Hurdle Rate Unit Trust - Portfolio Update

Hurdle Rate Unit Trust - Portfolio Update

October 2023

Dear Unitholders,

This month the Hurdle Rate Unit Trust generated a Gross return to unitholders of (3.58%) Including performance fees, the Net return to unitholders was (3.66%). The unit price as at month end is $0.9574. The full history of performance data can be found on the first page of this document.

The end of October 2023 marks 6 months since the inception of the Hurdle Rate Unit Trust, and I am happy with the progress made so far. Of course, 6 months is not a long-time span, as I expect our average holding period to be between 3 and 5 years, but it is good to see a trend in the right direction. For comparison’s sake, I have added in a chart along with the ASX300 (XKO) market index, which given that this is an Australian domiciled trust with solely Australian unitholders, is the index I thought would be the most relatable for the average unitholder. The intention remains to strive for a 25% hurdle rate, and our fee structure is still based on the 0/6/25 performance fee structure utilised by the Buffett Partnership.

This month, I want to talk all about portfolio management which I hope will work for me. To kick things off, I would like to set the scene with a discussion on diversification.

Diversification

One thing which has become apparent since beginning the trust is that the time, I have on hand is much greater than I have ever had since starting investing. When I started this trust, I thought managing 6-8 names felt right, but I was overlaying my prior experience of working in a full-time role and underestimated just how much time was freed up when leaving employment. As a result, the pace at which I am researching ideas has multiplied, and I have begun to think that I can use this to my advantage by keeping hurdle rates static and narrowing the range of outcomes around this hurdle rate by investing in more positions.

The common criticism to this is that each idea is incrementally worse, but I have the dilemma of putting ‘too much’ time into just 6-8 ideas would be counterintuitive and worsen returns, rather than improve them, due to entrenchment and commitment bias. Sure, you can just put this extra time into researching more things which do not make it into your portfolio, but I think moving up the count of both total researched ideas and invested ideas is a good move given my duty of care to Hurdle Rate Unitholders. Especially given that as of October 2023 some 2/3 of the NAV is external capital. Here is Magellan fund manager, Peter Lynch to explain through an excerpt from his book “One Up on Wall Street”:

In my view it’s best to own as many stocks as there are situations in which: (a) you’ve got an edge; and (b) you’ve uncovered an exciting prospect that passes all the tests of research. Maybe that’s a single stock, or maybe it’s a dozen stocks. Maybe you’ve decided to specialize in turnarounds or asset plays and you buy several of those; or perhaps you happen to know something special about a single turnaround or a single asset play. There’s no use diversifying into unknown companies just for the sake of diversity. A foolish diversity is the hobgoblin of small investors. That said, it isn’t safe to own just one stock, because in spite of your best efforts, the one you choose might be the victim of unforeseen circumstances. There are several possible benefits:

(1) If you are looking for ten baggers, the more stocks you own the more likely that one of them will become a ten bagger. Among several fast growers that exhibit promising characteristics, the one that actually goes the furthest may be a surprise.

(2) The more stocks you own, the more flexibility you have to rotate funds between them. This is an important part of my strategy.

Some people ascribe my success to my having specialized in growth stocks. But that’s only partly accurate. I never put more than 30–40 percent of my fund’s assets into growth stocks. The rest I spread out among the other categories described in this book. Normally I keep about 10–20 percent or so in the stalwarts, another 10–20 percent or so in the cyclicals, and the rest in the turnarounds. Although I own 1,400 stocks in all, half of my fund’s assets are invested in 100 stocks, and two thirds in 200 stocks. One percent of the money is spread out among 500 secondary opportunities I’m monitoring periodically, with the possibility of tuning in later. I’m constantly looking for values in all areas, and if I find more opportunities in turnarounds than in fast-growth companies, then I’ll end up owning a higher percentage of turnarounds. If something happens to one of the secondaries to bolster my confidence, then I’ll promote it to a primary selection.

