Portfolio Update

Portfolio (As at 31 May 2023)

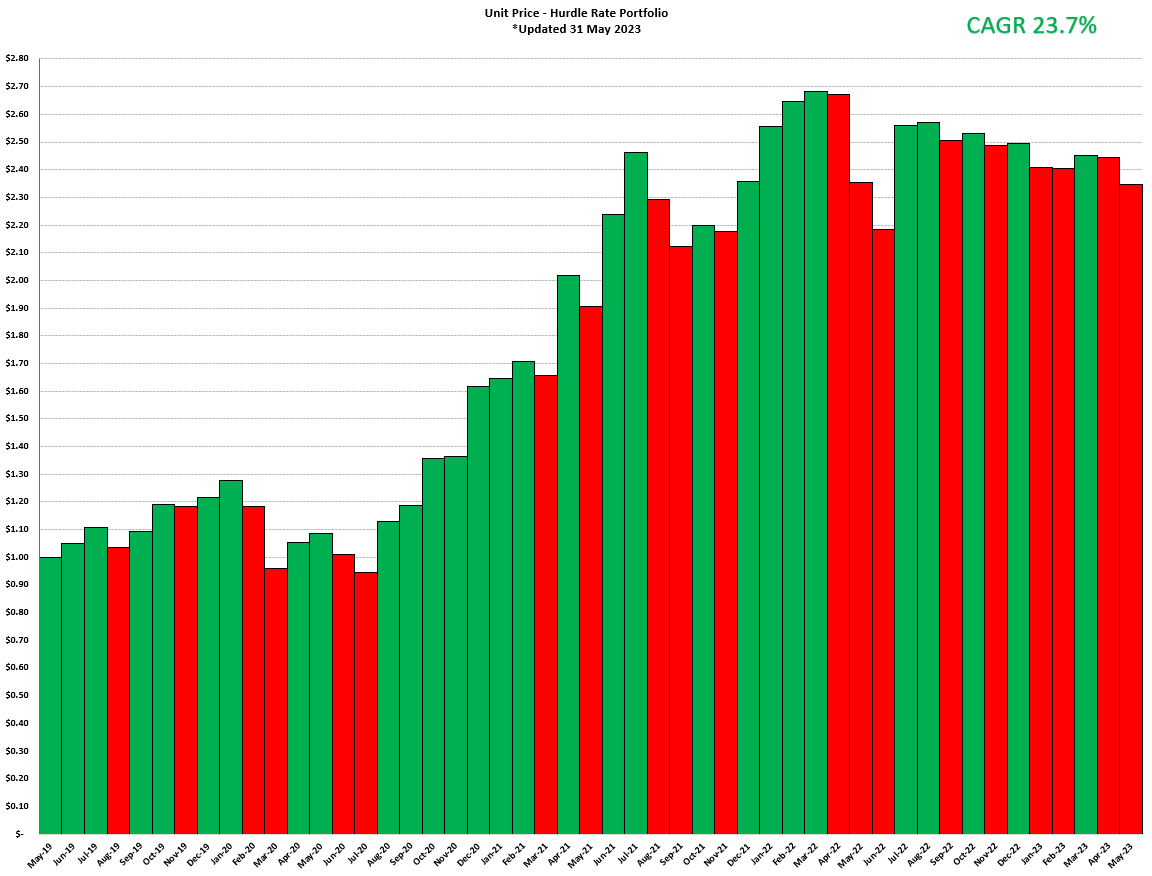

Performance Since Inception

Commentary

For the Month of May 2023, the portfolio returned -4.0%.

Note that this month I started a privately held unit trust for investors, mainly organised via. direct rapport. If this sounds interesting to you, feel free to email or twitter DM for more information. This is also the reason for the large increase in cash weighting, which I anticipate will disappear as I allocate the capital next month.

I will be continuing to report results on a ‘consolidated basis’. That is, including all portfolio’s I am running which going forward will be the Hurdle Rate Unit Trust and my own personal SMSF. SMSF rules allowing a maximum of 5% of ‘in-house’ assets do not permit me to invest my retirement funds into the unit trust, otherwise I would do so. However, my previous discretionary trust positions will be rolled into unit trust units, and it will effectively just be the Unit Trust + SMSF going forward with the exception of any minor contribution from the new 0.1% position made outlined below.

More broadly, my portfolio is going in the opposite direction to the market, similar to what it did last year. I am actually happy to see such a result, as it means I’ve got a low beta differentiated approach. It is the culmination of the work I’ve done to truly do something unique, and to have personalised clarity of thought which I expect to yield widely different results to the market over time.

