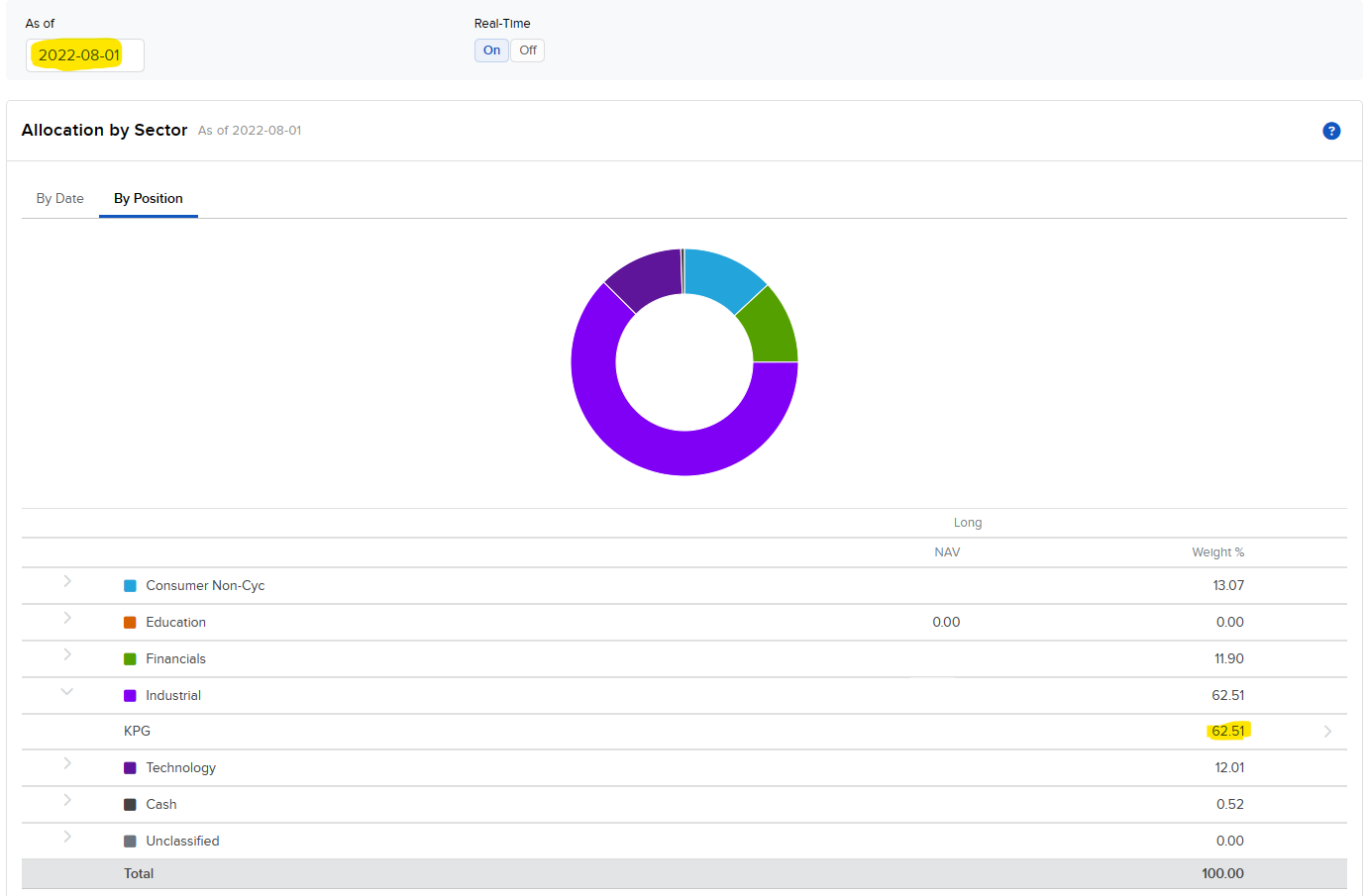

On the release of their results in August 2022 they unveiled plans to expand internationally, which I was far from enamored with. At the date of results, it was 62.5% of my account (IBKR allocation shown below).