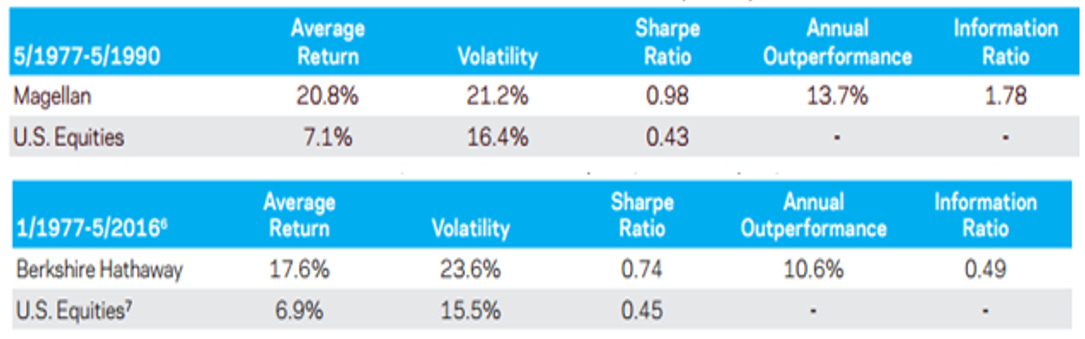

Having read this commentary, here is a few takeaways for me. I should invest in as many ideas as possible provided they pass the stringent rules I have set (including exceeding a 25% compound return hurdle rate). Diversification needs to be done based on consistent quality of ideas, if done so you can perhaps approach the returns of something like the Magellan fund as shown below. It is compared to Berkshire Hathaway on the right, rather, this study does a good job analysing both records. The article concludes due to Lynches’ lack of leverage, open ended structure, and more exposure to bear markets that “It is highly unlikely that the performance records of both investors were due to luck. That said, the probability that Lynch’s results were due to luck is far, far smaller than the probability that Buffett’s results were due to luck.”

Managing my Investible Universe

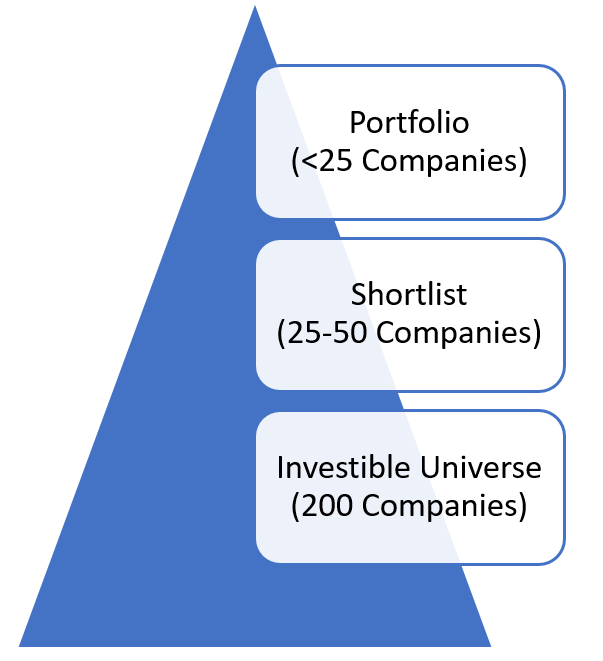

As you would expect from the outset of the trust, I have broadly an investible universe of professional and financial services companies worldwide. I have been finding this overwhelming of late to manage the multiple competing ideas, so I have developed a funnel approach as shown, not including my regular activities of monitoring for special situations outside of this investible universe.

Starting from the bottom, the investible universe has been capped at 200 companies at a time. These companies I will monitor passively through receiving announcements via. email, and monitoring multiples using Koyfin. This will allow me to keep abreast of any interesting developments which might warrant elevating this to my shortlist.