Sequioa Financial Group (ASX:SEQ) - 20.1% Weighting

First, if you haven’t done so already I have released the deep dive during May which you can read below:

At the start of May, Sequoia presented at the

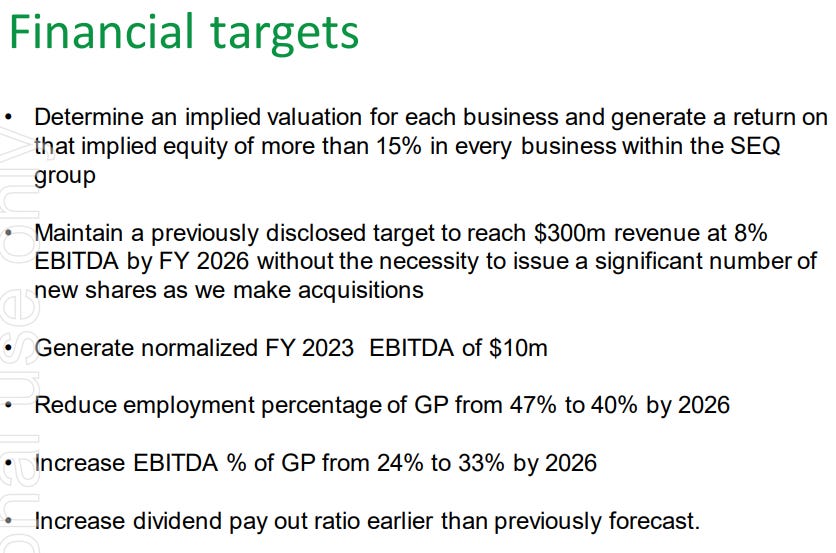

conference in Melbourne along with several other companies I am interested in. Unfortunately, I am based interstate and have commitments as a full-time employee and could not attend. Nonetheless, Garry released his slides on the ASX and I managed to discuss the presentation with someone that attended.Financial targets were stepped out in a different perspective in the slides as shown below. These targets are largely not new however, I have not seen cost base improvements mentioned before.

Furthermore, it stepped out a new capital structure which clearly lays out that they expect the business to have $40m of cash post deal, and henceforth as at 25th of April an EV of $38m, which given the EBITDA above is <4x EV/EBITDA, for a negative working capital service business. As represented by my sizing, I am quite excited about it.

At the tail end of the month, the group was meant to receive the next tranche of Morrison’s divestment settlement. There was an announcement made on June 1st which I will talk to more in next month’s update.

DSW Capital (LON:DSW) - 10.5% Weighting

During the month, I was fortunate enough to have a 1 on 1 discussion with James, which was extremely interesting which you can read my notes of here. As mentioned in the post however, my recording failed to pick up sound, so I had to scribble post-call notes after the fact.

Later on in the Month, the company released its full year results which came in as shown below:

Revenue/Fee Earner £193k (£237k or -18.6%)

Revenue £18.3m (Flat)

EBITDA £1.5m (£2.2m or -31.8%)

PBT £1.4m (£2.0m or -30%)

SBC is estimated to be £0.3m and a tax rate of 21% mean it'll be ~£0.9m NPAT.

On this point, I suspect there may be a write-back of previous SBC which was due for vesting, but I am not certain. This would increase the NPAT by a couple hundred thousand.

EV of about £9.8m on what I think are depressed earnings.

Comparing this to my initial deep dive the FY23 KPI’s compare as shown below:

As shown above, the key KPI's I had modelled out in my deep dive have largely all fell short. The key reasoning for this is a flat workload on 12% more fee earners along with an increased investment in central resources including a planned investment in recruitment staff. The timing is unfortunate as even in my bear case I wasn't modelling an aggressively sharp drop in Revenue/FE and even then, it was GBP £200k in FY24 rather than the £193k in FY23 we have gotten.

A positive is as alluded to in both my deep dive and the 2H23 trading update in January, I said that the model brings in better cash conversion when the ending quarter is lower than the PcP and worse when it grows. In this case Revenue is flat YoY for the full year, but down quite a bit for H2 YoY, meaning it’s likely that the license fee accrual is also down on the year. Add to this the higher headcount meaning potentially higher employee entitlements and I suspect a quite strong cash conversion. In the update they state cash is only down £0.1m despite paying out £1.26m in dividends over the year. As they are unlikely to have any financing cash flows, and I estimated a NPAT of £1.1m (after adding back SBC), it seems likely to see Cash conversion of >110% for FY23.