I held steadily through to August 2022 when I made my first trim of the business, and over the subsequent months I made a number of new investments, using KPG shares as my funding for those transactions. You can see my sale trades below along with ending return posted on twitter at the time.

We hold a few shares in the new Hurdle Rate Unit Trust, but it is not even remotely close to the conviction I held in the past. I remain vested and confident in their long-term prospects, nevertheless.

My takeaways here are to ride winners as long as they make sense to do so, and that multiple expansion does not compound, only earnings do.

Collection House (ASX:CLH)

This investment is actually perhaps one of those I am most proud of, as I conducted very deep research, only to sell a few months after at a breakeven price and avoided a catastrophic loss shortly thereafter.

Initial write up in September 2019. I invested despite a significant debt load. It was a case of a classic value trap, unaligned management and a misinterpretation of the true earnings power of the business.

Luckily, I sold the stock as soon as Anthony Rivas resigned (Announcement below), taking only a loss on brokerage (<1% loss).

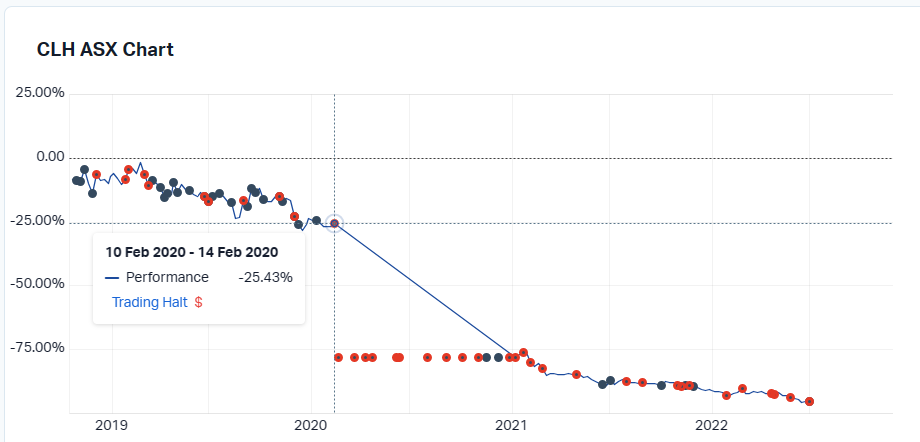

Continuing on the business went on to result in a catastrophic loss having been placed into a trading halt in February 2020, which was lifted at a >70% lower price in January 2021.

Takeaway is to place further emphasis on the debt, quality of earnings and the incentives of those at the top. After this investment I predominately focused on net cash founder-led businesses with extreme levels of cash conversion and net nets for the following 6 months…

Carnival (NYSE:CCL) - Cash secured Puts

In the depths of covid, I was fully invested and lacked cash flow. Thus I put my mind to thinking about how I could raise more cash to invest. What came from this was the Carnival puts.

I suggest reading the entirely of the linked write up, but it was in effect an observation of a business trading at a deep deep discount to book value, and options which had such a high implied volatility, that the premium on deep out of the money puts would yield high double-digit ROI in mere days. If i was placed, I would have owned carnival at a cost basis in the mid-single digits, despite tangible book value in the 30s at the time.

I viewed the chance that Carnival would reach that as remote, and even if it did, I was happy owning it at the strike price, so it was highly asymmetric. I compounded a small position size several times and generated a total return of 217% in just 15 days. Annualise that…

My takeaways here are to look for highly opportunistic investments and act decisively when you find one. My only regret is that I didn’t liquidate my other holdings and do this at a much greater scale.

I hope you enjoyed this post, I wanted to respond to this question so I decided to make it a post.

Where could I find more info on your trust - legal form, how did you come to idea to start it/open it to outside investors, who administers it, who are eligible investors etc. ?