The shortlist is the up to 25 companies not in my portfolio that I am most interested in right now. This list is both a research list, and a list of competing ideas where I can look for replacements for things within the portfolio. In addition to monitoring announcements, I am also considering talking to management, attending calls, maintaining more in-depth modelling and research amongst other things.

The portfolio is as you know it, ideas which have met our hurdle rate and other investment standards. I have capped this at 25 names and should there not be enough names in the shortlist to populate this up to 25 companies, I am perfectly fine shrinking the number of companies down to exclusively those where the hurdles are maintained (at purchase). When a portfolio company falls below an expected return of 15%, I look for a replacement in the shortlist or would consider shrinking the number of companies in the portfolio by consolidating the existing portfolio.

Position Sizing

As everyone would know, I am quite transparent about what investments have been made within the trust, however, I think something that I like to keep behind closed doors is the portfolio management side of things. There are many approaches to this, and for quite a long time my own approach to be relatively equally weighted at the ‘cost base’ level and to let investments run their course. With the addition of external capital, I have taken it upon myself to take this much more seriously, and there is a developing approach to position sizing in my mind which I wanted to briefly discuss.

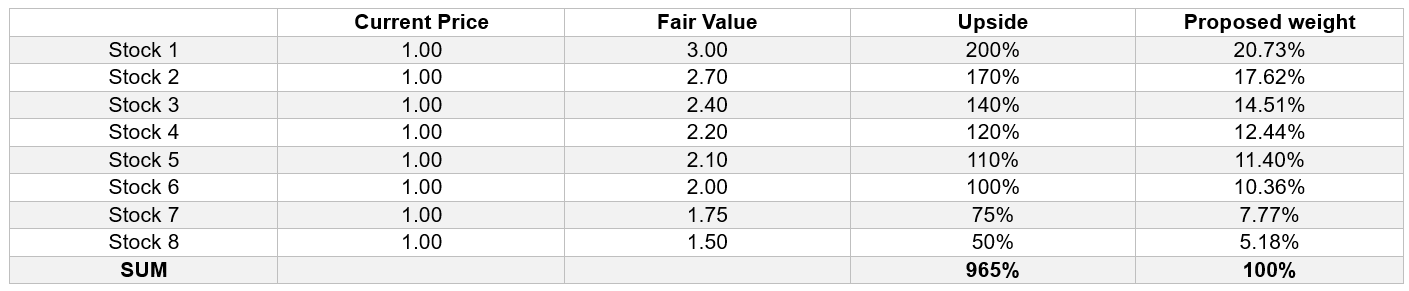

A hard rule in the Hurdle Rate Unit Trust is that an idea needs to make sense with a 25% discount rate before being worthy of consideration. Beyond that, ideas are largely weighted on perceived reward. I run each idea through a simple valuation process, assuming a 5-year holding period, and look to weight ideas on a % of the Upside SUM. To explain, I can illustrate below what this may look like.

Risk is something I control to the best of my ability, and in some cases I have taken the action to weight things greater than they would otherwise be because of the existence of a highly confident outcome (and vice versa). Thus, variations between my actual weighting and proposed weighting go through a screening process of justification whether the weighting is appropriate or not. My exact weightings right now for example, are largely in line with proposed weighting, although there are a few ideas which have been overridden due to specific reasons, and I did make some changes this month informed by the above rationale.

Importantly, this isn’t something I rebalance all the time, I just look at it once a month and see whether anything has changed significantly, if any ideas need to be revalued, if any positions should be added to or trimmed etc. I try to consider all information at my disposal. My larger investible universe is also being gradually researched and valued so I have a shortlist of ideas which are ranked and stacked against my existing holdings should I want to replace anything.

Importantly, most special situations are invested into using 100% debt, so they have no impact on the weighting of the equity and are merely intended to be a boost to returns when they arise. Often these are only held for a few days, purely to take advantage of quick profits such as merger arbitrage, odd-lots, warrants exchanges and so on and so forth. Longer term special situations which would require equity are stacked up against other holdings as according to the process above.