In saying the above however, it doesn't break the thesis, I'm of the view that they're now just over resourced at the parent entity and have ample capacity to soak up new partner firms, whether they be organic hires, breakouts or acquisitions. PBT is 7.7% of the network revenue whereas the average since 2019 has been 9.8%. This is despite a 16% hike in revenue share via increased license fees and profit share. The culprit being significantly greater central headcount from just 1 in 2019, 6 in 2020, 9 in 2021, 16 in 2022, and likely closer to 20 in 2023. I doubt we will see the lack of central overheads they had prior to listing but do expect that with increased revenue share they can offset much off the cost, and suspect they receive an ROI on their overhead investment as well, not too dissimilar to what Kelly Partners $KPG.AX did shortly after IPO as discussed in one of my deep dives on the company. I view these as non-recurring in nature and adjust themselves over time. I think a similar opportunity has presented itself here with DSW Capital and I am excited to take on a larger position to capitalise on this.

Prime Financial Group (ASX:PFG) - 14.7% Weighting

During the month, there was no news for Prime (outside of a few buyback announcements), and LinkedIn insights show no material move in employees over the month. There is no change on the previous month in terms of thoughts as a result.

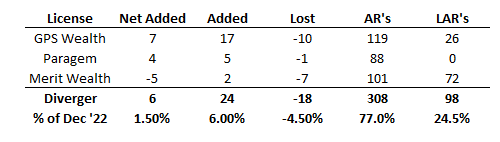

Diverger (ASX:DVR) - 4.4% Weighting

Per the Financial Adviser register, Diverger closed the month with 406 advisers, +0.75% over the previous month bringing it to +1.5% net additions for CY23 to date. Importantly, I want to point out the errors in my data from April. I had mistakenly classified advisers excluded from providing SMSF advice as ‘Limited’ or ‘LAR’s’ but that was wrong, it is advisers which are limited ONLY to providing SMSF advice which are effectively accountant’s with an add-on. I have corrected this and it shows in line with the initial comments made on my first management call with Nathan.

The price of the stock closed the month at 81c per share, when considering FY25 EPS targets of 18c-22c and a payout ratio of 40-60%… the stock looks incredibly cheap. I have purchased more this month to capitalise on the opportunity.

I remind you below their priorities.

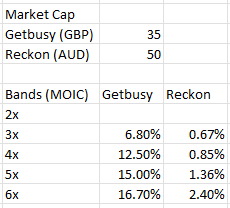

Getbusy (LON:GETB) - 1.6% Weighting

During the month, there was no notable change with Getbusy and I couldn’t find any major news. However, it’s old parent entity Reckon (ASX:RKN) announced an AGM resolution (also discussed in the Chairman’s letter) which is clearly inspired by the Cash distribution plan announced by Getbusy earlier in the year.

Your Board is very aware of the disconnect between the value of your Reckon shares represented by the share price and implied valuations based on revenue or EBITDA multiples usually applied to software companies, including the multiple applied to the sale price of the Accountants Practice Management Group. We firmly believe that there is considerable unlocked value in Reckon, more so than our current share price, and our management team are working hard to crystallise this value. To that end, we have included a cash incentive plan for our CEO and CFO that is subject to shareholder approval. The reward under the plan is significant, but so too are the targets. A return to you in cash of approximately three times the current market capitalisation of Reckon for any payment over the next six and one half years, up to approximately six times the current market cap for the maximum payment. It is indeed a large hurdle, but it is one that we believe is achievable if we can execute on our strategy. The sale of Accountants Practice Management Group shows that our management team can unlock unrealised value and deliver shareholder returns that exceed that of our ASX-listed peers.

~ Reckon 2022 Chairman’s Letter

The terms of that plan are set out below:

The payment of cash under the plan is contingent on the following Payment Conditions:

The participant being an employee of Reckon at 31 December 2029

the cumulative total of the following payments in respect to Reckon shares paid or received by Reckon shareholders from 24 May 2023 to 31 December 2029 (Shareholder Return) being at least $150,000,000:

Dividends

Distributions

if there is a change of control transaction occuring whereby 100% of the issued capital of Reckon Ltd is acquired by a third party (control transaction), the consideration received by Reckon shareholders under the Control transaction.

If the shareholder return includes shares or securities in another entity unrelated, whether in addition or instead of cash, the board may determine the value of the shares that will be factored into the calculation, in its discretion.

The shareholder return will not be reduced for any tax payable by shareholders and will be adjusted upwards for the effect of franking credits.