Value Trading

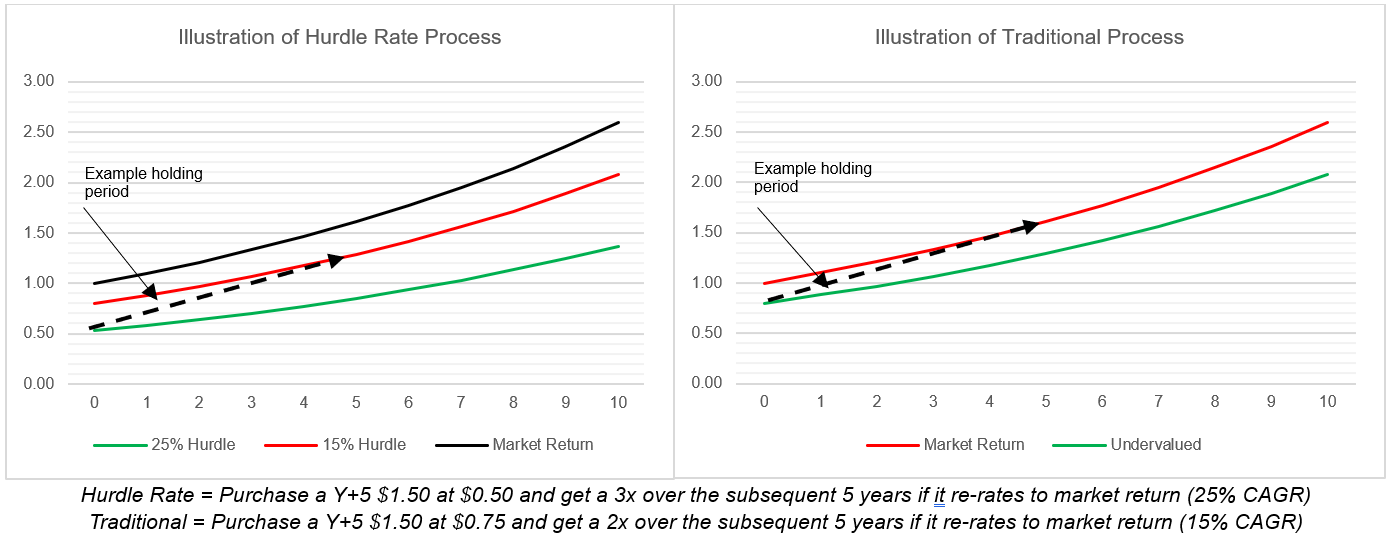

It is unlikely that a business can generate a 25% hurdle without some excitement from the market in the form of multiple expansion. And to maintain high discipline in this area, I haven’t talked about this but there is a hurdle to sell as well of 15%. In the event I think potential returns decline below 15% I would be inclined to sell to cash and reallocate into the existing portfolio or new ideas. To illustrate this, I have shown traditional value investment vs the Hurdle Rate approach below.

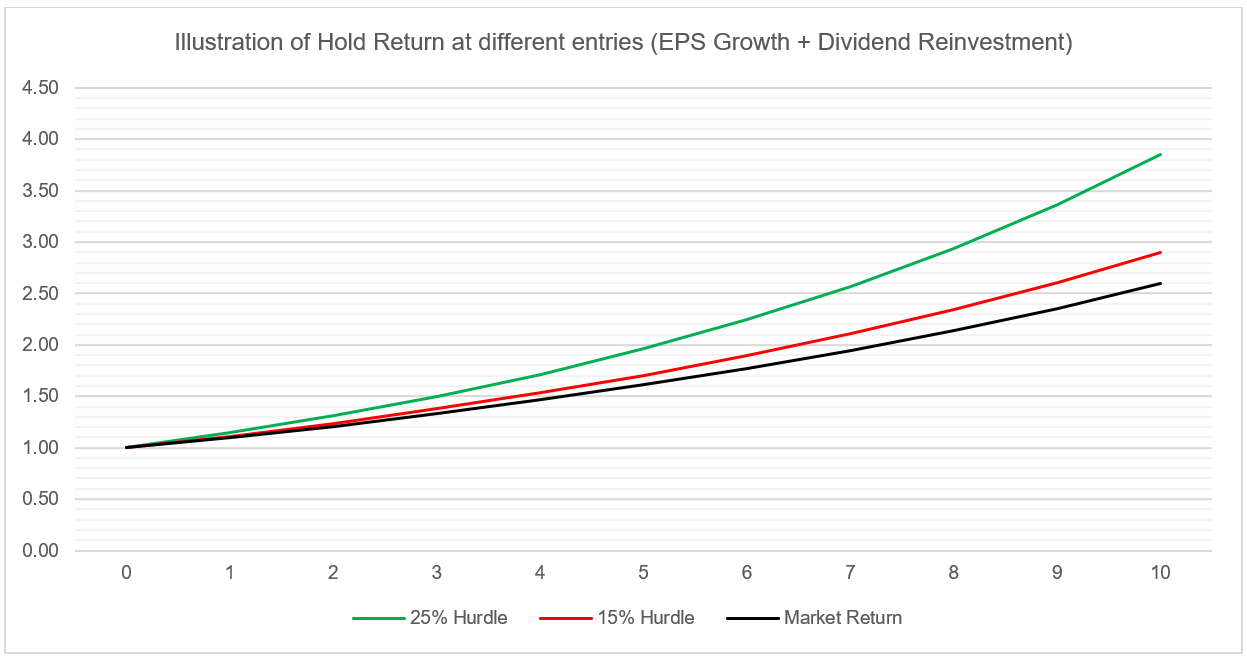

So, after looking at these charts, you might be wondering, what exactly is the difference here? Well, first by buying at a deeper margin of safety than other investors, I believe, that the possibility of losing money is drastically decreased, but perhaps the main factor is that we get both a higher free cash flow yield if any. To illustrate this further, we can plot the growth of $1 on various scenarios assuming you purchase a business generating a 10% ROIC and paying out 50% of earnings. The holding return (EPS Growth + Dividend Reinvestment) situations for a 10%, 15% and 25% return look like the following if the gap could close from Hurdle to Market return within a 5-year period.

The difference here is that the black line is reinvesting dividends at 10x earnings, the red is reinvesting at 8x earnings, and the green is reinvesting just above 5x earnings. In these 3 cases the EPS growth is the same, but the dividend yield is 5%, 6.2% and 9.5% respectively. Furthermore, the 5-year multiple expansion CAGR is 0%, 4.8% and 11.5% as well, bridging the gap between the hurdle rates and the hold return.

Herein lies the beauty of the approach. In my hypothesis, both hit rate and slugging percentage are increased by sliding the hurdle rate up, and ideally there is a demonstrable outcome from this approach in the years to come for unitholders.

Kelly Partners Group Holdings (ASX:KPG)

An update for the group’s strategic review was provided this month. The review continues to assess what combination of strategy, capital structure and governance will maximise long-term shareholder value, with the assistance of financial, legal and tax advisors. As part of this process, the group has established an independent board committee consisting of Stephen Rouvray, Lawrence Cunningham, and Ryan Macnamee to provide oversight of the review. Some general observations were relayed to shareholders, although have been repeated many times before, therefore the announcements felt unnecessary. Perhaps of the most interest was the discussion about the US market and the possibility of a dual listing with the primary shares in the US and use of CHESS depository interests (CDI) on the ASX. Nevertheless, the group has yet to decide. I trimmed our holding quite a bit to reallocate into new and existing holdings in both the previous and current month, but still hold a position in the company.