If the payment conditions are met, the amount will be calculated by the board based on the following distribution schedule:

Variation to Shareholder Return Bands and Cash Distribution (Potential amendments)

Reducing the cash distribution for a participant by any amount paid to the participant under a reckon long term incentive plan

Making changes to the shareholder return bands and/or the cash distribution amount to take into account any capital raising activities

Reducing the thresholds under the bands in the event of early testing

Increasing the cash distribution amount if the highest band is materially exceeded.

Getbusy Notice of AGM and Explanatory Statements

Getbusy Audited Results & Chairman’s Letter

Refer to 32:05 in the video above.

In striking resemblence, the Getbusy Cash distribution plan terms are as follows:

Awards under the CDP vest if the Company makes a gross cash distribution to shareholders in excess of £70million and up to £150 million within a 7 year period from the implementation date of the plan. An adjustment is made to the value of any award under the CDP to take account of any vested share options that have previously been exercised by the participants, thereby preventing participants benefiting from both the CDP and a distribution in respect of any exercised share options.

At a gross cash distribution of £70m (the “Entry Point”), the award paid to Daniel Rabie under the CDP, the VCP and the EMI Chare Option Plan would be £5.0m and the award paid to Paul Haworth would be £1.75m. These amounts are based on the approximate values that, absent the CDP, would otherwise be paid on the participants’ fully vested and exercised share options.

Above the Entry Point to a gross cash distribution of £120m (the “Target Point”), the participants earn a linearly increasing share of the incremental distribution above the Entry Point. Daniel Rabie’s share increases from 7.0% at the Entry Point to 15.0% at the Target Point. Paul Haworth’s share increases from 2.5% at the Entry Point to 10.0% at the Target Point. Above the Target Point, the share of the incremental gross cash distribution earned remains at 15.0% for Daniel Rabie and 10.0% for Paul Haworth up to a maximum award payable at a gross cash distribution of £150m (the “Stretch Point”).

However, Getbusy also has the "EMI Share option plan" and the "Value Creation Plan". The EMI is fully vested in full but the VCP will vest in January 2024. For the purposes of comparing the Cash distribution plans as per the first paragraph above, the CDP supercedes the previous plans so the % shown above is correct.

Comparing these 2 plans side by side it is very obvious that Getbusy is significantly more distribution to management. Well, it's clear that this plan is much better for Reckon shareholders than it is for Getbusy shareholders.

I much prefer the Getbusy business as I think Virtual Cabinet and Smartvault are much better products than Reckon One, Accounts Hosted and nQ Zebraworks etc.but I much prefer the incentives at Reckon as opposed to Getbusy.

iEnergizer (OTC:IBPO) - 0.1% Weighting

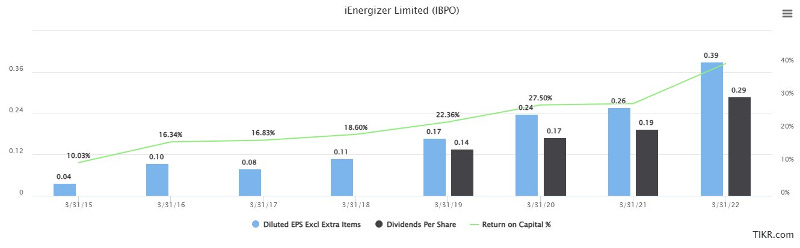

In the month, I did some research on iEnergizer, a holding company for a group of BPO companies based across India, US and Australia. Of the ~200 stocks on my watchlist as of May 2023, iEnergizer Ltd is the cheapest. The company has an increasingly profitable business and progressive dividend policy, yet trades on a PE of just 1.8x and has a LTM dividend yield of 46%.

Why?

The company is 83% owned by Founder and CEO, Mr. Anil Aggarwal, the controlling shareholder of EICR (Cyprus Ltd) which is the parent company of iEnergizer Ltd. This is important because the company has recently chosen to delist from the AIM exchange and continue trading unlisted. The market took this news poorly with it trading down amounts up to 90% below the high and at which price the LTM dividends per share would almost pay you off if it was maintained for just 1 year.

Key financials:

At the end of the day, I couldn’t get comfortable with the company going private, and could very well see no cash flow from the position. Out of curiosity in how the delisting would work I decided to allocate 0.1% of the portfolio to track it.

Closed Positions

No sales were made during the month.

Conclusion

Thank you for reading, these long form portfolio reviews are part of both my diligence to stay on top of my positions and the value for my paying subscribers, so I hope you get as much out of this as I do.