Diverger (ASX:DVR)

Late in the month Diverger received a counter-offer from COG Financial Services (ASX:COG) for $1.4083 per share (Half cash, half scrip), a business which I have written about before. Oddly enough the group determined this not to be a ‘superior’ proposal which is frankly ridiculous. The Diverger board is determined on embedding the Count synergies in their recommendation, which to us as shareholders is irrelevant as we would consider each on their own individual merits. The synergies of the acquiring business are irrelevant as there is no guarantee that those synergies can arise, and that COG cannot get synergies of their own for example.

Considering the weakness in support by the board, I took the opportunity in the strong trading on the day to sell our holding off at what was a strong premium to the Count offer, but reasonable discount to the COG offer. We realised a profit of $20,867 and annualised IRR of +145% ,which contributed +8.6% to the trust’ overall return since inception. I am still actively monitoring the situation; however, I saw it prudent in this case to take my chips off the table as there is the juxtaposition of a board recommending a lower bid, despite an obvious counterbid. If both deals end up failing, then we could see quite a re-trace to where it was prior to any deals. We will be ready should that event occur.

I know it is common to avoid capital gains tax, and in this case, we have recognised a significant capital gain, which is eligible for no concessional treatment. However, if I may clarify, my intent as trustee is to maximise after-tax returns rather than minimising tax. Securing a profit comes far ahead of holding out for the sake of a tax concession. As a reminder, unitholders can withdraw at any stage any amount of their invested capital to pay their taxes or opt to receive distributions in cash rather than reinvesting. I hope that tax planning becomes a constant issue due to excessive profits coming from the Hurdle Rate Unit Trust!

Sequoia Financial Group (ASX:SEQ)

During the month I had the pleasure of attending the Coffee Microcaps Conference, where I was kindly invited to as a VIP to attend to by the founder Mark Tobin. It was a very interesting day and fortunately I had the opportunity to meet and chat with the Sequoia CEO Garry Crole. I had spoken over zoom with Garry before but in the flesh, I was convinced of Garry’s genuine demeanour. In this event he presented these slides in which there is a number of interesting points made, many of which were simply reiterating what was said in the 2023 results.

Financially, the group reiterated their ‘return on management equity’ (ROME) implied valuation approach, but also had some additional colour as to their capital allocation approach. Namely, the following caught my eye:

- Maintain dividend at 90-100% of operating profit after tax whilst maintaining a target cash balance of $20m+.

- Utilise cash on balance sheet to acquire strategic EBITDA on 4-5 multiples of acquisition.

- Buy back when EV is below multiple of 4 that we can acquire growth at.

- Increase normalised dividends by 25% p.a. from 4c in FY 2023.

This is curious as it is implying that Garry can double the earnings of the group with ~$15-20m of capital over 3 years (depending on if dividend is 90% or 100%) given that they currently have $35m.

Orchard Funding Group (LSE:ORCH)

During the month, a new purchase into Orchard Funding was funded with the dividends received during the month. More detail into our rationale for this purchase is detailed here. In essence, Orchard Funding is a lending business which allows for clients to transition their lump-sum insurance premiums, professional services fees, or membership fees into instalment plans. It is a founder-led business trading as a deep net-net and high earnings yield, a good portion of which is paid out to shareholders, yielding high single digits. It is, however, a small business which requires securing larges amount of external funding to trade and operates in what is effectively a duopoly between 2 players larger than themselves.

Financial targets are a staple for the Hurdle Rate Unit Trust, and in this case, it is no different. Targets are set as a 45% payout ratio and 9% ROE. At a valuation of <5x earnings, this would equate to a 10% dividend yield and 5% EPS growth, meeting our hurdle for hold return. It is not farfetched to expect this to trade for 0.9x-1.0x book value at some stage in the short-medium term future. At 0.47x book value this would yield a double from the multiple, which when applied over our targeted 3–5-year average holding period would contribute an additional 15-24% compounded return to the investment. I would like to thank the unitholder which shared this with me.

Fiducian Group (ASX:FID)

Another purchase of Fiducian Group was also made. The full page write up can be read here. This increases our exposure to financial markets significantly, with over 90% of Fiducian’s profits coming from variable % of FUMAA based revenue on a fixed cost base. The rationale behind the purchase is that the Australian stock market is reasonably priced generally and investors should generally feel positive about their long-term returns buying the broader market today. Of course, that general view is the extent of the macro for me, but Fiducian has been priced for a bear market in my view, more specifically for a flat market, with net inflows which might just offset cost inflation and no market contribution. We are not paying for FUMAA increase in the form of market performance so I feel relatively confident taking a contrarian view that history will rhyme and Fiducian will continue to perform largely in line with what it has done previously, which when combined with a low valuation generates a return suitable for the Hurdle Rate Unit Trust. Lastly, I was fortunate enough to also listen to Rahul (Subsidiary CEO) at the Coffee Microcaps conference as well, and was impressed with his presentation and professionalism.

Sky Network Television (ASX:SKT)

As discussed in this write up, Sky is a short-medium term special situation which I anticipate to have a strong bid premium to it’s current price, supported by a strong absolute and relative valuation in the form of a high double digit free cash flow yield and the recent offer for Southern Cross Media (ASX:SXL). I will be waiting for the result of the NBIO process with keen eyes, and without an outcome I would be comfortable to remain a shareholder with strong absolute value. I believe these are strong traits of an appealing ‘merger arbitrage’ type situation. That is, situations in which you would be comfortable buying the business at the market price without the existence of an offer. As discussed in that write up, this is backed by my own personal line of credit, on-lent to the trust, and is therefore not using trust equity.

Bravura Solutions (ASX:BVS)

As discussed in the write up, Bravura is an Australian software business going through a turnaround process. It has a significant cost base which if alleviated could lead to a mid-teens margin, which given the current valuation, could lead to a very cheap stock this time in 3 years’ time. Tomorrow they are releasing a plan at their AGM on their 3-year initiatives which I am keenly interested in.

Peoplein (ASX:PPE)

Peoplein is a heavily sold-off recruitment business where I think that the fears are largely unwarranted relative to the price decline. On FY23 numbers it is equivalent to an EV/EBITA of ~3x which quite frankly, even if they lose much of their earnings still appears attractive. However, I sized this accordingly as I have reservations about my conviction.

Concluding Thoughts

We saw negative performance this month despite the wildly successful Diverger deal, largely due to what I believe is widespread panic (especially in smaller companies), but we still beat the overall ASX300. I know what we own and am excited to take advantage of compelling opportunities as they come up. Diversification will smooth out our results and allow for the benefit of asymmetry. On the contrary, I am prepared to concentrate heavily where it counts.

Some key events for November which unitholders may find of interest are.

· Bravura AGM on the 2nd (Includes 3 Year plan)

· Kelly Partners AGM on the 10th (Possible update on strategic review)

· AF Legal AGM on the 14th (Includes Q1 Results)

· Diverger AGM on the 20th

· Sequoia AGM on the 23rd (Includes results through to October 2023)

· Finexia AGM on the 24th

· Peoplein AGM on the 27th

· Prime AGM on the 30th

· Dow Schofield Watts Half year results.

· Possible outcome of the NBIO due diligence for Sky Network Television

· Possible Orchard Funding Group full year financial results.

As a reminder to all unitholders, please feel free at any time to deposit or withdraw funds. I am also open to negotiating savings plans for a recurring deposit if it suits you better. Additionally, we still have 7 free positions for new unitholders so if anyone is (or you know someone who is) an Australian tax resident and interested in the prospect of investing into the Hurdle Rate Unit Trust, please contact me using my details below.

Yours sincerely,

Tristan Waine

Sole Director of the Trustee of the Hurdle Rate Unit Trust

Phone – +61 426 928 026

Email – Tristan.waine@outlook.com